Best Air Miles Credit Cards Singapore 2026

Compare the best credit card for air miles to see which one benefits you the most based on your spending habits.

Refine Your Results

FEATURED OFFERS

We found 30 credit cards for you!

%20Medium%202.jpeg)

%20Medium%202.jpeg)

AA.png)

AA.png)

Disclaimer: At MoneySmart.sg, we strive to keep our information accurate and up to date. This information may be different than what you see when you visit a financial institution, service provider or specific product’s site. All financial products and services are presented without warranty. Additionally, this site may be compensated through third party advertisers. However, the results of our comparison tools which are not marked as sponsored are always based on objective analysis first.

Why Trust MoneySmart 💡

MoneySmart helps Singaporeans compare verified financial products side-by-side, so you find the best credit card, loan, insurance and other personal finance products for your needs — before you apply, not after. As an MAS-licensed platform with over 15 years in the market and a 4.4/5 Google rating from 100,000+ users, we surface exclusive sign-up bonuses and deals you won't find by going directly to a provider—with faster gift fulfilment and flexible redemption on top.

How We Choose and Rank Miles Credit Cards 🏅

We evaluate air miles cards in Singapore using a multi-criteria approach:

Rewards strength & flexibility

We prioritise cards with consistently high miles earn rates (both for local and overseas spend), a broad range of eligible spend categories, and enduring value such as non-expiring points.

Premium & bonus perks

Cards are rated for key features including airport lounge access, fast-track status, travel insurance, flexible transfer partners, and strong sign-up bonuses.

Promo & feature vetting

We also feature exclusive MoneySmart promos, updated monthly—bookmark this page and check back regularly to catch the latest campaigns!

Why Choose an Air Miles Credit Card in 2026?

Air miles credit cards are a top choice for Singaporeans in 2026—and it’s easy to see why. They transform everyday spending into valuable travel rewards, making them ideal for frequent flyers or those planning dream vacations.

With larger welcome bonuses, higher earn rates, and enticing travel perks, these cards are more compelling than ever for both seasoned jetsetters and everyday spenders.

Here, we’ve compiled a short guide on the best overseas spending and air miles credit cards to suit your spending and travel habits best.

Bigger welcome offers, faster rewards

Which miles cards best fits your lifestyle?

Beyond overseas trips, Singapore banks are rewarding digital-first lifestyles. Contactless PayWave, online shopping, and recurring travel-centric categories like hotels, airlines, and ride-hailing now feature enhanced earn rates.

- Frequent travellers: Top cards (like Citi PremierMiles and DBS Altitude) offer perks such as complimentary airport lounge visits, bonus miles for overseas spend, and other non-expiring travel rewards. These are perfect for those virtually “living at the airport”.

- Online spenders: With accelerated miles on e-commerce and food delivery, cards from UOB and AMEX turn your daily digital habits into future getaways.

- High earners & premium card seekers: Flexible redemption, premium perks, and high bonus earn caps make miles cards from DBS, Citi, UOB, Amex, and Standard Chartered especially attractive to those with bigger monthly budgets or frequent business travel.

How Do Air Miles Cards Work?

When you use an air miles card for purchases, you earn points or miles for every dollar spent. These can later be converted into frequent flyer miles with airline partners like KrisFlyer or Asia Miles. Unlike cashback cards that give instant savings, miles cards are best suited for those who plan ahead for travel and can maximise the value of their redemptions. Many miles cards come with additional perks such as airport lounge access, complimentary travel insurance, and hotel booking bonuses.

Thereafter, these points can be redeemed for miles under frequent flyer programmes like KrisFlyer miles or Asia Miles.

Here’s a step-by-step breakdown of how these cards actually function:

Local vs foreign spend

Miles and travel credit cards typically award bonus miles based on specific spend categories. In general, miles credit cards tend to focus on rewarding particular types of local spend, such as dining or groceries.

On the other hand, travel credit cards are more versatile, offering bonus miles for both local and foreign currency spend, making them ideal for frequent travellers who spend abroad.

- Local spend: Everyday expenses like dining, groceries, and shopping typically earn miles at a base rate. For example, the UOB PRVI Miles Card gives you 1.4 miles per $1 on local spend, including public transport such as bus and train rides.

- Overseas & foreign currency spend: Using your card abroad or on foreign websites usually earns a higher rate. For instance, the Citi PremierMiles Card rewards you with up to 2.2 miles per $1 on overseas transactions, giving you more value for international spend.

- Online & Travel Bookings: Certain cards boost rewards when you book through travel partners or specific booking sites. The Citi PremierMiles Card earns up to 10 Citi Miles per $1 on eligible Kaligo bookings and up to 7.2 Citi Miles per $1 on eligible hotel bookings worldwide on Agoda.

Merchant & category exclusions

Contactless payments

Contactless payments like Visa payWave, Apple Pay, or Google Pay generally count toward miles-earning transactions, as long as your merchant and spend type are eligible. Both the UOB PRVI Miles Card and DBS Altitude Visa Signature Card support payWave and major mobile wallets, making it easy to earn miles on daily tap-and-go spends.

How to redeem miles?

