Quick Guide to Understanding Endowment Plans in Singapore

Disclaimer: This page is meant for educational purposes only and not meant to be taken as personalised or professional financial advice. Please consult with a trusted professional before committing to any insurance plan.

What is an Endowment Plan & How Does it Work?

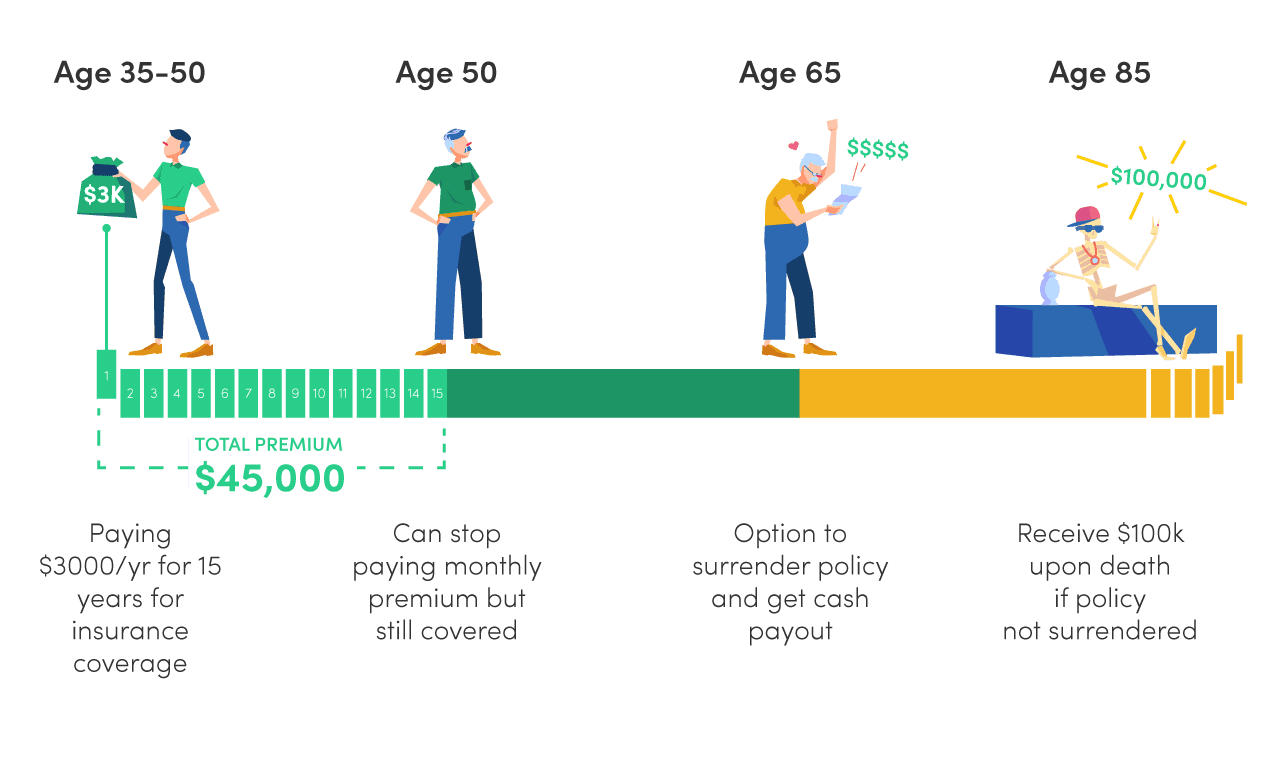

An endowment plan combines savings, investment, and basic life insurance coverage into a single product. You pay premiums over a set period either regularly (monthly/quarterly/yearly instalments) or as a one-time lump sum, and receive a payout at maturity. These plans help you work towards specific financial goals like children's education, retirement savings, or wealth accumulation with built-in protection.

Endowment plans offer guaranteed and non-guaranteed returns:

- Guaranteed returns: Refers to the minimum payout at maturity, regardless of market performance.

- Non-guaranteed returns: Comprise bonuses tied to the insurer's investment fund performance.

