Why Trust MoneySmart?

Why Trust MoneySmart?

Key Takeaways

BTO flats and smaller units typically cost less to renovate due to minimal hacking and smaller areas requiring fewer materials.

HDB renovation costs can range from ~$30,000 for a basic 3-room BTO to over $90,000 for a fully customised 5-room resale unit.

Component-level planning is crucial—carpentry and masonry are often the biggest cost drivers, so budgeting by room and feature helps you stay in control.

Personal loans give you more flexibility than renovation loans, especially for appliances and furnishings.

Only engage HDB-approved contractors and check if your renovation requires a permit—starting work without approval may lead to costly penalties.

Why HDB renovations need smarter planning

In 2026, planning your HDB renovation isn't as easy as simply picking tiles and paint colours. With rising inflation, global material shortages, and tighter government regulations, HDB renovation costs in Singapore have climbed noticeably. Whether you're upgrading a newly minted BTO or sprucing up a lived-in resale flat, cost control and a clear financing strategy are more essential than ever.

BTO renovations typically focus on aesthetic upgrades and built-ins, since most essentials are already in place. In contrast, resale flat renovations can involve major overhauls like hacking, rewiring, and replacing aging fittings, making them significantly more expensive. Add in compliance with HDB renovation guidelines, and it’s easy to see how the bills stack up quickly.

This is where smart planning, understanding the real costs, and exploring options like an HDB renovation loan in Singapore come in.

Renovating BTO vs resale flats: Key differences

Aspect | BTO flat renovation | Resale flat renovation |

|---|---|---|

Condition of flat | Brand new, no prior fittings | Pre-owned, may have outdated or damaged fittings |

Scope of work | Mostly cosmetic (e.g. flooring, carpentry) | Structural changes (e.g. hacking, rewiring, plumbing) |

Cost of work | Lower due to lesser work required | Higher due to greater amount of work |

Time required | Shorter renovation timeline | Longer due to demolition and repairs |

Complexity | Lower—no need to undo previous work | Higher—need to dismantle old fixtures |

Customisation | Easier to design from a clean slate | Limited by existing layout unless major works done |

Average HDB Renovation Costs by Flat Type (2026)

Renovation costs can vary significantly based on your HDB flat type, the scope of work, material choices, and whether it’s a brand-new BTO or an older resale unit. A resale renovation typically costs more due to demolition, rewiring, and plumbing upgrades. Here’s a breakdown of average renovation costs in Singapore to help you plan more realistically.

Estimated renovation cost

Flat type | BTO | Resale |

|---|---|---|

3-room | $36,100 to $43,700 | $51,000 to $61,800 |

4-room | $51,000 to $61,800 | $64,300 to $80,300 |

5-room | $67,000 to $82,400 | $84,300 to $97,000 |

Cost breakdown by renovation component

To give you a clearer picture of how renovation costs break down, let’s use a concrete example: a 70 sqm 3-room BTO flat with 2 bathrooms, where every room will be renovated. According to Income, which used estimates based on Qanvast’s renovation calculator, here’s how the costs could stack up by component. This example assumes moderate to extensive works across the main living spaces. Let’s break it down by component:

Hacking involves removing existing tiles, built-in fixtures, or walls to prepare the space for new renovation work. These costs depend heavily on how much you’re removing; more demolition means higher costs.

Room | Description | Estimated cost |

|---|---|---|

Living Room | Dismantling built-ins, light floor hacking | $400 – $700 |

Kitchen | Dismantling cabinets, cooker hob, minor floor hacking | $500 – $900 |

Master Bedroom | Removing old wardrobes, floors for platform bed setup | $600 – $1,000 |

Bathroom | Light hacking for vanity/sink replacement | $100 – $500 |

Masonry refers to wet works, including all tiling, flooring, and constructing bases or wall structures. The more customisation, the higher the cost.

Room | Description | Estimated cost |

|---|---|---|

Living Room | New tiles, touch-ups, bookcase base construction | $1,300 – $3,000 |

Kitchen | Backsplash, base construction for cabinets/appliances | $1,300 – $3,900 |

Master Bedroom | Full construction for platform bed and custom base cabinetry | $2,800 – $8,800 |

Carpentry includes the design and building of custom fixtures like cabinets, wardrobes, and shelving units. It tends to be one of the biggest cost drivers. The more built-in elements you want, the more it adds up.

Room | Description | Estimated cost |

|---|---|---|

Living Room | Built-in TV console and bookcase | $200 – $3,400 |

Kitchen | Full set of customised cabinets and storage solutions | $6,900 – $17,900 |

Master Bedroom | Platform bed, step drawers, built-in storage | $7,500 – $33,700 |

Bathroom | Vanity and top-hung mirror cabinet | $1,200 – $2,100 |

Plumbing covers the installation or relocation of sinks, taps, piping, and other water-related systems. These costs stay fairly modest unless you’re reconfiguring the bathroom or kitchen layout.

