How to Apply For and Use a Credit Card in Singapore

MoneySmart offers the most comprehensive resources dedicated to helping you understand, compare, and choose the best credit cards Singapore has to offer. From eligibility requirements, step-by-step application processes, and card comparisons across all major banks (DBS, UOB, OCBC, Citibank, HSBC, Standard Chartered, Maybank), our step-by-step guide will give you the clear, actionable guidance you need.

Types of Credit Cards in Singapore

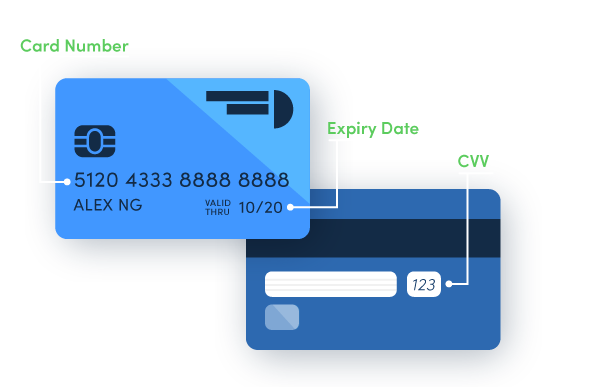

Knowing The Parts of Your Credit Card

Card number

Expiry date

CVV

Understanding Credit Card Features

Annual fee

Cashback / miles / rewards

Minimum annual income

Interest rate

Credit limit

Minimum monthly payment

Your Spending Deserves Better Rewards 🎁

Best Credit Cards in Singapore: Comparison

Whether you’re after unbeatable cashback, flexible miles, and rewards, big sign-up bonuses, or a solid starter card, this list covers the crowd favourites for different spending profiles like young adults, families, expats, and more. Here’s how they stack up right now:

| Credit card | Card type | Min. annual income | Annual fee | Card benefits | 💡 Best for |

|---|---|---|---|---|---|

| DBS Live Fresh Card ⭐⭐⭐⭐⭐ | Cashback | Singaporean/PR: $30,000 Foreigner: $45,000 |

$196.20 (1st year waived) | Up to 6% cashback on shopping & transport; digital wallet friendly Min. $800 monthly spend |

Young working adults seeking high rewards on everyday spending |

| UOB One Card ⭐⭐⭐⭐⭐ | Cashback | Singaporean/PR: $30,000 Foreigner: $40,000 |

$196.20 (1st year waived) | Up to 10% cashback on Shopee, McDonald's, Grab, SimplyGo Min. $600 / $1,000 / $2,000 spend per month (per quarter) |

Daily essentials spenders who frequent partner merchants |

| OCBC 365 Card ⭐⭐⭐⭐ | Cashback | Singaporean/PR: $30,000 (age 21–54) or $15,000 (age 55+) Foreigner: $45,000 |

$196.20 (2 years waived) | 6% cashback on petrol, 5% on dining, plus rewards on groceries, transport, streaming, bills Min. $800 or $1,600 spend per month |

Families with diverse spending across lifestyle categories |

| POSB Everyday Card ⭐⭐⭐½ | Cashback | Singaporean/PR: $30,000 Foreigner: $45,000 |

$196.20 (1st year waived) | Up to 5% cashback at Sheng Siong & SPC Some categories have no min. spend; others require min. $800 monthly spend |

Grocery shoppers and drivers seeking straightforward cashback |

| CIMB Visa Signature Card ⭐⭐⭐⭐ |

Cashback | Singaporean/PR: None (with fixed deposit) Foreigner: None (with fixed deposit) |

None | 10% cashback on groceries, online shopping, beauty, wellness, pets | Applicants with low/no income or rebuilding credit |

| Citi Cash Back Card ⭐⭐⭐⭐ | Cashback | Singaporean/PR: $30,000 Foreigner: $42,000 |

$196.20 (1st year waived) | 8% cashback on petrol/private transport, 6% cashback on dining/groceries Min. $800 monthly spend |

Drivers and frequent diners maximising category-specific rewards |

| Standard Chartered Simply Cash Card ⭐⭐⭐⭐½ | Cashback | Singaporean/PR: $30,000 Foreigner: $42,000 |

$196.20 (1st year waived) | 1.5% unlimited cashback on all spending with no caps or restrictions | Simplicity seekers who want straightforward, uncapped rewards |

| Citi Rewards Card ⭐⭐⭐⭐ | Miles / rewards | Singaporean/PR: $30,000 Foreigner: $42,000 |

$196.20 (1st year waived) | 10X reward points on online shopping, food delivery, ride-hailing Bonus points capped at ~$1,000 monthly spend |

