Why Trust MoneySmart?

Why Trust MoneySmart?Key takeaways

The Debt Repayment Scheme (DRS) in Singapore is a pre-bankruptcy alternative that allows individuals to repay debts over a fixed period (up to 5 years) while avoiding bankruptcy restrictions.

To be eligible, your total unsecured debt must not exceed $150,000, and you’ll need a regular income, plus no prior DRS or bankruptcy record in the past 5 years.

The DRS process includes assessing eligibility, submitting documents online, and working with creditors and the Official Assignee to customise a repayment plan.

If you don’t qualify for DRS, you may explore other debt solutions in Singapore such as annulment of a bankruptcy order, discharge by the Official Assignee, or discharge by the High Court.

Some individuals may explore personal loans as a way to consolidate payments. Unlike the DRS, which is a government-administered legal scheme, personal loans are commercial products that should be carefully compared before applying for.

Many individuals in Singapore take on loans to pay for essentials such as housing, education, medical needs, or other big-ticket items. These kinds of debts are quite common and acceptable, often referred to as “good debt”.

However, when it comes to outstanding credit card balances, personal loans or other types of loans for additional lifestyle indulgences, it can result in bad debt and get you stuck in a tricky financial situation. At some point, you may owe so much debt that you may consider or be considered by the bank or creditor for an application of the Debt Repayment Scheme (DRS).

What Is The Debt Repayment Scheme (DRS)?

Administered by the Official Assignee (OA) from the Ministry of Law’s Insolvency Office, the Debt Repayment Scheme (DRS) is considered a pre-bankruptcy scheme that enables you to avoid bankruptcy.

It has several advantages over declaring bankruptcy like:

Not having any travel restrictions,

Having the option to repay your debts for a fixed period (about 5 years), and

Even maintain a regular savings account.

However, a DRS is not like a personal loan which you can sign up or apply for.

💡 Paying high interest on multiple loans or credit cards? |

One plan could cut your interest significantly. Compare all bank debt consolidation plans side by side on MoneySmart’s debt consolidation comparison page! |

What Is The Eligibility Criteria For DRS?

You can only be eligible for a DRS in the situation if your total debt amount does not exceed $150,000 after you file for or your bank files a bankruptcy application. To be eligible, there is a list of criteria that you need to fulfill:

Total liabilities do not exceed $150,000

To be employed and earning a regular income

To not be bankrupt or placed on the DRS in the recent past 5 years

To not be subject to a court-based arrangement over the past 5 years

To not be a sole-proprietor or partner in any organisation

How Does The Debt Repayment Scheme Work In Singapore?

Step #1: Assessing eligibility

Once you meet the eligibility criteria, the OA will further assess your suitability to be for the DRS and submit documents including those related to your income, expenditure, financial affairs, and proposed debt repayment plan to your creditors.

Step #2: Submission of required documents

If the OA deems you suitable for the DRS, you’ll receive a “Notice of Introduction on DRS & Filing of Statement of Affairs”, in which you’ll be notified to submit the following documents online, via the Ministry of Law’s e-Collection Portal. These documents include:

Statement of Affairs

Income & Expenditure Statement

Proposed Debt Repayment Plan

Other supporting documents (as per Annex B which you can refer to on their e-Collection Portal)

