Income Health Insurance

No obligation.

Unbiased Advice

No hard selling, ever

~90mins

Quote delivered to you

⭐⭐⭐⭐⭐ Rated 4.4/5

1.900+ reviews on Google

Income Health Insurance: Integrated Shield Plans (IPs) & MediShield Life

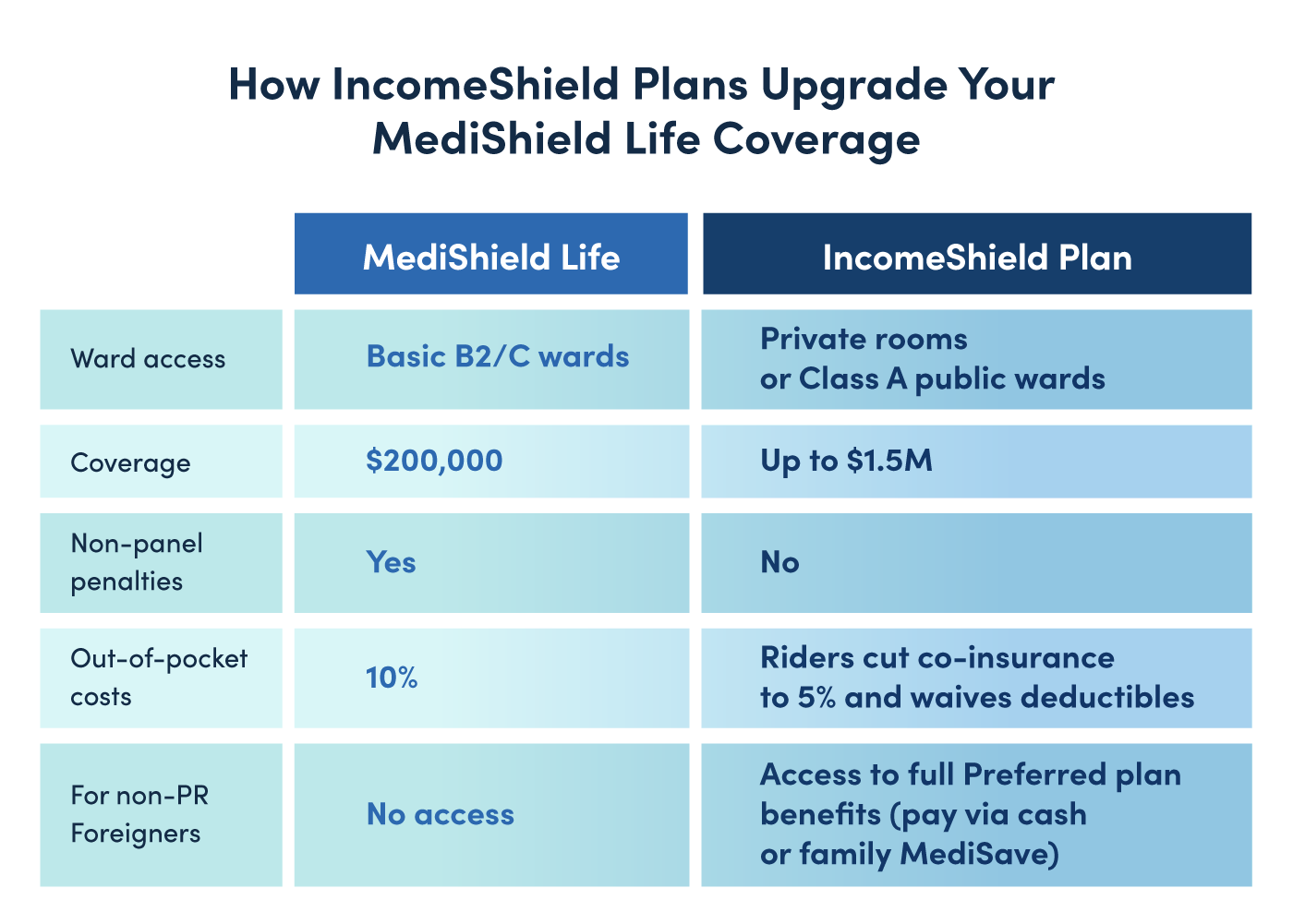

Income's core health insurance comes under its Enhanced IncomeShield series—an Integrated Shield Plan (IP) that layers private insurance coverage on top of MediShield Life (Singapore's basic, compulsory national insurance scheme). This structure gives you higher coverage limits and access to private hospitals beyond what MediShield Life alone provides.