Area | Description | Estimated cost |

|---|---|---|

Kitchen | Replacement of 2–3 water fixtures: sink, piping, water heater, filter system | $200 – $500 |

Ceiling and partition work typically includes false ceilings, L-box lighting setups, and non-structural partition walls; these works affect both form and function. In terms of costs, false ceilings and lighting boxes can add up in larger rooms.

Room | Description | Estimated cost |

|---|---|---|

Living Room | Light works on ceilings or wall partitions | $200 – $800 |

Master Bedroom | L-box lighting, partial partition walls | $600 – $1,100 |

Spare Bedroom | Minor ceiling or lighting fixture work | $0 – $600 |

Bathroom renovation usually focuses on upgrading tiles, vanities, and fittings to enhance both function and aesthetics. Upgrades to vanities and mirrors often require both carpentry and plumbing—but full makeovers cost much more.

Description | Estimated cost |

|---|---|

Storage and vanity upgrades, light hacking, minor cabinetry | $1,300 – $2,600 |

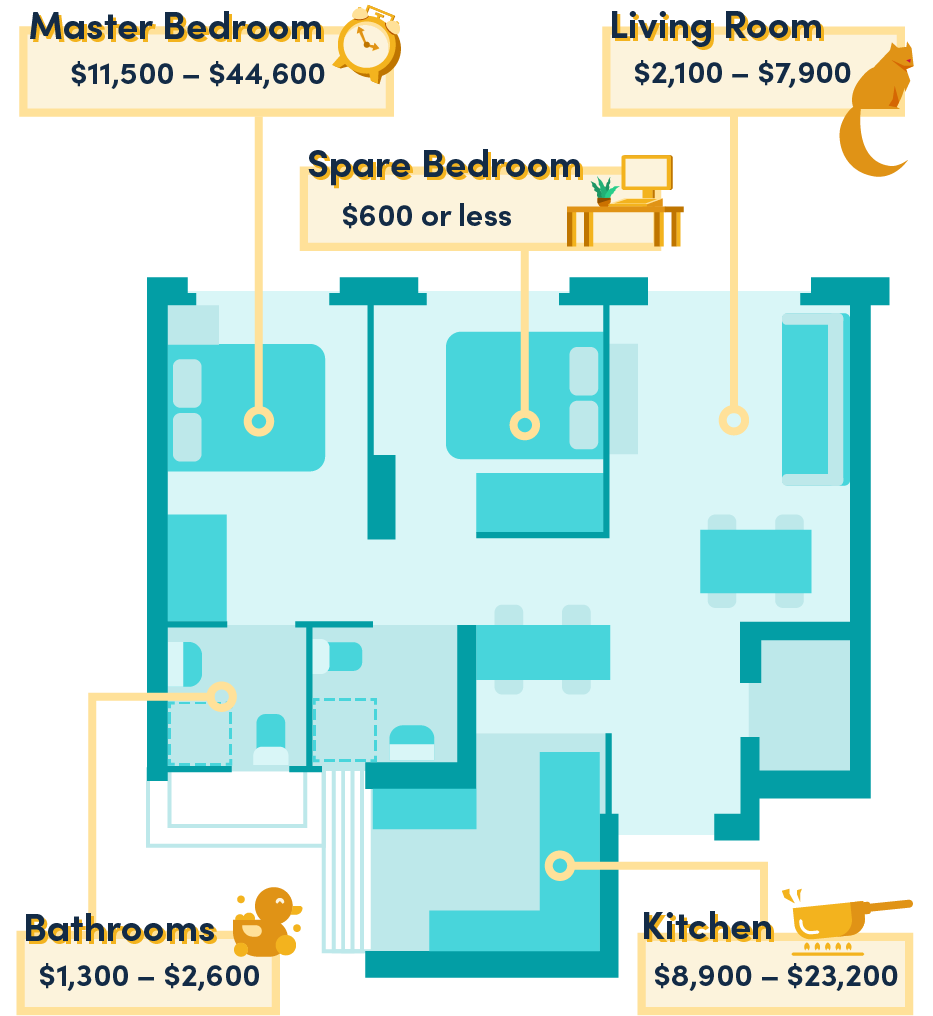

Summary of total estimated costs by room

Room | Estimated cost range |

|---|---|

Living Room | $2,100 – $7,900 |

Kitchen | $8,900 – $23,200 |

Master Bedroom | $11,500 – $44,600 |

Spare Bedroom | $600 or less |

Bathrooms | $1,300 – $2,600 |

Note: These are rough estimates for a moderate renovation of a 3-room BTO flat. Actual costs will depend on materials, design complexity, and contractor rates.

