Compare the Best Renovation Loan in Singapore 2026

Looking to upgrade your home? A reno loan in Singapore can help you finance everything from minor home improvements to a complete makeover. Discover the best renovation loans in Singapore here and apply instantly with ease.

Refine Your Results

We found 16 Personal Loans for you!

%20(1).png)

%20(1).png)

Sign up via MoneySmart and claim:

Up to S$4,200 Cash OR 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more) T&Cs apply.

Bonus promotion:

- 1.00% cashback of your loan amount

- Only applicable to loans over S$18,000 with a 3 to 5 year tenure

- New-to-card and new-to-loan customers only

T&Cs apply.

Valid till 15 Jun 2026

Sign up via MoneySmart and claim:

Up to S$1,700 Cash via PayNow OR 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more) T&Cs apply.

Bonus promotion:

- Use promo code: MONEYSMT

- Get S$10 FairPrice E-Vouchers

- New-to-Trust customers only

T&Cs apply.

Valid till 30 Jun 2026

Valid till 30 Jun 2026

Sign up via MoneySmart and claim:

Up to S$1,200 Cash via PayNow OR 14,335 SmartPoints (enough to redeem an Apple iPhone 17 and more)

And get your rewards in as fast as 4 weeks!

T&Cs apply.

Valid till 07 Jun 2026

Valid till 30 Jun 2026

Valid till 30 Jun 2026

Valid till 30 Jun 2026

.jpg)

.jpg)

.png)

.png)

.png)

.png)

Disclaimer: At MoneySmart.sg, we strive to keep our information accurate and up to date. This information may be different than what you see when you visit a financial institution, service provider or specific product’s site. All financial products and services are presented without warranty. Additionally, this site may be compensated through third party advertisers. However, the results of our comparison tools which are not marked as sponsored are always based on objective analysis first.

Renovation Loan Comparison in Singapore: Why Use MoneySmart 👉

Should I Take a Renovation Loan in Singapore?

Renovation loans often come with lower effective interest rates (EIR) than personal loans, helping you reduce your total borrowing costs. However, with the lowered interest rates for personal loans in 2026, it might be useful to compare both options to see which loan type is more suitable for you.

Best Renovation Loan Options in Singapore (2026)

| Personal Loan | Interest Rate | EIR | Promotion | Valid until |

|---|---|---|---|---|

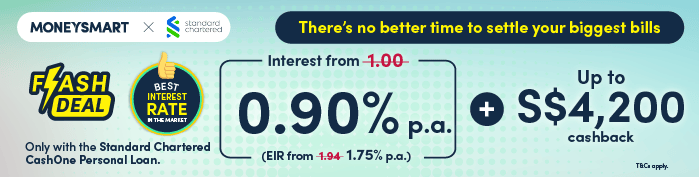

| Standard Chartered CashOne | From 0.90% p.a. | From 1.75% p.a. | Register through MoneySmart to claim:

Up to S$4,200 cash via PayNow or 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more).

Bonus promotion: | 1 Jun 2026 till 15 Jun 2026 |

| Trust Instant Loan | From 1.00% p.a. | From 2.43% p.a. | Register through MoneySmart to receive up to S$1,700 via PayNow or 19,050 SmartPoints—enough to redeem an Apple iPhone 17 Pro Max and more.

Bonus promotion: | 1 Jun 2026 till 30 Jun 2026 |

| UOB Personal Loan | From 1.00% p.a. | From 1.93% p.a. | Sign up through MoneySmart to claim up to S$1,200 Cash via PayNow or 14,335 SmartPoints, enough to redeem an Apple iPhone 17 and other rewards.

Rewards can be issued in as fast as 4 weeks. | 1 Jun 2026 till 7 Jun 2026 |

| Standard Chartered CashOne (Foreigners) | From 0.90% p.a. | From 1.94% p.a. | Register through MoneySmart to claim:

Up to S$4,200 cash via PayNow or 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more).