Online shoppers and families who prefer points flexibility |

| HSBC Revolution Card ⭐⭐⭐⭐⭐ | Miles / rewards | Singaporean/PR: $30,000 (HSBC customers) or $65,000 (standard) Foreigner: $65,000 |

None | Up to 20x / 10X reward points on eligible contactless and online transactions internationally (i.e. dining, shopping, travel, ride-hailing, taxis, and memberships) | Online spenders, diners, and expats who value flexibility |

| UOB Lady's Card ⭐⭐⭐⭐ | Miles / rewards | Singaporean/PR: $30,000 Foreigner: $40,000 |

$196.20 (1st year waived) | Up to 10 miles per $1 on chosen category (beauty, dining, entertainment, groceries, fashion, transport, travel) Can change categories per quarter |

Women with predictable category spending wanting tailored rewards |

| Citi PremierMiles Card ⭐⭐⭐⭐½ | Miles | Singaporean/PR: $30,000 Foreigner: $42,000 |

$196.20 (1st year waived) | 1.2 miles per S$1 locally, 2.2 miles per S$1 overseas; up to 10 miles per S$1 on Kaligo/Agoda bookings Miles never expire 2 complimentary Priority Pass lounge visits per year |

Frequent travelers seeking airport lounge access and travel mile accumulation |

| DBS Altitude Card ⭐⭐⭐⭐ | Miles | Singaporean/PR: $30,000 Foreigner: $45,000 |

$196.20 (1st year waived) | 1.3 miles per S$1 locally, up to 2.2 miles per S$1 overseas DBS Points never expire 2 complimentary Priority Pass lounge visits per year |

Miles enthusiasts and travelers wanting non-expiring points |

| DBS Live Fresh Student Card | Cashback | Singaporean/PR: Not required (Student) Foreigner: N/A |

$196.20 (5 years waived) | 5% cashback at GV, Starbucks, McDonald's, Netflix, Spotify; $500/month spending limit | University students (age 21–27) building credit history |

Is There A Right Credit Card For You? Our MoneySmart Chief Business Officer weighs in

How to Apply For Credit Cards in Singapore: Step-by-Step Guide

Browse and compare credit cards on MoneySmart

Start by using MoneySmart's credit card comparison tool to explore options tailored to your needs. Filter by:

- Card type: Cashback, miles, rewards, student, or secured cards

- Minimum income: Match cards to your eligibility

- Benefits: Compare cashback rates, miles earning, annual fees, and promotions

Besides reviewing card details, don’t forget to compare the sign-up promotions and requirements!

Apply for credit card via MoneySmart

Click the "Apply Now" button on your chosen card's MoneySmart page. You'll be redirected to the bank's application portal to login with SingPass MyInfo for instant document retrieval (Singaporeans/PRs).

This application method usually offers the fastest (almost instant) approval, if all eligibility requirements and documents are met.

Provide all necessary documents (where needed)

However, if you’re unable to auto-retrieve your details via Singpass or need to manually submit, you’ll need these documents:

- Singaporeans/PRs: NRIC, latest CPF statement or payslip, proof of address (if needed)

- Foreigners: Passport, Employment Pass/S Pass, latest 3 months' payslips, bank statements with salary credit

- Students: NRIC, student pass, proof of full-time study

Wait for card approval

Card approval timelines vary:

- Instant to 1 day: MyInfo applications with complete docs (most Singaporeans/PRs)

- 1-3 days: Manual applications or complex profiles

- Up to 7-10 days: Expats or self-employed applicants

You'll receive SMS/email updates. Some banks (like DBS) offer instant virtual card access for Apple/Google Pay while you wait for your physical card.

Receive your credit card

Your card arrives within 5-7 working days via registered mail. Activate it using your bank's mobile app, phone hotline, or any ATM.

Once activated, use it for purchases locally/overseas, add it to digital wallets (Apple/Google Pay), and track rewards via your bank's app.

Card troubleshooting and support

Card declined? Check your credit limit, ensure activation is complete, and verify overseas usage is enabled if abroad.

Lost card or issues? Contact your bank's hotline immediately to block/replace your card.

How to Resolve Common Credit Card Application Issues?