Here’s where it gets interesting. While some cards (like the AMEX Singapore Airlines KrisFlyer Ascend) credit miles directly to your airline’s frequent flyer account (in this case, KrisFlyer miles), most bank cards accumulate “reward points” which you’ll need to convert and redeem as miles.

Some cards, like the HSBC TravelOne, offer instant point-to-mile transfers, while others require a few days for processing. Most transfer programmes charge a conversion fee (e.g., $27.25 per airline transfer), so it’s best to accumulate points before converting.

- Transfer minimums: Typically, you need to convert a minimum block of points (e.g., 5,000 DBS Points = 10,000 KrisFlyer miles; 10,000 Citi Miles = 10,000 KrisFlyer miles).

- Processing delays: Once you request a transfer, expect a waiting period. Your miles may take several working days to arrive at your airline loyalty account.

💡 MoneySmart Tip: To get the best value, redeem miles for long-haul or business-class flights, where each mile can be worth 3–5 cents. Avoid using miles for merchandise or vouchers, as they usually provide lower value.

Miles expiry and shelf life

- Bank points: Each bank sets its own expiry rules. For example, DBS Points, Citi Miles, and 90°N Miles earned on the Altitude card never expire, while UNI$ from UOB expires 2 years from the last day of the quarter they were earned in.

- Airline miles: Once transferred, KrisFlyer miles (for Singapore Airlines) are valid for 36 months. So plan your redemptions because expired miles can’t be reinstated!

What are miles worth?

The value of a mile depends on how you redeem it, with flights offering the best value, typically ranging from $0.01 to $0.02 per mile. Business or first-class bookings and upgrades offer the most value for your miles.

While some cards allow redemption for cashback, merchandise, or gift cards, these tend to have lower value. Always check the fine print for additional fees, as certain travel partners or redemption methods may charge extra.

Top Air Miles Cards & Promotions in Singapore (2026)

Here’s a quick comparison of Singapore’s top air miles credit cards for 2026—sorted to help you spot the best fit for your travel and everyday spend style.

| Credit Card | Card highlights | Promotion | Valid until |

|---|---|---|---|

| HSBC Revolution Credit Card |

| Spend S$500 from the card account opening date to the end of the following calendar month to receive S$450 cash or 6,140 SmartPoints (gifts valued up to S$649).

Enter the exclusive lucky draw for a dream-destination getaway worth S$15,000.

Additionally, to celebrate Singapore's birthday, the first 10 customers who submit the claim form during the National Day Flash Deal will receive a S$61 cash bonus. | 1 Aug 2026 till 5 Aug 2026 |

| Citi PremierMiles Card |

| Spend S$500 within 30 days of card approval with your new Citibank Credit Card to qualify for either S$400 Cash Reward or 6,140 SmartPoints (worth up to S$649 in gifts), with rewards issued in about 5 weeks.

Enter the exclusive lucky draw for a chance to win a dream getaway valued at S$15,000 to your destination of choice.

During the National Day Flash Deal, the first 10 customers to submit the claim form will receive a S$61 cash bonus. | 1 Aug 2026 till 5 Aug 2026 |

| HSBC TravelOne Card |

| Receive S$400 Cash or 6,140 SmartPoints (worth up to S$649 in gifts) when you spend S$500 from the Card Account Opening Date to the end of the following calendar month.

Be in the running to win a grand prize of S$15,000 for a dream destination getaway in our exclusive lucky draw.

Additionally, celebrate Singapore's birthday with a S$61 Cash Bonus for the first 10 customers to submit the claim form during the National Day Flash Deal. | 1 Aug 2026 till 5 Aug 2026 |

| OCBC 90°N Card |

| Receive $250 Cash or 3,900 SmartPoints, enough to redeem an Apple AirPods Pro 3 worth S$349, when you apply and spend a minimum of S$400 within 30 days. National Day Flash Deal: be among the first 10 customers to submit the claim form and receive S$61 Cash Bonus. | 1 Aug 2026 till 14 Aug 2026 |

| Standard Chartered Journey Credit Card (No Annual Fee) |

| Receive S$180 Cash via PayNow or 2,800 SmartPoints (worth up to S$429 in gifts) when you spend a minimum of S$800 within 60 days and apply to any of the following SCB products via MoneySmart: Bonus$aver Account, CashOne Loan, EasyPay or Funds Transfer. Stackable Miles Promotion Earn 20,000 miles after spending at least S$800 during the initial 60 days after card approval. | 1 Aug 2026 till 14 Aug 2026 |

| American Express Singapore Airlines KrisFlyer Ascend Credit Card |

| New American Express Card Members can earn up to 45,000 KrisFlyer miles: 20,000 miles with an S$8,000 spend in 6 months and annual fee payment, 20,000 miles on first spend in the 15th month with fee payment, and 5,000 miles on the first transaction for first-time applicants. | 17 Jun 2026 till 31 Jan 2027 |