Bonus promotion: | 1 Jun 2026 till 15 Jun 2026 |

| Trust Instant Loan (Foreigners) | From 1.00% p.a. | From 2.43% p.a. | Register through MoneySmart to receive up to S$1,700 via PayNow or 19,050 SmartPoints—enough to redeem an Apple iPhone 17 Pro Max and more.

Bonus promotion: | 1 Jun 2026 till 30 Jun 2026 |

Choosing the Right Renovation Loan

Each lender meets different renovation needs. For instance:

- HSBC Personal Loan is ideal for large projects requiring long-term financing.

- CIMB Personal Loan works well for borrowers seeking transparent pricing and flexibility on repayments.

- MariBank Instant Loan suits those who need immediate cash with app-based convenience and low entry amounts.

Comparing these side-by-side helps you secure a renovation loan in Singapore that balances affordability and flexibility.

How to Calculate Your Renovation Loan in Singapore

Step 1: Know the loan limit

Step 2: Estimate monthly repayments

Step 3: Factor in fees

Every loan carries fees beyond interest. HSBC comes with a $120 annual fee, waived in the first year. Early or partial repayments incur with a 2.5% penalty, and late payments cost a $120 fee. These costs can add up if you change your repayment plan midway.

Step 4: Plan for funds disbursement

HSBC disburses renovation loan funds within 3–5 business days, credited to your account. Knowing this helps you plan payments to your different renovation contractors accordingly.

💡 Why this matters

Crunch Numbers Before You Borrow

Use our free loan calculator to estimate monthly loan repayments across banks instantly! No guesswork, no surprises—just clear figures to help you decide your next move with confidence.

Renovation Loan Fees & Eligibility in Singapore: What to Know

Renovation Loan Eligibility

To qualify for a renovation loan in Singapore, most banks require:

- Applicants should be Singapore citizens or Permanent Residents aged between 21 and 65 years old.

- Minimum annual income requirements typically start at $30,000, depending on the lender.

- Employment status matters too, and both salaried workers and self-employed individuals can apply if they meet income criteria.

- Some banks may also mandate applicants to be the legal owners of the renovated property.

Common renovation loan fees to expect

- Annual fee: Some renovation loans have annual fees, some don’t. For example, the HSBC Renovation Loan has a $120 annual fee (1st year waived).

- Processing fee: Usually 1% to 2% of the approved loan amount. Some banks waive this during promotional periods.

- Insurance premiums: A few lenders charge a mandatory insurance premium, often 1% of the loan amount, to cover unexpected events.

- Late payment fee: Ranging from $35 to $120 if monthly instalments are missed.

- Early repayment or cancellation penalties: Often 1% to 3% of the outstanding balance if you settle the loan early or cancel it. For instance, the HSBC Renovation Loan imposes a 2.5% penalty of the redemption amount.

- Funds disbursement: Loans are disbursed directly to contractors, sometimes through cashier’s orders that may incur small administrative fees.

How to Apply for a Renovation Loan in Singapore

Check renovation loan eligibility

Applicants must usually be:

- Singaporean or Permanent Resident

- Aged 21–65

- Minimum $24,000 annual income (varies with lender)

- Eligible for both salaried and self-employed individuals

Prepare necessary documents

Having the relevant documents ready helps speed up your loan application.

- Income documents:

- Recent payslips

- CPF Contribution History statements

- Income Tax Notice of Assessment

- Renovation quotations:

- Contractor costs

- Materials involved

- Scope of renovation work

Apply for renovation loan via MoneySmart

Click on the “Apply Now” button of the DBS Renovation Loan (or your preferred renovation loan) on our MoneySmart comparison site to kickstart your digital application.

Remember to use SingPass MyInfo for seamless retrieval of your personal particulars.

Before the application form, you’ll also be directed to fill in our MoneySmart Rewards Form with your email address. This step qualifies you for and helps you track your MoneySmart Exclusive sign-up gift.

Wait for review and approval

Typically, banks will take 1–3 business days to review and approve your loan application.