Should I use a renovation loan or personal loan for HDB renovations?

When it comes to HDB renovations, there’s one thing for sure: it’s no trivial sum you need to fork out. If you don’t have enough cash on hand, you’re not alone. Many homeowners in Singapore finance their renovation using a renovation loan or personal loan. Each option comes with its own pros, cons, and ideal use cases—so it’s worth understanding which suits your needs best.

Below, we break down the key differences and benefits of each loan type to help you make an informed decision.

Renovation loans

A renovation loan is specifically designed to fund home improvement works—think hacking, flooring, carpentry, tiling, electrical, and plumbing. Most banks will disburse the funds directly to your contractor.

Pros | Cons |

|---|---|

Fixed monthly repayments | Can only be used for approved renovation works |

Funds disbursed in stages directly to your contractor | May require you to show invoices or contractor quotes |

Loan amounts up to 6x your monthly income or around $30,000 (whichever is lower) | Shorter loan tenure (usually up to 5 years) |

Personal loans

A personal loan offers more flexibility and can be used for both renovation and non-renovation expenses—like buying appliances, furniture, or even covering temporary accommodation while works are ongoing.

Pros | Cons |

|---|---|

Can be used for a wider range of expenses (not limited to renovation) | May tempt overspending due to flexibility |

Higher loan limits (up to 10x your monthly income for some banks) and loan tenures (up to 7 years for some banks) | Loan tenures that are longer mean a higher total interest paid |

No need to show renovation quotations or proof |

Renovation loan vs personal loan at a glance

Feature | Renovation loan | Personal loan |

|---|---|---|

Purpose | Strictly for home renovations | Any purpose, including but not limited to renovations |

Effective interest rate | From 1.83% p.a. (lowest rate as seen on MoneySmart!) | From 1.00% p.a. (lowest rate as seen on MoneySmart!) |

Loan amount | Up to 6x monthly income or ~$30,000 | Up to 10x monthly income. depending on your income level |

Loan tenure | Up to 5 years | Up to 7 years |

Proof needed | Yes (quotes, invoices) | Not required |

Disbursement | To contractor directly | To your personal account |

Best for | Structural and contractor-heavy work | Mixed use: renovation + appliances + anything else |

💡 MoneySmart Tip |

Use trusted online comparison tools like MoneySmart's personal loan comparison to review personalised rates, eligibility, and requirements across major banks in Singapore—helping you make a more informed choice quickly. |

So, should you use a renovation loan or personal loan?

Go with a renovation loan if your renovation is contractor-led and you want lower interest rates with structured disbursement.

Choose a personal loan if you need more flexibility or want to cover extra expenses like appliances, decor, or short-term rent.

Still not sure? Use our renovation loan and personal loan comparison tools to weigh your options and find the best deal for your budget.

You can also read our other personal loan guides to learn more about where you can use your personal loan.

Tips to avoid renovation cost overruns

Renovation costs have a way of creeping up if you're not careful. Between surprise electrical works, tile upgrades, and last-minute add-ons, it’s easy to go over budget. Here are some essential tips to help you keep your renovation spending in check and stay sane throughout the process.

1. Plan your budget—with a buffer

Start with a clear renovation budget—but always build in a 10%–20% buffer for unexpected costs. Whether it’s finding asbestos, upgrading materials, or redoing subpar work, surprise expenses do happen.

2. Get detailed quotations

Always ask for itemised quotes from contractors. This lets you see exactly what you're paying for and makes it easier to compare across vendors. Vague lump sums like “miscellaneous works – $5,000” are red flags.

3. Prioritise needs over wants

It’s tempting to go for designer tiles and custom fittings, but not everything needs a high-end touch. Focus your budget on areas you’ll use daily (like the kitchen or bathrooms), and save on aesthetics where you can. You can also do further cosmetic work at a later date when you have spare cash.

4. Avoid rushing the timeline

Tight timelines can lead to costly mistakes or rework. A rushed job may also incur express fees. Plan ahead, take your time selecting materials, and give your contractor space to work properly. Read more on our guide to renovation and loan timelines.

5. Factor in “hidden” costs

Think beyond just the contractor’s quote. Budget for permit fees, debris removal, appliance delivery, additional power/water bills during renovation, and post-reno cleaning.

6. Work only with licensed contractors

Engage contractors who are HDB-licensed and CaseTrust-accredited. They’re more likely to follow regulations, avoid costly penalties, and provide better workmanship—reducing the chance of expensive rework.

(1).png)