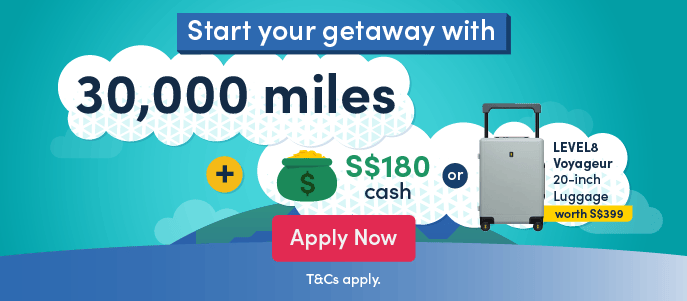

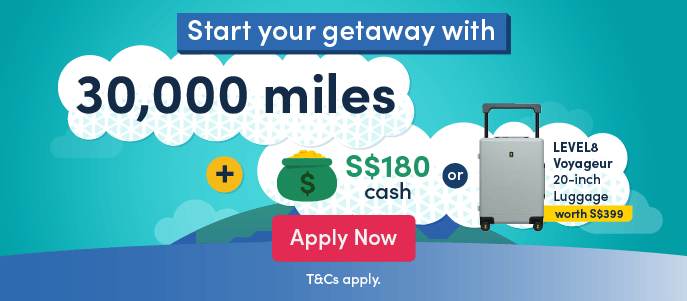

| Standard Chartered Journey Credit Card (Annual Fee Payable) |

| Receive S$180 cash via PayNow or 2,800 SmartPoints (worth up to S$429 in gifts) when you spend at least S$800 within 60 days and apply to any of the following SCB products through MoneySmart: Bonus$aver Account, CashOne Loan, EasyPay or Funds Transfer.

Receive 30,000 miles when you spend at least S$800 within the first 60 days of card approval and pay the first-year annual fee. | 1 Aug 2026 till 14 Aug 2026 |

| DBS Altitude Visa Signature Card |

| Receive a Samsonite MINTER 80/30 Trunk Luggage (worth S$680) or up to 38,000 miles by spending a minimum of S$800 within 60 days of card approval and maintaining a valid DBS PayLah! account. Terms and conditions apply. | 1 Jul 2026 till 31 Oct 2026 |

| UOB Visa Signature Card |

| Receive S$100 Samsung e-vouchers with a minimum spend of S$1,000 in the first month from card approval, plus 10% off at the Samsung online store. | 1 Jul 2026 till 30 Sep 2026 |

| OCBC 90°N Visa Card |

| Receive $250 Cash or 3,900 SmartPoints, enough to redeem an Apple AirPods Pro 3 worth S$349, when you apply and spend a minimum of S$400 within 30 days. National Day Flash Deal: be among the first 10 customers to submit the claim form and receive S$61 Cash Bonus. | 1 Aug 2026 till 14 Aug 2026 |

| American Express Singapore Airlines KrisFlyer Credit Card |

| New American Express Card Members can earn up to 16,000 KrisFlyer miles: 11,000 miles with a minimum spend of S$2,000 within the first 3 months and 5,000 miles upon the first transaction for first-time applicants. | 17 Jun 2026 till 31 Jan 2027 |

| UOB Lady's Card |

| Receive S$30 Cash with no minimum spend required for New-To-UOB customers. Plus, celebrate Singapore's birthday with a S$61 Cash Bonus for the first 10 customers to submit the claim form during the National Day Flash Deal. Receive S$100 Samsung e-vouchers after spending a minimum of S$1,000 in the first month from card approval, plus 10% off at Samsung online store. | 1 Aug 2026 till 14 Aug 2026 |

| UOB PRVI Miles Mastercard Card |

| Receive S$30 Cash with no minimum spend required for New-To-UOB customers. Plus, celebrate Singapore's birthday with a S$61 Cash Bonus for the first 10 customers to submit the claim form during the National Day Flash Deal. Receive S$100 Samsung e-vouchers after spending a minimum of S$1,000 in the first month from card approval, plus 10% off at Samsung online store. | 1 Aug 2026 till 14 Aug 2026 |

| DBS Altitude American Express Card |

| Receive a Samsonite MINTER 80/30 Trunk Luggage (worth S$680) or up to 38,000 miles by spending a minimum of S$800 within 60 days of card approval and maintaining a valid DBS PayLah! account. Terms and conditions apply. | 1 Jul 2026 till 31 Oct 2026 |

| UOB PRVI Miles Visa Card |

| Receive S$30 Cash with no minimum spend required for New-To-UOB customers. Plus, celebrate Singapore's birthday with a S$61 Cash Bonus for the first 10 customers to submit the claim form during the National Day Flash Deal. Receive S$100 Samsung e-vouchers after spending a minimum of S$1,000 in the first month from card approval, plus 10% off at Samsung online store. | 1 Aug 2026 till 14 Aug 2026 |

| UOB PRVI Miles American Express Card |

| Receive S$30 Cash with no minimum spend required for New-To-UOB customers. Plus, celebrate Singapore's birthday with a S$61 Cash Bonus for the first 10 customers to submit the claim form during the National Day Flash Deal. Receive S$100 Samsung e-vouchers after spending a minimum of S$1,000 in the first month from card approval, plus 10% off at Samsung online store. | 1 Aug 2026 till 14 Aug 2026 |

| KrisFlyer UOB Credit Card |

| Receive S$100 Samsung e-vouchers with a minimum spend of S$1,000 in the first month from card approval, plus 10% off at the Samsung online store. | 1 Jul 2026 till 30 Sep 2026 |

| DCS Flex Visa Platinum Card |

| First-time DCS cardholders receive a S$50 GrabGifts Voucher from MoneySmart and a CATERPILLAR Industrial Plate Trunk Luggage from DCS after spending S$800 within the first 30 days of approval. | 3 Aug 2026 till 31 Aug 2026 |

Key takeaways

- Choosing the right miles card depends on your travel frequency and spending patterns.