Regular premium plans suit salary earners building savings gradually, while single premium plans (typically $5,000–$20,000+) work for those parking lump sums for short-term goals.

Key Components of Endowment Plans

-

Coverage

- Death benefit: Payout to beneficiaries if you pass away during the policy term.

- Total and permanent disability (TPD): Most plans cover this, usually up to a certain age.

- Terminal illness: Some plans provide early payout if diagnosed with a terminal condition.

- Coverage typically lasts for a limited term (10–25 years), though some extend to age 99.

-

Sum assured

- The sum assured is the base amount guaranteed by the insurer.

-

In the event of death or terminal illness during the policy term, the insurer pays out the higher of:

- ~105% of total premiums paid, OR

- The sum assured

- Plus any accumulated declared bonuses.

-

Cash value

- The cash value of endowment plans comprises: guaranteed sum & non-guaranteed bonuses.

-

Non-guaranteed bonuses include:

- Reversionary bonuses; declared annually

- Terminal bonuses; paid at maturity/claim

- Cash dividends, if applicable

The estimated premiums required depends on the total sum assured chosen by customers, subject to health and lifestyle declarations.

Meet our financial advisorsYou don’t need to do this alone. Our advisors are here to help you plan it right. Our advisors aren’t here to push plans. They’re here to understand your life, answer your questions, and help you protect what matters most. Meet our MDRT-qualified specialist and his team. |

|

Types of Endowment Plans in Singapore

| Plan type | What they are | Ideal for | Eligibility | Flexibility | Withdrawals |

|---|---|---|---|---|---|

| Short-term premium endowment | Brief payment tenure (at least 5 years), but minimum 15-year policy term | Savers wanting predictable, near-term payout | 18–70 years old | Early surrender allowed, but payout is reduced | Full withdrawal (reduced payout before maturity) |

| Long-term premium endowment | 10–20+ year policies for goal-based savings or wealth accumulation | Retirement, legacy planning, future expenses | Up to 70 years old | Partial surrender may be allowed after lock-in; full cash-out near maturity | Partial or full withdrawal, but early exit is penalised (most flexible near maturity) |

| Single premium endowment | One-time lump sum at start | Those with cash to park for fixed growth |

18–70 years old Min. single premium from S$5,000–S$20,000+ |

Surrender allowed anytime (penalties apply) | Partial or full withdrawal, but early exit is penalised (payout depends on accrued value) |

| Participating endowment | Policies with guaranteed + bonus returns | Willing to accept some variability for upside | Up to 70 years old; regular or single premium | Bonuses only if declared and policy held to maturity | ✅ Partial or full withdrawal, but early exit is penalised (bonuses may be lost) |

| Traded / Resale endowment | Pre-owned, bought/sold on secondary market | Buyers wanting shorter wait; sellers needing liquidity | Buyer takes over premiums; insurer approval needed | Inherits original plan’s surrender/withdrawal terms Transfer requires insurer approval |

✅ Partial or full withdrawal allowed, but early exit is penalised (follows original plan rules) |

Disclaimer: Product availability and policy terms may change at any time at the insurer’s discretion. Always confirm the latest details directly with the insurer or platform before making any decisions.

Comparison: Top Singapore Endowment Plans

| Plan name | Premium type | Payment period | Coverage period | Payout mode | Cash-out (Surrender) | Resale/Tradable |

|---|---|---|---|---|---|---|

| AIA Smart Flexi Rewards (II) | Regular premium | 5 years |

10 years 15–30 years 20–30 years |

Same as premium payment method | Yes | Yes |

| Income Gro Saver Flex Pro | Single / regular premium | 1, 10–30 years (increment of 5 years) | 10–30 years or up to 120 years old | Lump sum | Yes | Yes |

| Singlife Smart Saver | Single / regular premium | 1, 3, 5, 10, 12, 15, 18, 20, or 25 years | 10–25 years or up to 99 years old | Lump sum | Yes | Yes |

| GREAT Flexi Cashback | Regular premiums | 10, 15, or 20 years | Lump sum (maturity benefit) or guaranteed yearly cash payouts (after end of 2nd policy year) | |||

| Pru Active Saver III | Single / Regular premium | 5–30 years | 10–30 years | Lump sum (maturity benefit) | Yes | Yes |

Don’t Leave Life up to Chance!