Approved funds are issued as cashier’s orders directly to your renovation contractor, ensuring proper use for intended renovation purposes.

Other fees involved may include:

- 2% processing charge

- 1% insurance premium

- $5 per cashier’s order after the first free one

Funds disbursement and repayment

Funds are disbursed within a few working days after approval.

Repayments follow fixed monthly instalments over 1–5 years (or up to 7 years if HSBC Personal Loan).

Most banks also typically impose:

- $150 or 2.5–3% early/partial/full repayment penalties, whichever is higher

- ~$100 late fees for missed instalments

What Can a Renovation Loan Cover in Singapore?

🧩 Structural and flooring works

Loans can cover demolition, masonry, flooring, and tiling works. These include laying new tiles, replacing marble or vinyl, or constructing walls for new rooms.

🪑 Carpentry and Built-Ins

Built-in wardrobes, cabinets, and carpentry works are generally covered. Since these fixtures are permanent, they fall under allowable use. Loose furniture such as sofas or tables, however, are not eligible.

🔌 Electrical and plumbing

Renovation loans may fund rewiring, new lighting points, and upgrades to water pipes and sanitary fittings. These essential works improve safety and functionality.

🎨 Painting and finishing

Loans can be used for painting the interior and exterior of the home, plastering walls, and other finishing touches that are integral to the renovation.

❌ What a renovation loan won’t cover

Most banks exclude movable items. Expenses like furniture, home appliances, curtains, or decorative accessories cannot be charged to a renovation loan. If these are part of your budget, you may need to explore personal loans or pay out of pocket.

Renovation Loan vs Personal Loan: Which Fits Your Renovation Budget?

Renovation loan

- Purpose-built for home improvements.

- Requires renovation quotation; funds go directly to contractors.

- Covers works like flooring, carpentry, wiring, painting.

- Lower rates than personal loans, but capped at ~$30,000 or 6× monthly income.

- Fees: 1%–2% processing, insurance premium, early repayment penalties.

Personal loan

- Flexible use, not limited to renovations.

- Can cover loose and movable items like furniture, appliances, and décor.

- Higher limits of up to 8–10× monthly income where funds are disbursed directly to your account.

- Interest rates are often higher than renovation loans.

- Similar processing fees; requires discipline to avoid overspending.

Build Your Dream Home Your Way 🧩🛠️🏡

Don’t let loan limits stop your dream home from coming to fruition. Use a personal loan to flexibly cover your renovation in terms of both structural works and lifestyle upgrades like furniture, appliances, and extras that renovation loans don’t.

How to Plan for a Renovation Loan in Singapore

Planning ahead makes it easier to secure the right renovation loan. By taking a structured approach, you can avoid shortfalls and ensure your loan covers the most essential works.

Assess your renovation budget

Begin by listing all expected costs. Separate structural and built-in expenses (which renovation loans typically cover ✔️) from furniture and appliances (which are usually excluded ❌). This helps you determine how much of your renovation can be actually financed with a loan.

Compare loan options

Different banks offer varying interest rates, fees, and repayment tenures. Renovation loans often come with capped amounts and usage restrictions tied to home upgrades, while personal loans are more flexible but may carry higher effective rates. When comparing, check the loan’s effective interest rate (EIR), processing or disbursement fees, and repayment rules. Some loans allow full early repayment with a fee, while others restrict partial prepayments. Recognising these differences helps you pick the loan that best matches your renovation and financial needs.

Prepare your documents

Before applying, ensure you have all required documents ready. This includes income proof, renovation quotations from your contractor, and identity documents. Preparing these early speeds up the approval process and avoids delays once you decide on a bank.

Build in a 10–15% contingency buffer

Even the best-planned renovation can have unexpected costs. Include a buffer in your budget so you’re not left short if extra work is needed. A renovation loan in Singapore can smooth out these costs, but careful planning keeps your finances manageable.

READ MORE: Should I Use Personal Loans for Renovations?

