Best Standard Chartered Credit Cards Singapore

Compare the best Standard Chartered Singapore credit cards for cashback, dining, air miles, and shopping here.

Refine Your Results

FEATURED OFFERS

We found 7 Standard Chartered credit cards for you!

.png)

.png)

Disclaimer: At MoneySmart.sg, we strive to keep our information accurate and up to date. This information may be different than what you see when you visit a financial institution, service provider or specific product’s site. All financial products and services are presented without warranty. Additionally, this site may be compensated through third party advertisers. However, the results of our comparison tools which are not marked as sponsored are always based on objective analysis first.

Why Trust MoneySmart 💡

MoneySmart helps Singaporeans compare verified financial products side-by-side, so you find the best credit card, loan, insurance and other personal finance products for your needs—before you apply, not after. As an MAS-licensed platform with over 15 years in the market and a 4.4/5 Google rating from more than 2,000 reviews, we surface exclusive sign-up bonuses and deals you won't find by going directly to a provider—with faster gift fulfilment and flexible redemption on top.

Why Choose Standard Chartered Credit Cards in Singapore 2026?

So if you're eyeing the best Standard Chartered credit card or simply browsing our latest SCB credit card promotions, we've got you covered with everything from fee waivers to money-saving deals and perks.

Latest Standard Chartered Credit Card Promotions 2026

| Credit Card | Card highlights | Promotion | Valid until |

|---|---|---|---|

| Standard Chartered Simply Cash Credit Card |

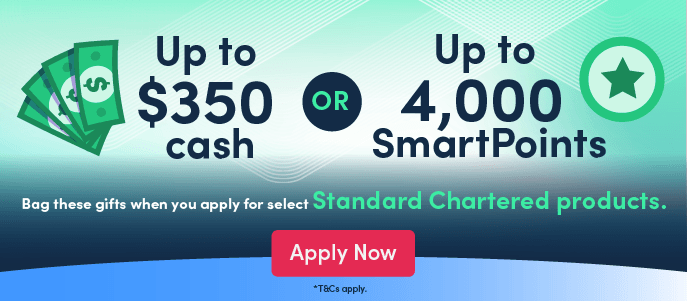

| Receive S$350 cash via PayNow or 4,000 SmartPoints (valued at up to S$469 in gifts) after you spend at least S$800 within 30 days and apply to any of the following SCB products through MoneySmart: Bonus$aver Account, CashOne Loan, EasyPay or Funds Transfer. | 1 Aug 2026 till 14 Aug 2026 |

| Standard Chartered Journey Credit Card (Annual Fee Payable) |

| Receive S$180 cash via PayNow or 2,800 SmartPoints (worth up to S$429 in gifts) when you spend at least S$800 within 60 days and apply to any of the following SCB products through MoneySmart: Bonus$aver Account, CashOne Loan, EasyPay or Funds Transfer.

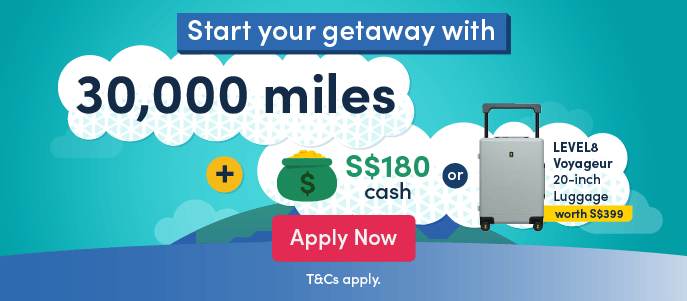

Receive 30,000 miles when you spend at least S$800 within the first 60 days of card approval and pay the first-year annual fee. | 1 Aug 2026 till 14 Aug 2026 |

| Standard Chartered Journey Credit Card (No Annual Fee) |

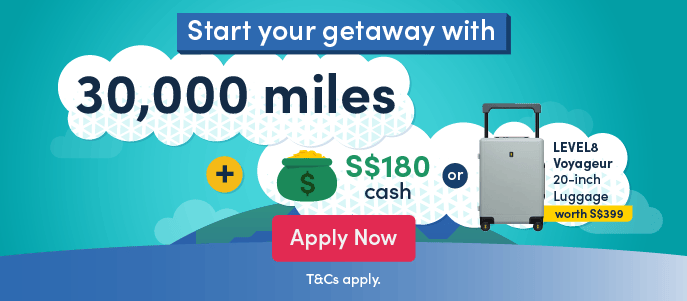

| Receive S$180 Cash via PayNow or 2,800 SmartPoints (worth up to S$429 in gifts) when you spend a minimum of S$800 within 60 days and apply to any of the following SCB products via MoneySmart: Bonus$aver Account, CashOne Loan, EasyPay or Funds Transfer. Stackable Miles Promotion Earn 20,000 miles after spending at least S$800 during the initial 60 days after card approval. | 1 Aug 2026 till 14 Aug 2026 |