Top reasons for delays or rejection

| Issue | What it means | How to avoid |

|---|---|---|

| Incomplete/missing documents | Outdated payslips, blurry ID scans, missing address proof | Upload clear, current documents (within 3 months) |

| Below minimum income | Card requires $30,000+ (SG/PR) or $40,000–$65,000 (foreigner) | Verify card's income requirement before applying |

| Multiple ongoing applications | Bank processes one new card per applicant at a time | Apply for one card, wait for outcome before next |

| Recent rejections | You must wait 30 days before reapplying | Wait cooling-off period; address rejection reason |

| Poor credit history | Existing high debt or late payments on record | Pay down debts before applying; review credit report |

| Mismatched details | Application info doesn't match MyInfo/NRIC | Double-check all details before submission |

What to do if you're rejected or delayed

| Step | Action |

|---|---|

| 1. Contact the bank | Reach out via official hotline, chat, or secure message to understand the exact reason |

| 2. Address document gaps | Upload any missing or corrected documents promptly |

| 3. Review eligibility | Confirm you meet salary, age, and status criteria for the specific card |

| 4. Check credit health | Pay down existing debts; avoid multiple new applications at once |

| 5. Wait cooling-off period | Typically 30 days before reapplying with the same bank |

Managing Your Card After Approval: Activation, Limits, Loss & Theft

1. Activate your card promptly

Timeline: Most cards can be activated immediately upon receipt, typically within minutes via digital channels.

2. Set or change your credit card PIN

3. Review and adjust credit limits

4. Set up Autopay (GIRO), alerts & reminders

💡 MoneySmart Tip: Monitor your first few statements to verify all transactions are legitimate and that your first-year annual fee waiver is applied correctly. If charged in error, request a waiver via your bank's app.

5. Update personal details

6. Report if card loss / theft / not received

If your card is lost, stolen, or hasn’t arrived:

- Immediately block your card (temporarily or permanently) and report it as lost in your banking app or by calling the 24-hour hotline.

- Call your bank’s hotline on their official website or within your app. Many banks allow instant freezing/unfreezing within the app.

- New cards are usually reissued within 3–5 working days, while some even provide a virtual replacement instantly.

7. Enable overseas use if travelling

FAQs About Credit Card Application in Singapore

Can I apply for multiple credit cards from different banks?

Yes, you can hold cards from multiple banks simultaneously. However:

- Ensure you meet each bank's minimum income requirement

- If recently rejected by any bank, wait 30 days before reapplying

- Each application may impact your credit score temporarily

- Banks assess your total credit exposure across all institutions

How many credit cards can I have in Singapore?

- There's no limit on the number of cards you can own. However, individual banks may cap the number of cards issued per customer based on your income, existing credit exposure, and internal risk policies.

Can I apply for a credit card if I'm self-employed or freelance?

Yes, but you'll need to provide additional documentation:

Document type What to submit Income proof Latest Notice of Assessment (NOA) from IRAS Business documents Business registration certificate (if applicable) Bank statements 3–6 months showing regular income deposits CPF statements Latest contribution history (if making contributions)

Most banks require self-employed applicants to meet the same minimum income thresholds ($30,000 for Singaporeans/PRs, $40,000–$65,000 for foreigners). Refer to our guide on best credit cards for freelancers and self-employed individuals to learn more.How can I request an annual fee waiver?

Most cards automatically waive the annual fee for the first 1–2 years. Check your card's terms to confirm.

However, for subsequent years, you may try:

- Requesting on your bank's mobile app (instant for eligible cards)

- Calling the customer service hotline

- Meeting minimum spend requirements if specified in card terms (e.g., $12,000 annual spend)

⭐ Cardholders with good payment history and regular card usage usually have the highest credit card annual fee waiver success rate.What if my card hasn't arrived after approval?

Most credit cards will be delivered via registered mail 5-7 working days after approval.

If delayed beyond 10 days:

- Check application status in your bank's app for dispatch confirmation

- Contact the bank's hotline to verify delivery address

- Request reissue if lost in transit (usually processed within 3-5 working days)

- Some banks offer instant virtual card access while you wait

How do I set up autopay for my credit card bill?

Aspect Details Setup method Via bank app/online banking (same or different bank) Payment options Full balance, minimum payment, or fixed amount Processing time 1–2 billing cycles to activate

⭐ Ensure sufficient funds by due date to avoid GIRO rejection fees.

How can I use my credit card overseas?

Preparation Action Enable overseas usage Activate in your bank's mobile app before departure SMS OTP setup Verify mobile number is registered for transaction authentication Emergency contact Save bank's 24-hour hotline number

💡 MoneySmart Tip: Most credit cards have a foreign currency fee ranging between 3%–3.25% (DBS, UOB, OCBC, HSBC credit cards) or 3.5%(Standard Chartered, Citibank). But in general, miles cards usually offset conversion fees for frequent travelers.What happens if I miss the minimum spend for sign-up bonuses?

You forfeit the advertised welcome gift or cashback. Banks enforce strict spend windows (typically 30-60 days from approval) and track eligible transactions automatically.

Avoid missing bonuses by:

- Setting calendar reminders for your deadline

- Verifying eligible transaction categories (bill payments, cash advances, and government payments often excluded)

- Monitoring progress in your bank's app