Key Renovation Loan Aspects To Consider - Public vs. Private Housing

| Criteria | Public Housing | Private Housing |

|---|---|---|

| CriteriaEligibility | Public HousingMust be Singaporean/PR, aged 21–65 Minimum $24,000 annual income Self-employed and salaried employees may qualify No outstanding renovation loans permitted | Private HousingForeigners with valid Employment and Work Passes may qualify, subject to higher income/property criteria |

| CriteriaLoan quantum and tenure | Public HousingUp to $30,000 or 6x monthly income (whichever is lower) 1–5 years tenure | Private HousingVaries by bank Caps are generally higher than HDB limits but still tied to borrower’s income 1–5 years tenure |

| CriteriaInterest rates | Public HousingFrom ~5% p.a. flat interest | Private HousingSimilar range, though some lenders may price higher depending on loan size and borrower’s profile |

| CriteriaLoan usage | Public HousingCovers structural and built-in works: flooring, tiling, hacking (with HDB approval), electrical re-wiring, plumbing, sanitary fittings, built-in carpentry, painting | Private HousingCovers similar renovation works May include external/compound works (e.g. landscaping) for landed property, subject to bank and SLA approval |

| CriteriaExclusions | Public HousingDoes not cover loose or movable items such as furniture, appliances, curtains, or decor | Private HousingDoes not cover loose or movable items such as furniture, appliances, curtains, or decor |

| CriteriaRepayment | Public Housing~1% early full repayment penalty fee Partial repayments not allowed | Private Housing~1% early full repayment penalty fee Partial repayments not allowed |

| CriteriaLate Payment | Public Housing~$30–$120, depending on the bank | Private Housing~$30–$120, depending on the bank |

Frequently Asked Questions About Renovation Loans in Singapore

Who can apply for a renovation loan?

- Applicants must be Singapore Citizens or Permanent Residents, typically aged 21 to 65. Minimum annual income thresholds usually start at $24,000 for renovation loans, and $30,000 for personal loans. Both salaried and self-employed individuals qualify.

What does a renovation loan cover?

- Renovation loans typically fund structural and built-in works such as flooring, tiling, carpentry, plumbing, and rewiring. Furniture, appliances, or decorative item expenses are excluded.

How are interest rates calculated?

- Renovation loan rates are advertised from 1.83% p.a. (or personal loans from as low as 1.60% p.a.), but actual personalised rates depend on income, credit history, and loan tenure. For example, Standard Chartered CashOne offers instant approval and disbursement for existing SCB customers, but final rates are adjusted to the borrower’s profile.

What fees should I expect?

- Common charges include processing fees (1%–2%), late payment fees ($100–$120), early and/or full repayment penalties. Partial prepayments are also often disallowed.

How long is the repayment tenure?

- Renovation loan tenures usually run from 1–5 years. Personal loans used for renovations may range from 6 months to 5 years.

How long does renovation loan approval take in Singapore?

- In Singapore, renovation loan approval from a bank typically takes 1 to 7 working days, assuming all your documents are in order.

The exact timeline depends on the lender, whether you’re already a customer, and how complete your application is. Some banks offer near-instant approval for existing customers via digital channels, while licensed moneylenders can sometimes process applications within just a few hours. How quickly are funds disbursed?

- Most banks disburse funds within a few working days after approval. Existing customers with linked accounts may enjoy near-instant approval and release of funds.

How long does it take to pay off a renovation loan in Singapore?

- In Singapore, renovation loans are typically paid off within one to five years, with most banks capping the maximum tenure at 60 months. These are unsecured loans dedicated specifically for home renovation, so the repayment period is relatively short compared to mortgages. Your choice of tenure affects both your monthly budget and the total interest you’ll pay.

Can a renovation loan in Singapore be paid with CPF?

- No, you cannot use your CPF savings to pay for a renovation loan or cover the costs of home renovation, repairs, or improvements in Singapore. CPF funds are strictly allocated for ertain housing-related purposes—such as buying a property or repaying a mortgage—not for interior renovation or fittings.