MediShield Life at a Glance

|

Who’s covered |

All Singaporeans & PRs. Foreigners are strictly not eligible. |

|

Coverage scope |

Inpatient stays, day surgeries, and key outpatient treatments (e.g., cancer therapy, dialysis). |

|

Claim limits |

Specific limits per treatment type:

Subject to a maximum policy year limit of $200,000, with no lifetime cap. Also subject to annual deductibles and co-insurance, varying by age and hospital ward. |

|

Exclusions |

Treatments such as cosmetic surgery, most dental procedures (unless due to an accident), infertility treatments, and non-approved drugs. |

Meet our financial advisorsYou don’t need to do this alone. Our advisors are here to help you plan it right. Our advisors aren’t here to push plans. They’re here to understand your life, answer your questions, and help you protect what matters most. Meet our MDRT-qualified specialist and his team. |

|

|

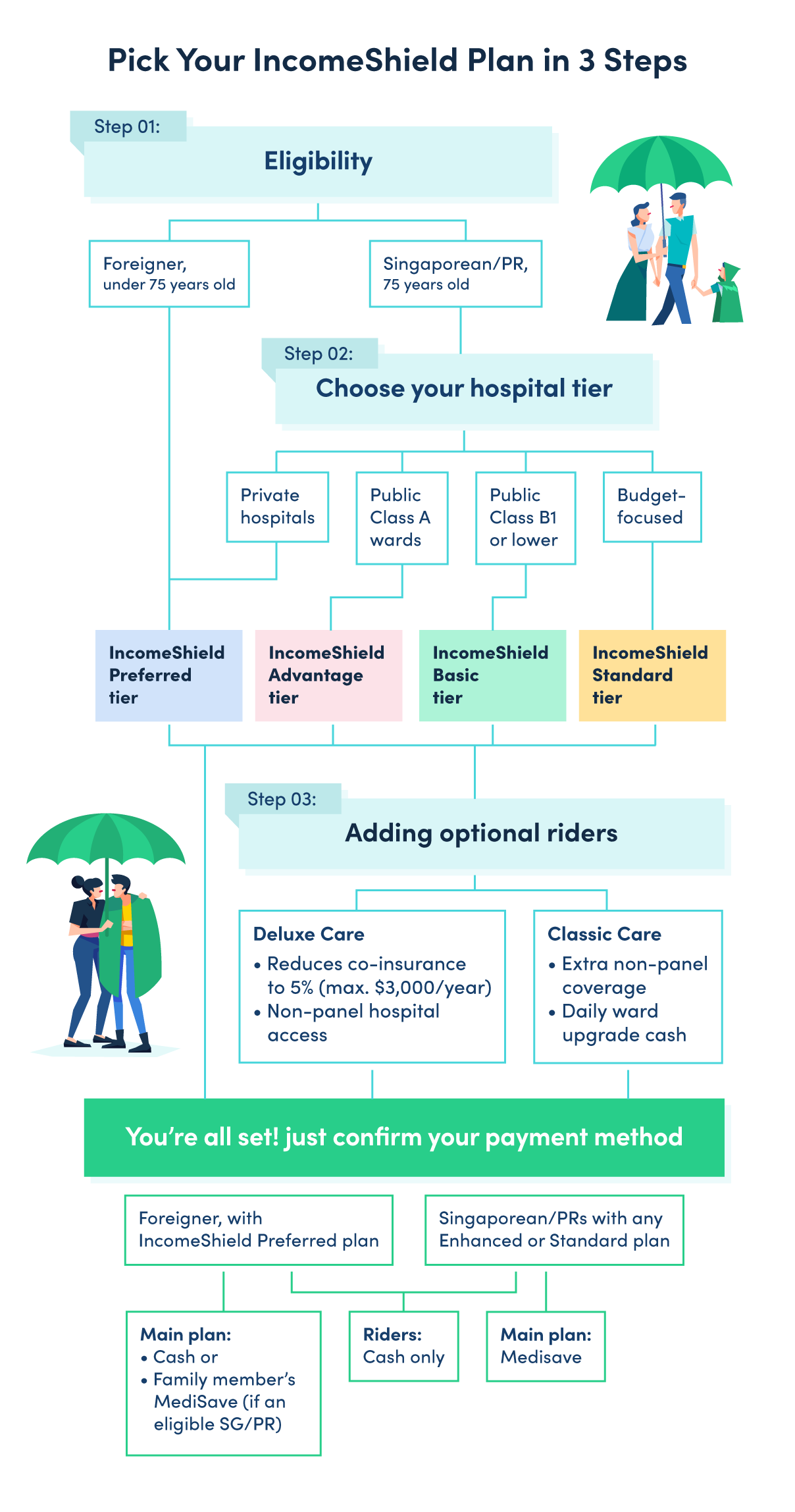

Key Enhancements with IncomeShield

|

Feature / Plan |

Enhanced IncomeShield Preferred |

Enhanced IncomeShield Advantage |

Enhanced IncomeShield Basic |

IncomeShield for Foreigners (Preferred) |

+ Classic Care Rider |

+ Deluxe Care Rider |

|---|---|---|---|---|---|---|

|

Hospital eligibility |

Private hospitals, public Class A wards |

Public Class A wards and below |

Public Class B1 wards and below |

Private hospitals, public Class A wards |

Add-on to main plan |

|

|

Annual claim limit |

Up to $1.5 million |

Up to $500,000 |

Up to $250,000 |

Up to $1.5 million |

Follows main plan |

|

|

Deductible |

Varies by age/ward (e.g., $3,500 for private) |

Waives deductible up to benefit limits |

||||

|

Co-insurance |

10% (reduced with rider) |

10% capped at $3,000/year at panel providers |

5% capped at $3,000/year at panel providers |