- Earning rates shown are the typical bonus miles earn rate; however, even higher earn rates may apply in special promotional or category spend scenarios.

- All featured bonuses and campaigns are subject to eligibility, qualifying spend, and T&Cs per issuer.

- "Annual Fee" column reflects the main (principal) card, not supplementary cards.

Travelling soon? Get covered with travel insurance starting as low as $17!

Find the Perfect Miles Card For Your Travel Style

Different travellers have different priorities—some chase luxury, others prefer practical everyday earn rates. Each top pick is matched to a distinct user profile, with a quick rationale, main eligibility or offer note to match your spending habits and

Frequent traveller: UOB PRVI Miles Card

- Why this card: Ideal for those who frequently travel within Southeast Asia and beyond. Earn up to 3 miles per $1 on regional spend (Indonesia, Malaysia, Thailand, Vietnam) and 2.4 miles per $1 for other overseas spend. Plus, enjoy 4 complimentary Priority Pass airport lounge visits per year.

- Additional benefits: No minimum spend; reliable for both local and international travel.

- Eligibility: Minimum annual income $30,000 (Singaporean/PR); $261.60 annual fee (1st-year waiver).

⭐ READ: UOB PRVI Miles Card Review

Local spender: Standard Chartered Journey Card

- Why this card: Perfect for those who prioritise everyday spending and travel occasionally. Earn 1.2 miles per $1 on general local spend, with up to 3 miles per $1 on local transport (including Grab rides), food delivery (e.g. foodpanda, Deliveroo), and everyday spend.

- Additional benefits: Earn 2 miles per $1 on eligible overseas spend; 2 complimentary Priority Pass airport lounge visits per year and up to $500,000 complimentary travel insurance; 360º Rewards Points never expire. Can be redeemed for miles, cashback, or shopping vouchers.

- Eligibility: Minimum annual income $30,000 (Singaporean/PR); $196.20 annual fee (1st year waiver) with “FEE WAIVED” option.

Online Shopper: HSBC Revolution Credit Card

- Why this card: Earn up to 4 miles per $1 on online and contactless* transactions including popular e-commerce and travel platforms*. Versatile for digital lifestyles and avid online shoppers.

- Additional benefits: Flexibility to offset spending with reward points or split purchases into monthly instalments; no minimum spend; bonus reward points capped at 13,500 points* per month.

- Eligibility note: Minimum annual income $30,000 (Singaporean/PR); no annual fee.

*Perks extended till 28 Feb 2026.

⭐ READ: HSBC Revolution Card Review

Travel reliability: DBS Altitude Visa Signature Card

- Why this card: Ideal for those making high-value purchases such as flights, holidays or major bookings. Eligible local spend earns 1.3 miles per $1, whereas foreign spend earns up to 2.2 miles per $1.

- Additional benefits: Up to 3 miles per $1 on select bookings via Agoda, Expedia, and other travel partner sites; DBS Points never expire; up to 2 complimentary Priority Pass airport lounge visits per year.

- Eligibility note: Minimum annual income $30,000 (Singaporean); $196.20 annual fee (1st year waiver).

SQ Loyalists: AMEX Singapore Airlines KrisFlyer Ascend Credit Card

- Why this card: Especially rewarding for Singapore Airlines loyalists; direct miles credit to your KrisFlyer account, complimentary fast-track to KrisFlyer Elite Gold, and generous SIA travel perks (including complimentary Hilton stay & lounge vouchers).

- Additional benefits: Generous SIA travel perks like complimentary Hilton extra night stay and airport lounge access, priority check-in, and baggage allowance for KrisFlyer members.

- Eligibility note: Minimum annual income $30,000 (Singaporean); $397.85 annual fee (no waiver).

⭐ READ: AMEX Singapore Airlines KrisFlyer Ascend Card Review

Global professionals: Citi PremierMiles Card

- Why this card: Earn 1.3 miles per $1 on eligible local spend, up to 2.2 miles per $1 on eligible foreign spend; outsized value for high-spending professionals or premium users who want maximum flexibility.

- Additional benefits: 2 complimentary Priority Pass airport lounge visits per year; can redeem DBS points for flights, hotel stays, and retail purchases through their DBS Rewards program.

- Eligibility note: Minimum annual income $30,000 (Singaporean/PR); $196.20 annual fee (1st year waiver).

