Why Trust MoneySmart?

Why Trust MoneySmart?Key Takeaways

Renovation loans are ideal for structural works, but come with strict usage and documentation requirements such as proof of ownership.

For smaller renovation budgets, a personal loan may be more practical despite higher interest rates since they are more convenient and require minimal paperwork.

Take note of the impact your loan choices can have on your TDSR (Total Debt Servicing Ratio). A poor score will impact your eligibility for future loans or mortgage refinancing.

Beyond financing, it’s crucial to align your renovation timeline, contractor payment terms, and loan disbursement schedule to avoid project delays or cash flow issues.

Planning a home makeover but stumped over which loan for home renovation in Singapore makes sense for your wallet? From dedicated renovation loans to flexible personal loans, there’s no shortage of renovation financing options in Singapore and it can be terribly confusing.

Choosing between the two comes down to understanding your renovation needs and objectives. Factors like renovation loan interest rates, personal loan eligibility, and loan flexibility can make or break your budget. Read on to find out how to choose the best loan for your renovation needs in Singapore.

Overview of Loan Options for Home Improvement

What is a renovation loan?

A renovation loan is a dedicated bank loan designed to finance renovations, repairs, or improvements of new and existing homes. Funds are strictly for renovations works only and are directly disbursed to your contractor or ID, based on approval quotes.

What is a personal loan for home renovation?

A personal loan for home renovation is an unsecured loan offering greater flexibility than standard renovation loans. Besides using it for renovation-related expenses like furniture, appliances, and decor, the funds disbursed can also be used for any other purpose, really—without needing to submit renovation quotes or invoices.

Comparison: Renovation Loan vs Personal Loan for Home Upgrades

Let’s compare renovation and personal loans by analysing their strengths and weaknesses to find the best option for your renovation needs.

Criteria | Renovation loan | Personal loan |

|---|---|---|

Interest rates | From 1.85% p.a. (lowest rate as seen on MoneySmart!) | From 1.00% p.a. (lowest rate as seen on MoneySmart!) |

Loan tenure | Up to 5 years | Up to 5 years, sometimes 7 years |

Loan limits | Typically up to 6X monthly income, capped at $30,000 | Typically up to 4X monthly income, or up to 8X monthly income for those with at least $120,000 annual income Mostly capped at $200,000, but varies across banks |

Fund flexibility | Strictly for home renovations Must submit documents like contractor quote or invoice, proof of ownership, HDB or MCST renovation permit | For any purpose |

Income eligibility | Depends on bank Usually $20,000 – $30,000 | Depends on bank Singaporeans/PRs: $20,000 – $30,000 Foreigners: $45,000 – $60,000 |

Upfront fees | May include processing fees (1 – 2%), disbursement fees, or admin charges | |

Loan approval & funds disbursement | May take 3 – 5 working days, subject to document approvals Funds directly disbursed to renovation vendor | Almost instantaneous; within 1 – 2 working days Funds disbursed directly to linked bank account |

In general, although renovation loans have a relatively lower effective interest rate than personal loans, they have stringent usage restrictions and supporting documents like renovation quotes, proof of ownership, HDB or MCST renovation permits (where applicable), and more.

Notwithstanding that, renovation loans are also usually strictly reserved for structural works and built-in renovations, while personal loans offer greater flexibility to cover other renovation-related expenses like furniture, appliances, and other non-structural upgrades.

So depending on the primary purpose of your loan, identifying and prioritising your renovation must-haves and nices is fundamental in deciding whether a renovation loan or personal loan is the better fit.

💡 MoneySmart Tip |

Use trusted online comparison tools like MoneySmart's personal loan comparison to review personalised rates, eligibility, and requirements across major banks in Singapore—helping you make a more informed choice quickly. |

MoneySmart Tip |

While personal loans are generally easier to qualify for than renovation loans due to fewer paperwork requirements and faster approval times, they may come with higher interest rates, so weigh the trade-offs carefully. |

When is a Personal Loan Better for Home Improvements?

While it’s established that renovation loans are designed for home upgrades, there are situations where a personal loan may actually be more practical for financing home improvements—especially when flexibility or speed is key.

Besides the expected funds flexibility, faster approval and disbursement times, and easier-to-manage timelines, what other scenarios might a personal loan be more suitable for home renovations?