|||

|

Eligibility |

Singaporeans/PRs only |

Non-SG citizens, non-PRs only |

Singaporeans/PRs primarily |

|||

|

Pre-existing conditions & exclusions |

Exclusions apply; must declare. Standard Income exclusions apply |

|||||

|

Best for |

Private hospital users wanting maximum coverage (S$1.5M limit, low co-insurance with riders) |

Public hospital Class A users seeking good balance of coverage and premiums |

Budget-conscious public hospital users (Class B1 wards) |

Expats/non-citizens seeking comprehensive standalone coverage equal to Preferred tier |

Those wanting lower out-of-pocket costs and non-panel hospital access |

Those wanting minimum co-insurance (5%) and no non-panel penalties |

MediShield supplement & rider options

|

Feature |

Deluxe Care Rider |

Classic Care Rider |

|---|---|---|

|

Cover deductible & co-Insurance |

Yes, up to benefit limits |

Yes, up to benefit limits |

|

Co-payment Limit |

Lowered from 10% → 5% (capped at S$3,000 for panel clinics; no cap for non-panel) |

Standard 10% co-insurance applies |

|

Extended panel / Non-panel payment |

No additional charges for non-panel clinics |

Up to S$2,000 supplementary coverage for non-panel hospitals |

|

Daily cash benefit |

S$80/day for ward upgrades |

|

|

Additional Cancer Drug Treatment (Outpatient) |

Covers CDL-listed and non-CDL cancer treatments with 10% co-payment (CDL) or 20% co-payment (non-CDL); limits vary by base plan tier |

|

|

✅ Best for |

Minimising out-of-pocket costs at both public and private hospitalisation |

Families or patients seeking additional flexibility and supplementary non-panel coverage |

Key things to note about riders:

- Classic Care and Deluxe Care Riders must be paired with a main IncomeShield plan to mitigate out-of-pocket costs and broaden hospital access.