Mini-Guide: How to Surrender, Sell, Claim, or Hold to Maturity

| Scenario | What happens | Typical penalty / value | Processing time | Step-by-step instructions |

|---|---|---|---|---|

| Early surrender | Exit anytime for surrender value (often with penalties) | Early years = high penalties, often ~60% less than total premiums paid; penalties reduce closer to maturity | 7–14 business days |

|

| Sell | Transfer ownership to another party at a negotiated price |

Depends on plan’s accrued value, market demand, and platform fees May recover more than via direct surrender value |

2–4 weeks (platform processing + insurer approval) |

|

| Claim / Partial withdrawal | Withdraw part of the policy value while keeping the policy active | Depends on plan’s accrued value and withdrawal amount | 7–14 business days |

|

| Hold to maturity | Complete the policy term and receive full guaranteed amount plus any declared bonuses | No penalty; full maturity value payable | Upon maturity, typically ~2 weeks |

|

How to Apply for Endowment Plans?

Eligibility criteria by endowment plan type

| Plan type | Age | Residency | Min. premium | Medical checks | Other requirements |

|---|---|---|---|---|---|

| Regular premium & single premium | 18–70 years old | Singaporeans, PRs, or approved foreigners | Recurring monthly premium or annual lump sum premium | Rarely needed for low sum assured plans; more likely for high coverage or longer tenure plans | Nominee can be named |

| Resale / Traded |

Buyer: From 18 years old Seller: Any eligible policyholder |

Buyer: Singaporeans, PRs, or approved foreigners Seller: Any policyholder |

Subject to plan | As per original plan | Insurer approval for plan transfer |

Step-by-step application guide

Reach out to our financial advisors at MoneySmart

- Identify suitable endowment plans based on your financial goals

- Review prospective plans’ projected returns and guaranteed values

Review your eligibility

- Age: Typically 18–65 years for regular premium plans; some plans accept entry from babies up to age 70

- Residency: Singapore citizens, PRs, or approved foreigners with valid passes

- Minimum premium: Check if you can commit to the required premium amount (single premium: S$5,000+; regular premium: varies by plan)

- Medical underwriting may be required for high-coverage or long-tenure plans

Prepare required documents

- NRIC/FIN/passport

- Proof of address (e.g., bill, bank statement)

- Latest income document (if requested)

- Completed application form

- Nominee details (optional, if naming beneficiaries)

Undergo underwriting & receive policy illustration

- Guaranteed cash values at different policy years

- Non-guaranteed bonus projections (for participating plans)

- Surrender value schedule

- Premium payment terms and frequency

- Policy exclusions and conditions

Pay your first premium

Depending on your financial capabilities and preferences, you can either choose a single or regular premium.

Use the 14-day free-look period

- Changing your mind and cancelling policy without penalty

- Receiving a full refund of premiums paid (minus medical check costs)

- Re-assess if the endowment plan truly fits your goals

5 Things to Consider Before Buying an Endowment Plan

100% capital guarantee feature

Total Distribution Cost (TDC)

- Refers to the total commission and distribution cost paid to agents or advisors, disclosed in your policy illustration.

- A higher TDC = more premiums go to commissionsrather than the policy’s cash value.

Understanding TDC helps you assess the true cash value of your endowment plan.

Limited pay period options

- Certain plans only require you to pay premiums for a limited period(e.g. 5 years) but extend coverage much longer (e.g. next 20 years).

- ✅ Reduces payment burden with long-term coverage, but annual premiums will be higher.

Surrender value & early exit penalties

- Early surrender almost always means financial loss. Surrender values are typically significantly lower than total premiums paid, especially in the first few years.

- Some policies return just a fraction of premiums if surrendered soon after purchase.

- Penalty formulas vary by insurer, but the “cost of early exit” is almost always steep; always review the surrender schedule before deciding.

Liquidity constraints

- Endowment plans are not designed for flexible withdrawals. Your funds are locked in until maturity, surrender, or resale once committed.