⭐ READ: Citi PremierMiles Card Review

Overview: Miles Optimisation Checklist

1. Audit your monthly spend (groceries, dining, bills, travel) and match to the highest-earning card.

2. Strategically apply for a new credit card just before a major expense to maximize welcome deals.

3. Register for all digital wallet, contactless, and online banking features to unlock bonus earn rates.

4. Stack and build a reliable credit card roster for various dedicated spending categories/types. For instance, the SCB Journey Card is more suited for daily, local spend as compared to AMEX Singapore Airlines KrisFlyer Ascend Card that’s geared towards SIA-related spends.

5. Track your rewards and miles expiry schedule. Set phone reminders for both points and miles, to convert or redeem them before expiry.

6. Always pay in full and on time to avoid interest charges and late payment fees that wipe out your rewards.

7. Review eligible MCCs and exclusions before major transactions: does your spend really qualify for bonus miles?

8. Transfer miles in larger blocks where possible to minimise conversion fees (typically $25-$27 per transfer).

9. Monitor MoneySmart promotions monthly to qualify for exclusive sign-up gifts and rewards as well as limited-time enhanced earn rates to seize them when they align with your spending plans.

UOB PRVI Miles VS DBS Altitude

Battle of the cards! Ever wondered what the difference is between these two travel cards?

Pros & Cons of Miles Credit Card

Pros

- Earn miles on everyday spending

- Complimentary seat selection

- Flexibility in redemption

- Priority boarding and check-in

- Additional baggage allowance

- Booking flexibility waiver

- Perks through reward points or cashback

- Express upgrade of exclusive airline class

Cons

- Can only be redeemed for flights

- No cashback or limited cashback benefit

- Limited airline choices

- Annual fees

- Conversion fees

How Much is 1,000 KrisFlyer Miles Worth?

The value of 1,000 KrisFlyer miles will differ for different destinations as per SIA's redemption chart, so naturally, the average value of a mile if you were to redeem a Saver Award return ticket will differ according to the destination you pick.

Example: 4D3N Bangkok Economy Saver Award Ticket

For travel in November 2025, return flights from Singapore to Bangkok start from approximately S$306. Based on that, here’s how to calculate the value of your miles:

- Flight details: Singapore → Bangkok, return Economy Saver Award

- Miles required: 27,000 miles

- Base fare: S$306 (exclusive of taxes and fees)

- Calculation: S$306 ÷ 27,000 miles = ~S$0.0113 per mile

Thus, in this case, the average cost of a mile is valued at around 1.13 cents per KrisFlyer mile for this redemption.

Disclaimer: Promotional deals for airfares and mileage redemptions may vary over time, potentially affecting the value of KrisFlyer miles.

Read our guide on the best credit cards with airport lounge access

Discover all credit cards with complimentary access to airport lounges like Changi Airport lounges and many more around the world.

How to Earn & Maximise Miles in Singapore

Singapore’s air miles credit card scene is more competitive than ever—so to make the most out of every dollar spent, you’ll want a tactical, step-by-step approach. Here’s your ultimate guide to maximising value from your miles cards.

Focus on categories with highest earning rates

One of the quickest ways to earn miles is to get an air miles credit card that rewards you for your everyday spending — whether it’s online shopping, dining, travel bookings, or overseas spend.

Here are some of the best credit cards in Singapore to earn KrisFlyer miles, depending on your spending category:

| Category | Credit Card Recommendation | Details |

|---|---|---|

| Online & Contactless Payment | HSBC Revolution Card | Earns 4 miles per S$1 (10X rewards points) on online and contactless spend across eligible shopping, dining, and travel bookings. Capped at 13,500 bonus points per month. Valid till 28 Feb 2026. |

| Travel & Overseas Spend | UOB PRVI Miles Card | Earns up to 3 miles per S$1 on overseas spend in regional countries like Indonesia, Malaysia, Thailand, and Vietnam. Earns 2.4 miles per S$1 on all other eligible foreign currency spend — with no minimum spend required. |

| Dining, Transport & Online Shopping | KrisFlyer UOB Credit Card | Earns up to 3 miles per S$1 on eligible local categories like dining, online shopping, and transport, when you meet the minimum annual S$800 SIA Group spend. Ideal for frequent users of Singapore Airlines, Scoot, or KrisShop. |

| Online Travel Bookings | Citi PremierMiles Card | Earns up to 10 Citi Miles per S$1 on Kaligo bookings and up to 7.2 Citi Miles per S$1 on hotel bookings worldwide via Agoda. |

Strategise welcome bonuses wisely

One of the quickest ways to earn a windfall of miles is to time your applications:

- Meet the qualifying spend on new credit cards applied via MoneySmart (e.g. S$500 or S$800 within 30–60 days). These entitle you to attractive welcome bonuses offered exclusively on MoneySmart, such as up to XX,XXX miles, S$XXX cashback via PayNow, or lucrative SmartPoints.

- Apply only when you have upcoming unavoidable big spends (like wedding expenses, travel bookings, or home renovations) to easily hit minimum requirements.

- MoneySmart’s exclusive promotions change every month. 🔖 Bookmark this page to check back for enticing offers regularly.

Stack and rotate card roster by spend type

- Use different cards for different categories. For example: HSBC Revolution for online/contactless, UOB PRVI Miles for travel/overseas, and KrisFlyer UOB for daily spend.