- Pre-existing medical conditions are also subject to underwriting.

- Premiums can be paid by family members’ MediSave (if the family member is a Singaporean or PR) or by cash.

Why choose Enhanced IncomeShield?

The premium for IncomeShield is relatively lower than average for most of the plan types, even with the riders included.

For Enhanced IncomeShield plans with the Classic Care Rider (age 1 to 75):

- The Basic and Advantage plans are very competitively priced, ranging from $112—$654.

- However, the Preferred plan is relatively more expensive, ranging from $369—$5,460.

For Enhanced IncomeShield plans with the Deluxe Care Rider (age 1 to 75):

- The Basic and Advantage plans are fairly affordable, ranging from $168—$2,529.

- Meanwhile, the Preferred plan starts at a markedly higher rate of $850—$10,862.

IncomeShield’s annual coverage limits scale based on the level of ward or hospital access you choose. In practical terms, this means:

- Enhanced C plan: Annual coverage starts from around $150,000.

- Enhanced Basic (Class B1 wards): Higher annual limit than Enhanced C.

- Enhanced Advantage (Class A wards): Significantly higher policy year limit.

- Enhanced Preferred (Private hospitals): Up to $1.5 million per policy year.

These limits represent the maximum total amount claimable, regardless of whether you claim across hospitalisation, surgery, or other covered treatments.

Enhanced IncomeShield’s pre- and post-hospitalisation coverage is typically much more extensive when treatment is received through approved providers:

- Pre-hospitalisation treatment: Up to 180 days before admission

- Post-hospitalisation treatment: Up to 365 days after discharge

These timeframes facilitate continued, subsidised patient care for consultations, diagnostic tests, and follow-up treatment related to a covered hospitalisation.

Enhanced IncomeShield offers comprehensive coverage without fixed dollar sub-limits, where claims are paid according to the actual bill amount. “As charged” treatments include:

- Inpatient hospitalisation expenses

- Surgical procedures

- Certain specialised outpatient treatments

However, these are not unlimited. Claims are still subject to:

- Your plan’s policy year limit

- Deductible and co-insurance requirements

- Any policy terms or exclusions

IncomeShield Exclusions: What’s Not Covered

Disclaimer: This is a non-exhaustive list of common exclusions. Always check with your policy wording or Income directly if you’re unsure whether a specific treatment or service is covered, especially before proceeding with major medical procedures.

|

Hospital admission & pre-existing conditions |

Outpatient & general medical services |

Birth defects, pregnancy & fertility |

|

|

|

|

Mental health & substance abuse |

Cosmetic & elective procedures |

Dental treatment |

|

|

Dental procedures are excluded unless accident-related and require inpatient care |

|

Alternative & complementary medicine |

High-cost & specialised medications |

Medical Equipment & Experimental Treatments |

|

Traditional Chinese medicine (TCM), chiropractic, acupuncture, homeopathy, naturopathy, and related treatments are not covered. |