For property not in your name

Renovation loans typically require proof of ownership to be approved. This means if you’re renovating a property that isn’t legally under your name, such as your parents’ or partner’s property, you likely won’t qualify. In contrast, a personal loan doesn’t require such requirements, making them a more viable option.

While awaiting TOP or still under construction

In Singapore, a Temporary Occupation Permit (TOP) needs to be obtained by the HDB or private developer from the Building and Construction Authority (BCA) in order for occupants to legally move in or commence renovations—even if certain communal facilities or minor works like playgrounds or swimming pools are still under construction.

For landed properties, the registered property owner or appointed Qualified Person (QP)—usually the architect or engineer—may apply for the TOP directly.

In these scenarios, a personal loan can be useful for preparing pre-emptively for earlier renovation stages, such as buying furniture or planning minor renovation works before full access is granted.

For smaller renovation budgets

Sometimes, if you only need to borrow a few thousand dollars, the interest difference might not justify the hassle of applying for a renovation loan with its restrictions and paperwork. Essentially, the higher interest is arguably offset by the smaller borrowed amount.

MoneySmart Tip |

Personal loans are also especially useful if you’re bundling costs together with other life expenses. For example, couples planning a wedding, buying a home, and renovating simultaneously may prefer a single, large personal loan to cover several big-ticket costs all at once. This helps streamline cash flow and manage repayments more efficiently under one consolidated loan. |