- Be mindful of merchant category codes (MCCs). Some transactions (like utilities or insurance) are typically excluded, so stick to eligible shopping, dining, and travel merchants.

- Take advantage of limited-time promos and bonus ‘10X points’ earn periods by shifting your routine spend for those months.

Take note of miles expiry and transfers

- Non-expiring options: DBS Altitude and Citi PremierMiles both feature points/miles that never expire, giving you freedom to accumulate for major redemptions.

- Other expiry windows: Many bank rewards points (for example, HSBC’s) expire after 37 months, while KrisFlyer miles (after transfer) last only 3 years. It’s best to set reminders to avoid risking them expiring and losing out on their value.

- Bank-to-airline transfer times: Processing can take a few days to a couple of weeks (especially during peak periods). Plan ahead to have your miles in time for flight bookings or promotions.

Leveraging PayWave, digital wallets & shopping portals

Most modern miles cards support Visa PayWave, Apple Pay, Google Pay, Samsung Pay, and proprietary bank wallet services. This allows such digital payments to earn bonus miles at qualifying merchants too.

Purchases made via online shopping platforms and travel booking sites are generally eligible for bonus miles (check your card’s T&Cs!). However, note that top-ups to prepaid accounts and government or insurance payments are usually excluded, even if made through digital payment portals.

Pitfalls & mistakes to avoid

- ❌ Missing minimum spend for welcome bonuses due to poor planning.

- ❌ Overlooking points/miles expiry and letting value lapse.

- ❌ Using the wrong card for a category (e.g. using HSBC Revolution Card for overseas spending instead of a travel credit card like HSBC TravelOne Card).

- ❌ Paying unnecessary annual fees. Always calculate if your spending justifies the cost, or seek fee waiver options.

- ❌ Do not assume every contactless or digital wallet spending earns miles. Always double check MCC exclusions.

How to Redeem Miles By Card

5,000 DBS Points = 10,000 KrisFlyer miles

UNI$5,000 = 10,000 KrisFlyer miles

10,000 Citi Miles = 10,000 KrisFlyer miles

KrisFlyer miles

25,000 360 Rewards Points = 10,000 KrisFlyer miles

25,000 HSBC Points = 10,000 KrisFlyer miles

1,000 90N Miles = 1,000 KrisFlyer miles

Redeem 90N Miles for miles transfer to a range of airline and hotel partners. Minimum transfer block and fee apply.

25,000 HSBC Points = 10,000 KrisFlyer miles

Easily transfer HSBC Rewards Points to over 20 airline and hotel partners for free. If left unattended, your HSBC points will expire after 37 months.

Miles vs Cashback vs Flexible Rewards: Which is Best?

Choosing between air miles, cashback, or rewards points credit cards in Singapore depends on your spending habits and priorities.

To make things easier to understand, let’s break it down in simpler terms. Cashback cards are pretty straightforward – you earn cashback when you use your credit card to pay for bills such as telco, medical, and utility payments. Air miles cards reward travel-related spending, while rewards cards reward general local spending like shopping and dining.

Rewards credit cards that are worth getting often give you high bonus points for the latter, making it possible to earn air miles more quickly – for example, S$1 = 4 miles on your online shopping spending. However, do note that there are usually caps on these. So, the best card (or combination of cards) really depends on your spending habits.

Best for travellers and big spenders

Ideal for frequent travellers seeking flights, upgrades, or travel perks, with bonus benefits such as airport lounge access, travel insurance, and miles that never expire.

- Citi PremierMiles Card: 1.2 miles per S$1 on local spend; 2.2 miles per S$1 on foreign currency spend.

- Standard Chartered Journey Card: Up to 3 miles per S$1 on select local transport, food delivery, and online groceries; 1.2 miles per S$1 on other local spend; 2 miles per S$1 on foreign currency spend.

- DBS Altitude Visa Signature Card: 1.3 miles per S$1 on local spend; 2.2 miles per S$1 on foreign currency spend.

Best for everyday spending

Perfect for those who want hassle-free cash savings each month, without the need to track points or miles. Enjoy tiered or capped rebates (e.g. up to 5% cashback) on select categories, with no complicated redemption processes.

- Citi Cash Back Card: Up to 8% cashback on eligible pirate commute, petrol, dining, and groceries worldwide, with minimum $800 spend per month.

- UOB One Card: Up to 10% cashback on daily spend at eligible merchants like Cold Storage, Giant, 7-Eleven, Guardian and other Dairy Farm merchants, online shopping via Grab, pumping petrol at SPC and Shell. Minimum $600, $1,000, or S$2,000 spend per month.

- Standard Chartered Smart Credit Card: Up to 10% unlimited cashback for eligible streaming services, dining, and commute.

Best for online spenders & bargain value hunters

Rewards points can be redeemed for miles, cashback, shopping vouchers, or other rewards.

- Citibank Rewards Card: 10X Points for select online and in-store purchases.

- Standard Chartered Rewards+ Credit Card: Use for online shopping and overseas spending

- OCBC Rewards Card: 15 OCBC$ (6 miles) per $1 at Watsons and select online shopping platforms; 10 OCBC$ (4 miles) per $1 in select retail categories, both online and in-stores

- DBS Woman’s World Card: Use to redeem Apple products, shopping vouchers, and for online hotel and staycation bookings with Agoda and Klook

Citi PremierMiles VS DBS Altitude

Compare which card suits you best - Citi PremierMiles or DBS Altitude.