|

|

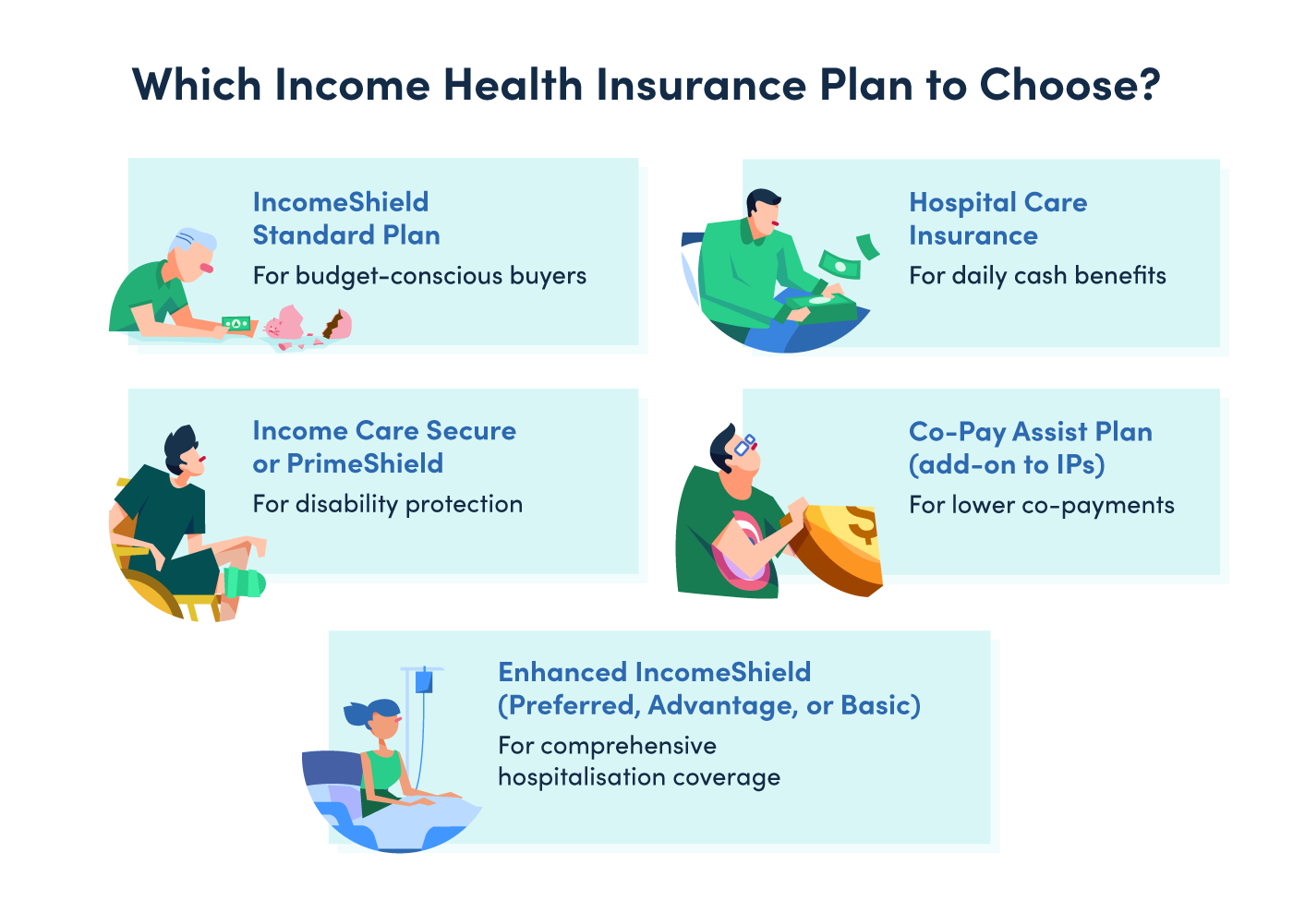

Other Income Health Insurance Plans

Income Care Secure & Secure Pro

These are CareShield Life supplements that provide:

- Enhanced disability coverage + guaranteed $5,000 payout (if loss of ≥ 2 Activities of Daily Living)

- Up to 600% increase in support benefits

- Lump sum death benefit

- Can pay premiums via MediSave

Hospital Care Insurance

Features a daily hospital cash plan:

- Up to $200 per day for hospitalisation (including Covid-19)

- Up to $600 per day for ICU stays

- Day surgery coverage

- Up to $750 for emergency outpatient expenses

- Up to $500 for ambulance costs

Co-Pay Assist Plan

A group insurance policy only available for public officers covered under the Comprehensive Co-payment Scheme (CCS). It reduces out-of-pocket costs by covering:

- Co-payment by up to 7.5% for employees and up to 20% for dependents

- Inpatient and outpatient treatments, including medical expenses incurred during overseas job postings

Premiums can be paid via payroll deduction in the form of cash/cheque for the first year.