Key Highlights of Standard Chartered Credit Cards

| Credit Card | Best for | Card Benefits | Minimum Spend | Cashback/Miles/Points Cap | Annual Fee |

|---|---|---|---|---|---|

| SCB Simply Cash Card | Fuss-free spending | 1.5% unlimited cashback on all eligible spend, boosted to 2% unlimited cashback when you spend at least $800 eligible spend per month. | None | No cap | $196.20 (First year waived) |

| SCB Journey Card | Air miles |

3 miles per $1 (mpd) on select local online transactions 2 mpd on eligible overseas spend 1.2 mpd on eligible local spend Rewards Points don’t expire 2 complimentary Priority Pass airport lounge visits per year Up to $500,000 travel insurance Flexibility to redeem rewards for cashback, miles, or vouchers |

None |

3 mpd rate capped at $1,000/month No cap on 2 mpd and 1.2 mpd |

$196.20 (First year waived with “FEE WAIVED” option) |

| StanChart Beyond Card | Luxury and reward earnings |

100,000 miles welcome offer Up to 8 mpd for Priority Private clients on eligible overseas dining Unlimited airport lounge visits for principal members Complimentary airport limousine rides Complimentary upgrades to business class with the purchase of two business and two premium economy tickets |

100,000 miles welcome offer 60,000 miles by paying the annual fee Bonus 40,000 miles for hitting the $20,000 spend within 3 months of card approval Otherwise, there is no minimum spend requirement |

No cap | $1,500 (No waiver available) |

Best Standard Chartered Credit Cards in Singapore (By Category)

🪙 Cashback Credit Cards

Standard Chartered Simply Cash Credit Card

Standard Chartered Smart Credit Card

✈️ Miles Credit Cards

Standard Chartered Journey Credit Card

Standard Chartered Visa Infinite Credit Card

🎁 Rewards & Lifestyle Credit Cards

Standard Chartered Rewards+ Credit Card

- Note: Rewards+ points capped at 20,000 points per year.

Honourable mention: Standard Chartered Simply Cash Card

🌟 Lifestyle Perks

The Good Life

Enjoy exclusive dining, retail, and wellness deals with Standard Chartered's partner merchants all across Asia.SmartDelay

Introduced as Standard Chartered's newest travel perk, enjoy free airport lounge access if your flight is delayed by 2+ hours under the SCB Smart Credit Card.Complimentary travel insurance

Enjoy free travel insurance coverage when you charge your travel fare to SCB credit cards like SCB Journey and SCB Visa Infinite. The extent of coverage amount varies with SCB card.

Eligibility & How to Apply for Standard Chartered Credit Cards?

Ready to start applying for your Standard Chartered credit card? Here’s what you need to know.

Eligibility criteria

| Credit card | Minimum age | Minimum annual income (Singaporean/PR) | Minimum annual income (Foreigner) |

|---|---|---|---|

| SCB Simply Cash Credit Card | 21 years old | $30,000/year | $90,000/year |

| SCB Journey Credit Card | 21 years old | $30,000/year | $90,000/year |

| SCB Smart Credit Card | 21 years old | $30,000/year | $90,000/year |

| SCB Rewards+ Credit Card | 21 years old | $30,000/year | $90,000/year |

| SCB Visa Infinite Credit Card | 21 years old | $150,000/year for all regular SCB banking customers | |

Apply for SCB credit card via MoneySmart

To apply for a Standard Chartered credit card, navigate to your preferred card listing (on this page).

Click on the “Apply Now” button > Input email address and click “Continue with email” > Fill up application details using Myinfo on SingPass

Prepare required documents

If you’re not relying on SingPass and are filling up application details manually instead, here are some possible documents required:

For commission-earners and foreigners, please refer to SCB’s official website for more details.

Wait for card approval

Standard Chartered will review and assess the eligibility of your SCB card application.

In most cases, instant digital approval is usually possible with applications via SingPass (and all supporting documents provided, if necessary). Otherwise, approval can take between anywhere between 1 to 14 working days, depending on the nature of the application.

Receive & activate credit card

Activate your virtual SCB credit card instantly via the SC Mobile Singapore app under the "Help & Services" tab.

Navigate to “Credit Card Activation & PIN Set” > Select your SCB credit card > Set new PIN for card > Enter OTP to registered number > Done!

Remember to add it to your mobile wallets (i.e. Apple Pay, Google Pay, Samsung Pay, Fitbit Pay) for convenient access.

Alternatively, you can wait to receive your physical SCB Card in the mail before formally activating it via the SC Mobile Singapore app.

Troubleshooting & support

If you experience instant denial or technical problems, check the troubleshooting tips and reach out to Standard Chartered support for help.

Additionally, remember to enable security feature precautions such as:

How to Earn SmartPoints and Redeem Complimentary Vouchers?

Each Standard Chartered credit card also comes with its own set of perks, ranging from bonus cashback at select merchants to exclusive travel and shopping rewards. Strategically selecting a card that aligns seamlessly with your spending patterns and timing your purchases with limited-time promos is key to unlocking optimal benefits by boosting your rewards.