- Some plans allow partial withdrawals, but this reduces future bonuses and the final payout.

- Not suitable if you need regular or emergency access to funds — see our guide on emergency access options.

Pros & Cons of Endowment Plans

| Plan type | Pros ✅ | Cons ❌ | Avoid if ⚠️ |

|---|---|---|---|

| Single premium |

|

Locked funds; early exit penalty | You don't have the lump sum available |

| Regular premium | Gradual, disciplined savings |

|

You dislike long-term payments |

| Participating | Potential bonuses based on insurer’s performance | Bonuses fluctuate annually; returns are not guaranteed | Strictly only want guaranteed returns |

| Traded/Resale |

|

Market risks; inherited terms | Prefer new contracts or less paperwork |

Traded & Resale Endowment Policies: The Secondary Market Guide

| Step | Buyer Action | Seller Action |

|---|---|---|

| 1 | Find a reputable, Singapore-based resale platform (insurer-recognised) | Submit policy for free valuation |

| 2 | Screen listings for term, sum assured, bonuses, remaining premiums | Compare offer to insurer’s surrender value |

| 3 | Make offer, complete KYC (NRIC, proof of address), submit application | Accept offer, complete assignment/ID documents |

| 4 | Review policy schedule, check for loans/encumbrances | Platform submits paperwork to insurer |

| 5 | Sign assignment/transfer forms | |

| 6 | Insurer approves and confirms transfer | |

| 7 | Assume policy ownership, begin payments if needed | Receive funds (usually within 2–4 weeks) |

Note: Cooling-off periods do not apply to resale policies. Transfer typically takes 2–4 weeks after all documents are submitted.