IPs for public officers

Income Corporate & Group Health Plans

|

Category |

Plan |

Coverage |

|---|---|---|

|

Health & Medical |

Employees FlexCare |

Customizable group health plan with flexible coverage tiers |

|

WorkMedic |

Outpatient and hospitalization coverage |

|

|

Group Hospital and Surgical Insurance |

Hospitalization, surgeries, ICU stays |

|

|

Personal Accident |

Group Personal Accident |

Accidental death, disability, and medical expenses |

|

Short-term Group Personal Accident |

Temporary PA coverage for projects or events |

|

|

Group Personal Accident for MOE Personnel |

PA coverage for Ministry of Education staff |

|

|

Life Insurance |

Group Term Life |

Death and total permanent disability coverage |

|

How to apply for your Health Insurance plan

Applying for a Health Insurance plan through MoneySmart

Reach out to our expert advisors

Submit questionnaire

Apply & purchase health insurance

Not Sure Which Shield Actually Shields You? 🛡️

How to Make an IncomeShield Health Insurance Claim?

Common claims mistakes to avoid

- ncomplete documentation (signatures, bills, reports)

- Late filing (past Income’s deadline)

- Panel confusion (verify your provider's panel status)

- Outdated medical disclosures

- Non-English documents without certified translations

|

Panel vs non-panel hospital claims |

Rider & supplement claims |

Expat and foreigner claims |

|

Panel hospitals: Submitted as electronic claims by hospitals for faster processing and lower out-of-pocket costs Non-panel hospitals: Submitted manually with supporting documents like medical bills and invoices. |

Riders (Deluxe Care, Classic Care) are processed automatically with your main claim—no separate submission needed. Just verify your co-insurance cap and non-panel coverage match your hospital choice and to include all supporting documents. |

Submit copies of:

|

Verify your hospital’s panel status

If panel, submit e-claims. If non-panel, submit manual claims.

For panel provider claims (e-submission)

Once you’ve confirmed your hospital is on the panel, just take note of:

- To receive statement showing covered and non-covered amounts

- Claims processing takes 5–10 business days

- Only need to pay co-insurance/deductible at discharge

Non-provider claims (manual submission)

For non-panel hospitals, you’ll need to submit claims by yourself.

- Download the claim form from Income's website or collect at a branch

- Gather supporting documents:

- Original bills and receipts

- Discharge summary with diagnosis details

- Referral letter (if applicable)

- Medical/lab reports (if requested)

- For expats: passport, work/visit pass, and certified English translations of non-English documents

Submit claim within deadline

Track claims progress

Once submitted, monitor claim’s status through Income’s online portal or by calling their helpline.

Expect processing to take between 2–4 weeks for straightforward claims, or longer for claims requiring extra documentation or medical review.

In case of rejection, appeal!

In the event your claim is rejected or partially denied, remember you have the right to appeal with additional information and documents!

💡 Always keep copies of everything submitted, including submission receipt or tracking number.

IncomeShield Premiums, Payment Options & Cost-Saving Tips

Singaporeans and PRs:

Foreigners / expats:

Do note that non-citizen foreigners are not eligible for MediShield Life, so the plan will operate as a standalone private IP.

How to pay with MediSave?

- Apply for IncomeShield with the help of our licensed financial advisors.

- Select CPF/MediSave payment at checkout (main plan only).

- Set up auto-deduction (GIRO) or pay once.

- For expats/mixed families, use an eligible family member's MediSave or pay cash.

IncomeShield cost-saving tips

- Right-size your coverage: Select an IncomeShield plan tier that aligns with your typical hospital coverage preference. Avoid over-insuring for private hospitals if you’re happy with public wards.

- Review riders carefully: Only add riders like Deluxe Care (reduces co-insurance to 5%, removes non-panel penalty) or Classic Care (extra cash benefits, non-panel cover) if the extra out-of-pocket protection justifies the added premium cost.