User Reviews and Feedback: Insights From Real Customers

Curious about what’s really shaping the air miles cardholder experience in Singapore? We’ve gathered local data, not hearsay, to provide insights into recent poll results, popular redemption choices, and ongoing frustrations.

Poll findings: What matters most in 2025

What’s hot: Redemption trends & values

Miles redemption habits have shifted, with updates to the KrisFlyer programme:

- Saver-class economy tickets are now more attractive, with miles requirements for selected Asia/Southwest Pacific routes dropping by 5%.

- Business and first-class redemptions for Europe and the US have become more expensive, with miles needed increasing by 5%.

- The “Access Redemption” feature allows users to lock in flight seats with miles even when Saver redemption options aren’t available, though it may require more miles during periods of high demand.

Flight redemptions remain the go-to for the highest value, with typical redemption values ranging from S$0.01 to S$0.02 per mile, depending on route and timing. Promotions, high-value partner transfers, and bonus categories for hotel bookings also influence redemption choices.

Cardholder frustrations: Expiry, exclusions & roadblocks

| Challenge | Details |

|---|---|

| Miles expiry | While cards like Citi PremierMiles, DBS Altitude, and OCBC 90°N offer non-expiring miles, others impose a 3-year expiry once miles are transferred to airline programmes — leading to anxiety and frequent reminders to redeem. |

| Redemption devaluation | 16% of surveyed users noted that it’s becoming harder and more expensive to redeem for premium cabin flights, following award chart changes. |

| Exclusion of certain categories | Many cardholders face issues with excluded spend such as insurance, government transactions, and educational fees — especially frustrating for frequent miles collectors. Additionally, some cards cap bonus rates on popular categories, disappointing high spenders. |

| Fees sensitivity | Cardholders often weigh annual fees against benefits, seeking to offset costs with sign-up promotions and renewal bonuses. For example, 31,000 miles for the Amex KrisFlyer Ascend and 38,000 miles for the DBS Altitude are popular offers — but only if users can meet minimum spend requirements. |

FAQs About Miles Credit Cards in Singapore

Which credit card is the best for air miles in Singapore?

There is no single best air miles card for everyone—your spending style determines the right fit. Citi PremierMiles, DBS Altitude, and UOB PRVI Miles are top for general spending (1.2–1.4 mpd locally, up to 2.4 mpd overseas, points don't expire). Cards like Citi Rewards offer 4 mpd on online spend (capped at S$1,000/month).

How do I earn a free air ticket as quickly as possible?

- Base earn rates are usually low, so everyday small purchases take time to accumulate miles. To earn a free ticket faster, focus on larger local spend, use your card overseas where earn rates are higher, and take advantage of bonus miles with partner merchants.

What’s the difference between KrisFlyer Miles, Asia Miles, etc.?

- Miles credit cards link to different programmes, and there is no universal air miles account. Banks often use their own proprietary points (e.g., Citi Miles) that require conversion, while some cards credit directly into established frequent flyer programmes like Singapore Airlines’ KrisFlyer, avoiding conversion hassles.

Citi PremierMiles vs UOB PRVI Miles vs DBS Altitude: Which is best?

- The “best” card depends on your priorities. Citi PremierMiles and DBS Altitude both offer non-expiring miles and lounge access but lower earn rates. UOB PRVI Miles is strong for overseas spenders, both regionally and internationally at 3 miles (at selected countries) and 2.4 miles per $1 abroad everywhere else.

Meanwhile for travel-related bookings, Citi PremierMiles offers up to 10 miles per $1 on select bookings via Kaligo and Agoda, whereas UOB PRVI Miles offers up to 8 miles per $1 through select Agoda and Expedia bookings. So really, they each have their pros and cons, and it’s up to you to determine which perks are the most valuable to you. How to redeem KrisFlyer miles?

- To redeem KrisFlyer miles, sign up for a KrisFlyer account, convert your reward points, and track expiry, denominations, conversion fees, and lead times. Redeem with Star Alliance and SQ partner airlines, keeping in mind you still pay taxes and other charges.

Can miles be transferred between airlines?

- Miles can only transfer between partner airlines. Citi PremierMiles allows transfers to multiple programmes including KrisFlyer, Asia Miles, Qantas, and more.

Do I need to pay any fees for my air miles credit card?

Most air miles cards charge an annual fee, covering administrative costs and services like lost-card replacement. Conversion fees may also apply when transferring points to frequent flyer programmes.

What are conversion fees for air miles credit cards?

- Conversion fees apply when moving card points to frequent flyer programmes. For instance, UOB PRVI Miles charges $25 per conversion, Citi PremierMiles charges $27.25 per conversion, and other cards may vary. Cards often link to multiple programmes, giving flexibility for international travel.

Which credit cards offer miles with no expiry?

- Some of the credit cards that offer miles with no expiry date include Citi PremierMiles Card, DBS Altitude Visa Signature Card, and OCBC 90°N Card.