So if you're looking to maximise your SCB credit card benefits, here's how to make every spend count.

#1: Apply for financial products

#2: Top-up your SmartPoints for bigger gifts

Here’s another illustration of how the top-up of SmartPoints works:

Visit our Rewards Store to explore our range of rewards today.

Standard Chartered Credit Card Reviews & User Ratings

👉 Overall, users praise SCB cards for their consistent cashback, miles, and digital convenience, though annual fees and minimum spend requirements are points to watch.

❌ Common compliants include:

SCB Simply Cash Card

Straightforward cashback card that becomes especially rewarding after hitting the S$800 monthly spend for the 2% rate.

Great for everyday use and big-ticket items.

SCB Journey Card

Praised for having no annual fee, lounge passes, and easy mile-earning on everyday categories.

Best for beginners in the miles game.

SCB Smart Credit Card

Popular among younger spenders for high cashback on dining and entertainment when meeting the spend requirement.

Downsides include the relatively high monthly minimum spend.

SCB Rewards+ Credit Card

Good for frequent overseas shoppers and foodies, thanks to 10X points on foreign currency spend and 5X on dining.

The main drawback is the capped points and the annual fee after year one.

SCB Visa Infinite Credit Card

Premium perks such as 6 lounge visits, travel insurance, and tax payment miles appeal to affluent travellers. However, the steep $150,000 annual income requirement makes it less accessible.

Swipe Smart, Earn Smarter

Standard Chartered credit card promotions await you here. Compare your best MoneySmart Exclusive sign-up reward options with us now!

Explore Other Standard Chartered Products

Beyond perks from The Good Life programme across dining, retail, and travel merchants, Standard Chartered offers a broad suite of banking and wealth solutions too. So after applying for your preferred Standard Chartered credit card, check out these other Standard Chartered products too:

FAQs About Standard Chartered Credit Cards

How do I pay my Standard Chartered credit card bill?

- You can pay your Standard Chartered credit card bills via Standard Chartered online banking or mobile banking app if you are an SCB banking customer.

From SCB ibanking/mobile app

Log in to your SCB ibanking or mobile app > Select “Pay SC Credit Cards” > Follow on-screen instructions to complete payment

From other banks

If you’re paying from other banks such as DBS, POSB, Maybank2u, you can pay your SC credit card bills via ibanking or the mobile apps as well.

Under “Payments and Transfers” > Select “Pay Other Credit Cards” > Follow on-screen instructions to complete payment Can I apply for a credit card without a SCB bank account?

- Yes, you can apply for a Standard Chartered credit card even if you do not have an existing SCB bank account. You will be able to pay your credit card bills from your current bank account via your bank’s ibanking, mobile app, or FAST transfers.

How can I redeem my Standard Chartered reward points in Singapore?

- Via Online Banking

Log into SCB Online Banking > Go to SCB 360° Rewards portal > Go to “Rewards Catalogue” to view redemption options > Select desired rewards > Proceed to checkout to complete redemption

Via SC Mobile

Log into SC mobile app > Go to “Credit Card Rewards” to view points and available redemption options > Select desired rewards > Proceed to checkout to complete redemption How long will my Standard Chartered credit card application take?

- Applications via SingPass Myinfo should be instantly approved digitally.

Whereas for manual applications, processing could take at least 14 days. Applications with incomplete or missing documents will result in further processing delay.

All SCB credit card applications are subject to approval by the bank. How do I cancel my Standard Chartered credit card?

- To request for an SCB credit card cancellation, follow these steps:

- Navigate to the Services tab > Go to “Help & Services” > Select “View All”

- Under Card Management > Select “Credit Card Cancellation” > Select reason for cancelling such as “I seldom use my credit card” or “I’ve too many cards” > Select card(s) to cancel

- Review details and submit request. A confirmation email and SMS will be sent upon completion and follow-up actions will take within 3 working days

Is there a cap on the miles I can earn with the Standard Chartered Beyond Card?

- No. The Standard Chartered Beyond Card offers unlimited miles earning potential. Whether you spend locally, overseas, or on dining, there’s no cap on the miles you can accumulate, making it ideal for high-spending individuals who want to maximise rewards without worrying about limits.

Do Rewards+ points expire?

- Yes, Rewards+ points are capped at 20,000 points per year, expiring if unused within the rewards programme’s terms.

Which airline programmes can I transfer miles to?

- You can transfer your Standard Chartered rewards points for KrisFlyer miles, Asia Miles, and other leading frequent flyer partners. A transfer fee applies (typically $26.75 per transfer) when converting SCB 360º Rewards Points into miles.

Can I get my Standard Chartered credit card annual fee waived?

- Yes, most Standard Chartered credit cards waive the first year; with exceptions to the rule where SCB Smart Credit Card waives with S$10,000 annual spend. Meanwhile, the SCB Visa Infinite Card strictly does not waive annual fees.