- Reassess annually: As premiums increase with age, re-evaluate yearly if your current tier still fits your budget and hospital preferences.

- Compare at renewal: During policy renewals, don’t shy away from the idea of “shopping around” for other plans. Other IPs may offer better rates or coverage for your profile.

|

Explore other products from Income Insurance Singapore

FAQs About Income Health Insurance in Singapore

Can expats or foreigners get Income health insurance?

Yes. Foreigners (non-citizens, non-PRs) can apply for IncomeShield Preferred for Foreigners, which covers:

- Private hospitals and public Class A wards

- Optional riders (Classic Care, Deluxe Care) to reduce out-of-pocket costs

Premiums are payable via cash or a Singaporean/PR family member's MediSave (within CPF limits). Riders are cash-only.

What's the difference between the main Income health insurance plan and its riders?

Main plan: Core coverage for hospitalization, surgery, and major outpatient treatments.

Riders (add-ons): Optional enhancements that reduce co-insurance and add non-panel hospital access:

- Deluxe Care: Lowers co-insurance to 5% (capped $3,000 per year), covers non-panel penalties

- Classic Care: 10% co-payment cap ($3,000 per year), non-panel flexibility

How do I upgrade or switch my Income health insurance plan?

To upgrade or switch your plan:

- Review your hospital preferences and coverage needs

- Check eligibility (SG/PR can access all tiers; foreigners only Preferred for Foreigners)

- Submit change form during renewal (30 days before) or mid-term

- Undergo medical underwriting for upgrades

- New coverage takes effect once approved

Do also note the following caveats:

- Upgrades to higher tiers require health assessment; new conditions may be imposed.

- Downgrades don't require fresh health checks. However, exclusions at inception are maintained.

- Riders can only be changed at renewal

- 12-month waiting period may apply to upgraded benefits and pre-existing conditions

Can I use MediSave or CPF to pay my premiums?

- Singaporeans/PRs: You can use MediSave to pay for main plan premiums, up to CPF Board limits. Riders must be paid in cash.

- Foreigners: Main plan premiums can be paid by cash, or via a Singaporean/PR family member’s MediSave (within CPF limits). Riders are strictly cash-only.

For an in-depth walkthrough, refer to our CPF and MediSave insurance guide.

Which hospitals are considered “panel” and why does it matter?

Panel hospitals partner with Income for direct medical billing and preferred rates. Using them means:

- Lower out-of-pocket costs

- Claims will be e-filed, as advised by the hospital’s business office prior to admission

- Capped co-insurance (especially with riders)

Non-panel hospitals may incur higher charges unless you hold the Deluxe Care rider.

How do I make an Income health insurance claim? What documents are needed?

Panel hospitals:Claims will be e-filed as advised by hospital admin

Non-panel/manual claims:

- Completed claim form (from NTUC Income website)

- Original bills and receipts

- Hospital discharge summary and medical reports

- For expats: Passport, work pass copies, certified English translations (if needed)

How can I apply for Income health insurance plans?

The easiest way to apply is to get a personalised review from our team of MDRT-licensed financial advisers. Whether you’re a Singaporean, PR, or expat, they’ll assess your current health insurance portfolio, explain your options, and help you choose the right Income plan for your needs.

Request a free health insurance review and our experts will guide you through the application process, paperwork, and any required medical checks.Are there waiting periods or exclusions for pre-existing conditions?

Yes. Pre-existing medical conditions declared at application may be excluded entirely, subject to loading (higher premiums), or waived if properly disclosed (subject to underwriting assessment). Upgrades to higher tiers trigger new medical underwriting and may exclude recently developed conditions.

What happens if I want to downgrade or remove a rider?

You can usually downgrade during renewal or mid-term without fresh health checks. However:

- You may lose certain benefits

- Any health conditions developed since policy start may face new exclusions

Check with our MoneySmart financial advisors or Income directly for mid-term downgrade availability