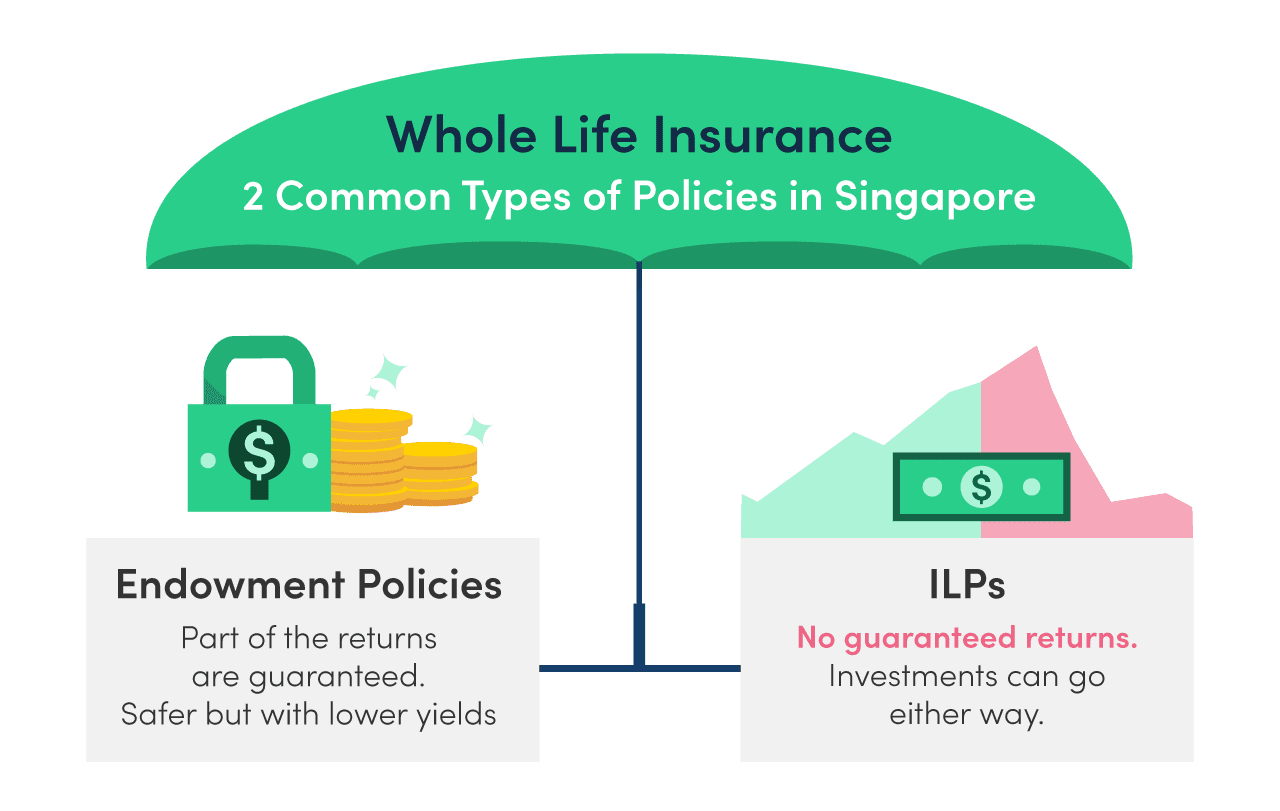

Endowment Plans vs Investment-Linked Policies (ILPs)

Many people compare endowment plans with Investment-Linked Policues (ILPs) when evaluating long-term savings options. However, they come with a distinct set of differences:

| Criteria | Endowment plans | ILPs |

|---|---|---|

| Structure | Savings + life protection + potential bonuses | Investment funds + life protection |

| Returns | Guaranteed sum assured + non-guaranteed bonuses (based on insurer’s participating fund) | Depend entirely on performance of chosen investment funds (e.g. stocks, bonds, etc.) |

| Risk level | Lower risk due to guaranteed cash value providing protection | Higher risk due to fluctuating returns with market performance |

| Flexibility | Limited; locked-in savings until maturity | More flexibility to switch between funds and adjust coverage |

| Best for | Conservative savers prioritising wealth accumulation, goals-based, or capital protection with modest returns | Those comfortable with market risk seeking potentially higher returns |

| Choose if you… |

|

|

For more differences between insurance and investment products, check out our Complete Guide to Life Insurance in Singapore.

Frequently Asked Questions

What is 100% capital guaranteed?

- It is a feature of an endowment plan that provides you 100% of your capital back when your policy matures. For such plans, the payout amount will at least be equal to the total premiums paid—provided you held the policy till its full term.

Are short term endowment plans better than long term ones?

- Yes and no. It really depends on what your financial goals are. Let’s say you’re just looking for alternatives to savings accounts, fixed deposits and even Singapore Savings Bonds (SSBs), short term endowment plans may give you more returns than bank accounts, plus some insurance coverage.

Conversely, for other objectives like saving for your child’s education or retirement planning, a long-term endowment plan may be more apt, but it requires a longer period of commitment and consistent premium payments throughout the policy tenure. What are guaranteed cash values and non-guaranteed bonuses?

- Guaranteed cash values will be the guaranteed amounts of your policy or policies, which excludes the non-guaranteed bonuses you've accumulated during the duration of the policy.

Non-guaranteed bonuses only become guaranteed once declared. This is usually done annually and accumulates on top of your policy's guaranteed cash value over time. What's the difference between participating and non-participating endowment plans?

- Participating plan: Offers both guaranteed cash values and non-guaranteed bonuses (often paid as dividends) based on the performance of the participating fund.

Non-participating plan: Only offers guaranteed returns, with no additional bonuses. The payout is fixed and with no investment influence. How do I know if my endowment plan has a limited pay period?

- You may check with your insurer or read the terms and conditions of your endowment policy. It should state that your endowment plan with a limited pay period means you’ll only have to pay premiums for a limited number of years in exchange for a lifetime’s coverage.

Can I cash out or surrender my endowment plan early?

- Yes, you can “surrender” your policy before maturity, but expect to receive a surrender value less than your total paid premiums in the early years. Know the penalties and timeline before proceeding.

For participating policies, the surrender value typically consists of two parts: a guaranteed portion and a non-guaranteed portion (such as declared bonuses, if any), depending on the participating fund's performance. Are there waivers for endowment plan premiums?

- Yes, many endowment plans offer optional riders that waive future premiums if you're diagnosed with a critical illness, total permanent disability, or similar conditions.