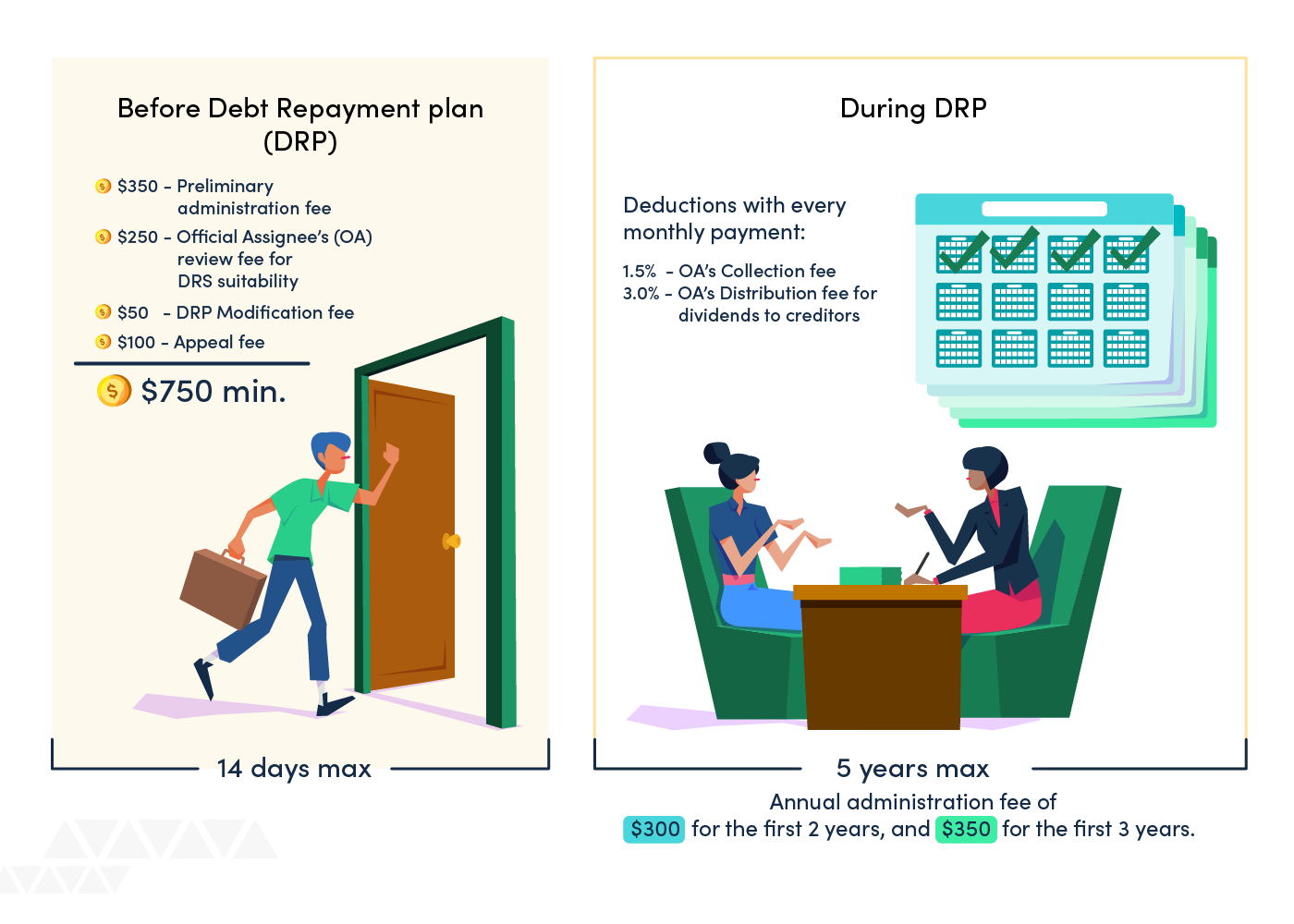

A total of 14 days will be given to you to view the Introductory Video and complete the online submission. Note that you’ve got to stick to this deadline well, or complete it before the 14 days to avoid a failure in your DRS suitability. If you miss this deadline, your case will be referred back to Court for the bankruptcy proceedings to be heard again.

When your online submission has been verified, a payment of the $350 preliminary admin fee is to be paid online. Thereafter, you’ll have to prepare to head down to the Ministry of Law’s office (there may be more fees to be paid prior to the meeting, so set aside a few hundreds for this) for a further assessment of your suitability for the DRS.

Step #3: Customising your DRP

At the meeting, the DRS administrators will chair the meeting, discuss your approved monthly instalments and terms and conditions of your proposed DRP with your creditors, before devising a final Debt Repayment Plan (“DRP”) for you. You’ll need to wait within 7 days of the meeting to be notified of the outcome of the discussion and DRP.

Step #4: Unsuitability for a DRS

In the situation the OA assesses that you are unsuitable, or if you do something that results in failure to comply with the OA’s instructions, you will be deemed unsuitable and your case will be referred back to Court for the bankruptcy proceedings to be heard again.

What Can I Do If I Don’t Qualify For DRS?

If you do not qualify for DRS, and have a creditor filing you for bankruptcy, you may consider these 3 options:

Annulment of the Bankruptcy Order by full settlement or unanimous composition/scheme

If you choose this option, you’ll need to apply to the court for an annulment of the Bankruptcy Order under Section 123 of the Bankruptcy Act. Note that a summons supported by an affidavit stating the reasons why your Bankruptcy Order should be annulled, must be filed in order for this application to be considered, or else, it’ll be rejected.

Discharge by Certificate of the Official Assignee

Applying to the Official Assignee for a certificate of annulment under Section 95A or Section 123A of the Bankruptcy Act, may actually increase your chances of getting your bankruptcy order annulled as the OA plays a big role in determining the outcome of the annulment.

Discharge by the High Court

The High Court’s assessment of your annulment of bankruptcy will also depend on the views of the OA and the bankrupt’s creditors, as well as other important factors such as your age, monthly income and total assets, as well as the amount of monthly instalments payments you have contributed to his bankruptcy estate.

Explore Personal Loan Options In Singapore (2026)

Unlike the DRS, which is a government-managed scheme, personal loans are commercial financial products offered by banks and financial institutions. They can help with debt consolidation in certain cases, but it’s important to compare terms carefully and ensure they suit your financial circumstances.

💡 MoneySmart Tip |

Use trusted online comparison tools like MoneySmart's personal loan comparison to review personalised rates, eligibility, and requirements across major banks in Singapore—helping you make a more informed choice quickly. |

The Fees And Costs Of A Debt Repayment Scheme

Advantages And Disadvantages Of A Debt Repayment Scheme

Advantages | Disadvantages |

No interest rate as compared to Debt Consolidation Plans (DCPs) and other personal loans | Time-consuming process of assessment for eligibility and suitability |

Convenient online submission of documents via the Ministry of Law’s e-Collection Portal | Requests are all subject to the approval of the OA and High Court |

No travel restrictions unlike those who declared bankruptcy | Failure to comply with the repayment plan may result in bankruptcy proceedings. |

Able to maintain a regular savings account unlike those who declared bankruptcy | May still affect your credit record during the repayment period. |

Flexibility of choosing repayment loan tenor (1–5 years) |

(1).png)