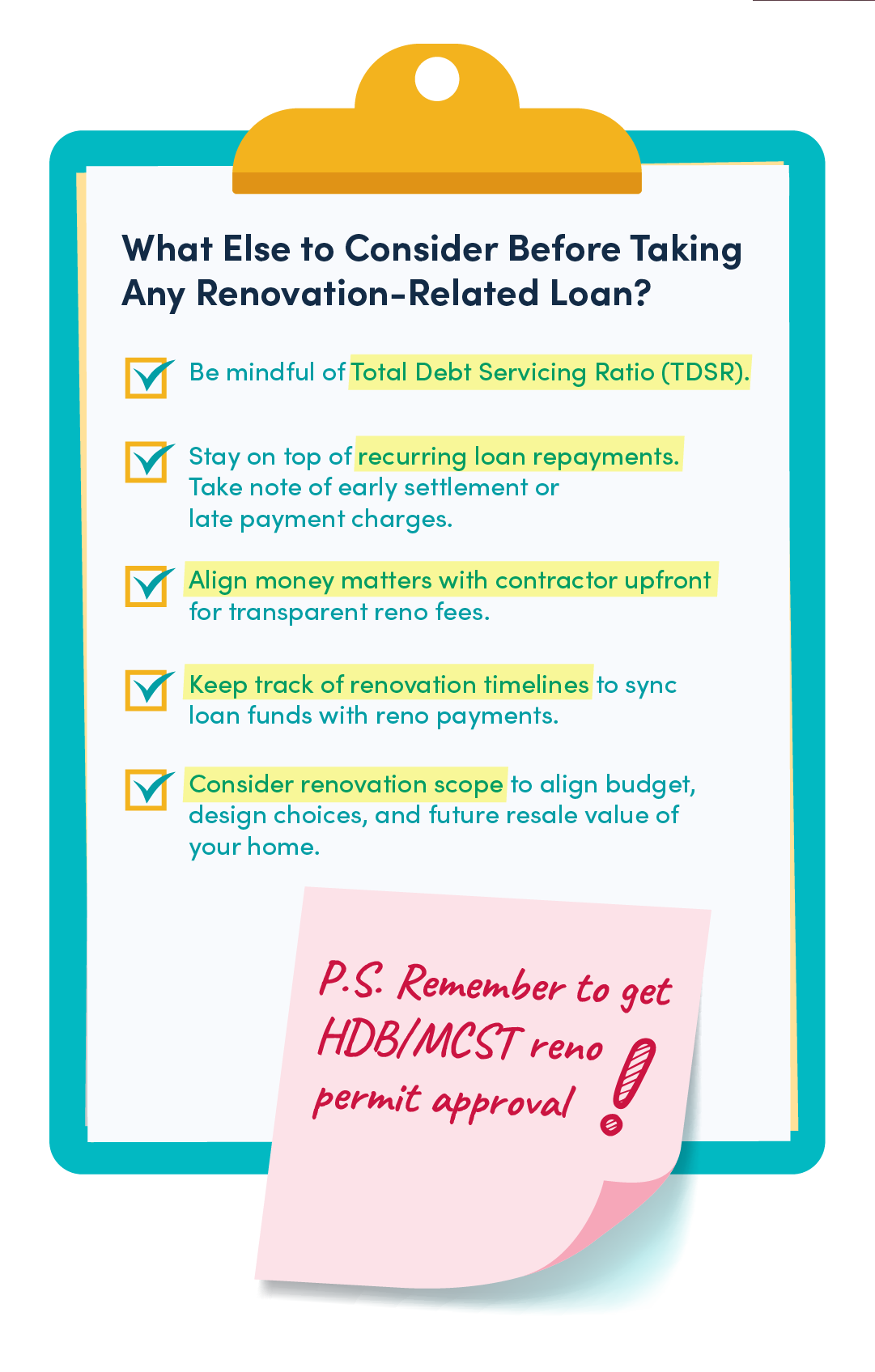

What Else to Consider Before Taking Any Renovation-Related Loan

When deciding on a renovation or personal loan, it’s pertinent to evaluate several components like interest rates, repayment terms, upfront fees, loan amount, funds flexibility, and more. Those aside, what other factors should we consider?

1. Total Debt Servicing Ratio (TDSR) impact

For homeowners with existing home loans, taking a renovation or personal loan will contribute to your Total Debt Servicing Ratio (TDSR). The TDSR is a property framework used in Singapore to calculate how much of your income goes towards repaying debt, like financing a loan.

Currently, the TDSR limit sits at 60%, which accounts for all outstanding debt obligations (e.g. home loan, credit card debts, car loans, etc.). If your total debt exceeds this threshold, it may affect your ability to refinance your mortgage or secure future loans. Thus, it’s important to plan ahead—especially if you intend to switch mortgages, take out other loans, or buy a second and/or subsequent property in the future.

MoneySmart Tip |

Use our in-house TDSR calculator at MoneySmart where you currently stand with your outstanding debt repayments! |

2. Impact on future cash flow

Although renovation loans are typically capped at a reasonable $30,000, renovation costs often exceed this—and this is notwithstanding home insurance or mortgage insurance premiums, moving expenses, new furniture, appliances, and potential post-reno repairs. It’s important to stay mindful of ongoing financial commitments (like recurring repayments) and allocate sufficient buffers to avoid overstretching your budget.

3. Payment details to contractor

In Singapore, banks disburse renovation loan funds either as lump sum or by instalments, depending on the loan product and bank policy. For instance, banks like DBS, OCBC, and Maybank disburse loans in full amounts directly to the contractor upon invoice submission. Meanwhile, other banks may follow drawdown schedules that release funds in tranches as renovation milestones are completed—subjected to bank approval and progress checks.

It’s crucial to clarify and align payment terms with your contractor upfront, because not all contractors accept partial or milestone-based bank disbursements—some may require larger upfront deposits. Matching your loan disbursement schedule to the contractor’s payment terms helps manage expectations and avoid cash flow issues during renovation.

4. Renovation timeline

If your renovation project is staggered (e.g. phase 1: kitchen, phase 2: bathrooms), or if delays like pending HDB/MCST permits or renovation materials are expected, ensure your loan’s tenure and disbursement window matches this schedule. If the renovation timeline isn’t aligned with the loan disbursement timeline, you might be dealt with cash flow issues that impede your renovation’s progress.

5. Early Settlement or late payment fees

If you repay your loan ahead of schedule or—the opposite—are delayed, watch out for early settlement and late payment fees respectively. These amounts vary by lender and loan terms. Always review the fine print before committing to any loan.

Other potential loan fee charges to be mindful of include:

Rejecting loan after accepting letter of offer

Refinance loan with a different bank or licensed moneylender

Upfront fee for loans from licensed moneylender

Partial or full loan repayment

Loan tenure adjustment

Safekeeping of title deed for facility that’s been fully repaid

Request for statements (per year)

Admin fee for third-party insurer for property insurance

6. Renovation scope vs resale value

An often overlooked consideration: many homeowners don’t account for how renovations impact their property’s future resale value.

If you plan to sell within the next 3 to 5 years, carefully weigh the pros and cons of each renovation aspect you’re financing: certain choices like excessive in-built carpentry or polarising design choices may not add value and in fact, have the inverse effect and end up diminishing the resale value of your property—all while you’re still repaying the loan.

💡 Read our other personal loan guides to learn more about where you can use your personal loan. |

(1).png)