Can I withdraw money from my endowment plan before it matures?

- Some endowments allow partial withdrawals, but doing so will reduce the policy’s cash value upon maturity or result in penalties.

Early policy surrender can also lead to losses, particularly in the initial years of premium payments. How long do endowment plans last?

- It varies across endowment plans. Short-term plans can range between 2 to 6 years whereas long-term ones can range from 10 to 25 years or more.

It depends on personal preference and financial goals. Are there any tax benefits associated with endowment plans?

- No, endowment plans do not qualify for life insurance tax relief.

Can I use my Supplementary Retirement Scheme (SRS) funds to purchase an endowment plan?

- Yes, you can purchase an endowment plan using your SRS funds.

However, do note:- Premiums paid through SRS funds are ineligible for additional tax relief since SRS contributions already receive tax benefits.

- 50% of endowment plan withdrawals from the SRS account are subject to tax, if withdrawn on or after the statutory retirement age prevailing at time of first SRS contribution.

What if I miss my endowment premium payments?

Missed premium payments can cause your endowment policy to lapse or reduce in benefits. Here’s what typically happens:

- Grace period: Most plans offer a grace period (usually 30 days) to make up missed payments without penalty.

- Lapse or auto-reduction: If payment isn’t made after the grace period, your policy may lapse (ending coverage) or enter auto-reduction, where coverage is reduced based on premiums paid.

- Automatic premium loan: Some insurers may use your policy’s cash value to pay overdue premiums temporarily, keeping your policy active.

- What to do: Always contact your insurer promptly if you miss a payment to discuss reinstatement options and avoid losing coverage.

What is an endowment plan, and how does it work?

- An endowment plan is a fixed-term insurance policy that combines basic life protection (death, TPD, sometimes terminal illness) with long-term savings. You pay premiums (regularly or as a lump sum), and at maturity, receive a lump sum payout—comprising guaranteed cash value and non-guaranteed bonuses (for participating plans only). If you pass away during the term, your beneficiaries receive the sum assured plus any declared bonuses.

Plans like AIA Guaranteed Protect Plus, China Taiping i-Secure, and Manulife LifeReady Plus offer different terms and ways to customise cover. What’s the difference between surrender and resale of my endowment plan?

- Surrender: End your plan and receive the surrender value from your insurer (often less than premiums paid).

Resale: Sell your policy on the secondary market to a new buyer, who takes over the plan. You may get more than the surrender value, but this depends on market demand, platform fees, and insurer approval. Not all plans are eligible for resale. Are resale/traded endowment plans safe to buy in Singapore?

- Resale policies are legal, but always check that both the platform and transfer process are recognised by your insurer. MAS doesn’t license most policy resale brokers, so use only Singapore-based, insurer-accepted platforms. Avoid unverified agents or promises of “guaranteed returns.”

Who is eligible for endowment plans in Singapore?

- Most Singaporeans, PRs, and certain foreigners (with valid passes) from age 18–65 can apply for mainstream endowment plans. Resale/traded plans require buyer eligibility checks and insurer approval for assignment. Health underwriting or medical checks may apply for higher sums or certain plans.

What are the main risks of endowment plans?

- Funds in endowment plans are locked in and are not liquid until maturity.

- If you exit your endowment plan prematurely, you’ll likely suffer losses with only around 60–80% of premiums in value returned.

- Non-guaranteed bonuses under participating plans may not meet projections.

- Secondary market risks include paperwork errors and possible platform disputes.

- Its opportunity cost is typically lower returns than ILPs or direct investments.

How do I choose the best endowment plan provider?

Get in contact with MoneySmart’s team of licensed financial advisors to discuss your savings, investment and protection portfolios. They’ll be able to advise on the best endowment plans for your financial needs. Speak to MoneySmart’s team.

What are the most common pitfalls for endowment plans in Singapore?

- Common endowment plan pitfalls include:

- Assuming bonuses are guaranteed.

- Overlooking surrender penalties or assignment paperwork when selling on the secondary market.

- Ignoring policy exclusions or missing medical requirements.

- Using overseas or unrecognised platforms for resale; always check with your insurer first.