How do I calculate the value of my miles?

- The value of a mile depends on how you redeem it. For flights, a common benchmark is $0.01 to $0.02 per mile. For example, if a flight ticket costs $500 or 25,000 miles, each mile gives you a value of $0.02. While redemption rates may shift, this is a helpful reference point for maximising value.

Which cards offer the highest earn rates for daily spend?

Miles awarded per S$1 vary by card and category. So far, the miles credit cards with the highest earn rates for daily spend include the Standard Chartered Journey Card (up to 3 miles per S$1 on eligible transport, food delivery, and online merchants), HSBC Revolution Card (4 miles per S$1 on select online and contactless spend, including travel), and UOB PRVI Miles Card (1.4 miles per S$1).

I’m a high-income earner. Which miles card suits me best?

If you’re a higher-income earner, you can consider miles credit cards with higher annual fees and higher annual income requirements. The American Express Singapore Airlines KrisFlyer Ascend Card is a good example of this, coming with a non-waivable annual fee of S$397.85 but earning you KrisFlyer miles directly and granting exclusive Singapore Airlines perks and access—ideal if you value premium travel upgrades and extras.

What are the typical eligibility criteria for miles cards?

- Standard income threshold: S$30,000 annual income (Singaporeans/PRs), S$40,000–S$45,000 for most foreigners. HSBC Revolution is the exception with S$65,000 (Singaporeans/PRs), or S$30,000 if you have an HSBC Total Relationship Balance of at least S$50,000.

- Age: At least 21 years old (differs for some cards, e.g. OCBC 90°N accepts SG/PRs at S$15,000 income for those aged 55+).

Always check the fine print for any extra documentation or unique requirements.

What ongoing fees should I expect?

- Annual fees range: Anywhere between S$0 (for cards like HSBC Revolution and Standard Chartered Journey due to annual fee promotions or waivers) to S$397.85(for the AMEX Singapore Airlines KrisFlyer Ascend).

- Waivers: Most cards offer a first-year waiver; continued waivers may require annual spend benchmarks (e.g., S$25,000 spend per year).

- Conversion fees: Transferring points to airline miles typically costs between S$25–S$27 per transfer.

What’s the process to convert my points to miles?

- Bank cards: (e.g., DBS Altitude, UOB PRVI, Citi PremierMiles) — Points are earned first and transferred in set blocks (e.g., 5,000 DBS Points = 10,000 miles).

- Direct-earn cards: (e.g., AMEX Singapore Airlines KrisFlyer Ascend) — Miles are credited straight to your KrisFlyer account.

- Transfer fees: Typically S$25–S$27 per conversion.

- Timing: Allow several working days for miles to reflect in your airline account.

Are there any categories or payments that don’t earn miles?

- Yes. All credit cards define eligible MCC (merchant category code) categories for earning bonus miles, along with exclusions such as insurance premiums, government payments, education, utilities, cash advances, and prepaid top-ups. Always check your card’s exclusion list before assuming which spend qualifies.

How long do I have before my points or miles expire?

- No expiry:DBS Altitude, Citi PremierMiles, OCBC 90°N (on the bank points/miles side).

- Expiry applies: HSBC Revolution points expire after 37 months; transferred KrisFlyer mile expire after 3 years, on the last day that they were credited.

- Pro tip: Track expiry dates and consolidate redemptions to avoid losing value.

Real scenario: How many miles can I earn in a year, and what’s that worth?

Example:

If you spend S$1,500/month on categories earning 1.3 miles/S$1 (e.g., DBS Altitude local spend):

- Annual spend: S$1,500 x 12 = S$18,000

- Miles earned:18,000 x 1.3 = 23,400 miles per year

A typical regional return ticket with KrisFlyer may require 25,000-28,000 miles (economy). At an estimated value of S$0.01 per mile, 23,400 miles are worth roughly S$234. This excludes welcome bonuses, accelerated category spend, or partner promotions, which can further increase the value.

However, do consider the following:

- Actual value per mile can fluctuate depending on route, class of travel, and redemption timing.

- Using cards in bonus categories or for overseas spend can help you earn miles faster.

- Always check MCC eligibility and exclusions to ensure your spend counts toward miles accumulation.

What are the unique perks or protections specific to certain miles cards?

- Priority Pass lounge visits: Offered by DBS Altitude, Citi PremierMiles, and Standard Chartered Journey (limitations apply per card).

- Travel insurance coverage: Select cards provide complimentary travel insurance coverage when you charge your full travel fare to the card (e.g., up to S$500,000 with Standard Chartered Journey, and S$1 million with AMEX Singapore Airlines KrisFlyer Ascend).

- Online purchase protection: OCBC 90°N offers e-Commerce insurance for all online purchases.

Which miles card should I get for best flexibility or digital-first features?

- DBS Altitude, Citi PremierMiles, OCBC 90°N: No expiry on miles or points, with broad earn categories across travel, dining, and online spend.

- HSBC Revolution: Earns 10X points on online and contactless transactions until Feb 2026 — great if your lifestyle is digital-heavy.

- All major cards: Support Apple Pay, Google Pay, and tap-to-pay options for everyday convenience.