Why Trust MoneySmart?

Why Trust MoneySmart?Key Takeaways

Most people can apply online in minutes. Many banks offer digital applications with Singpass/MyInfo, allowing for quick preliminary approval if you meet the eligibility criteria.

Check eligibility before applying. Most credit cards require a minimum annual income of $30,000 for Singaporeans and PRs, with higher thresholds for foreigners or certain card types.

Choose a card that fits your spending habits. Cashback, miles, and rewards cards all offer different benefits depending on how you typically spend.

Prepare your documents in advance. Having your NRIC, income documents, or MyInfo ready can help speed up the application process.

Promotions may offer extra value. Applying during promotional periods could unlock sign-up bonuses such as cash gifts, points, or miles—usually with a minimum spend requirement.

Applying for a Credit Card in Singapore: Quick Overview

Applying for a credit card in Singapore is fast and convenient. Most banks offer fully online applications with instant approval options, so you can often apply and receive a decision within minutes.

There is also a wide range of cards suited to different needs and lifestyles:

Cashback cards: Earn direct cash rebates on everyday spending like groceries, dining, or transport.

Miles cards: Let you accumulate air miles for flights or hotel stays.

Rewards cards: Offer points you can redeem for shopping, vouchers, or travel perks.

Premium cards: Provide lifestyle privileges such as lounge access and exclusive dining offers.

Many banks also use MyInfo to auto-fill your details, making applications even quicker—though final approval still depends on income and credit checks.

Eligibility and Requirements: Who Can Apply for a Credit Card in Singapore?

Understanding whether you qualify is an important first step before applying for a credit card in Singapore. Below is a quick overview of the key eligibility requirements for Singaporeans, PRs, foreigners, and special cases such as self-employed applicants and students.

Main credit card eligibility criteria

1. Minimum age

You must be at least 21 years old to apply for a principal credit card with any major bank in Singapore.

2. Minimum annual income

Singapore Citizens & PRs: Most major banks typically require a minimum annual income of $30,000.

Foreigners: The threshold is higher—commonly $40,000 or more per year (exact amount depends on the bank).

These income minimums apply across leading banks, but always check if the policy varies for the card you’re eyeing.

3. Employment type

Salaried Employees: Provide recent payslips or IRAS Notice of Assessment to prove income.

Self-Employed/Commission-Based: Generally, banks will accept your most recent Notice of Assessment from IRAS. Some may also ask for bank statements to supplement your application.

Students: For those under 21 or who do not meet minimum income, banks typically offer special student credit cards or supplementary cards (with a lower credit limit and separate eligibility criteria).

4. Local residential address

A Singapore residential address is required; PO boxes or overseas addresses are usually not accepted.

5. Credit record

Banks will run a basic credit check through local bureaus. A poor credit history or recent defaults can result in rejection, even if you meet other criteria.

Special cases

Secured Credit Cards: If you have low or no declared income, or if your credit score is less than ideal, a secured credit card may be an option. These are issued against a fixed deposit placed with the bank and have less stringent income requirements.

Supplementary Cards: Typically available to the immediate family of the main cardholder; eligibility (including age) can be as low as 18 depending on the bank’s policy.

Students and Young Adults: Student credit cards tend to have lower annual income requirements (or waive them altogether) but may come with lower credit limits and fewer perks.

Example: Typical bank requirements at a glance

Applicant type | Minimum age | Minimum annual income | Other key criteria |

Singaporean / PR | 21 | $30,000 | Local address, good credit |

Foreigner | 21 | $40,000+ | Valid work pass, local address |

Student (SG/PR) | 18* | As low as $0 | Student status; lower limit |

Supplementary (Family) | 18* | N/A | Main cardholder’s eligibility |

Self-Employed | 21 | $30,000 (SG/PR) | NOA, bank statements |

Secured Card Candidate | 21 | No minimum | Security deposit required |

*Student and supplementary card eligibility may start from age 18, depending on provider.

Understanding these requirements helps you avoid unnecessary rejections. Always check card-specific criteria before applying, as banks may update policies or run promotional exceptions.

Compare the Best Credit Cards in Singapore (2026)

Here’s a quick table comparing popular credit cards in Singapore for 2026, highlighting eligibility, annual fees, key features, and promotions to help you find one that suits your needs.

Card and bank | Key features | Welcome promotion* | Annual fee (waiver) | Minimum income (SG and PR/Foreigner) | Best for |

Up to 6% cashback on shopping & transport, 0.3% on all spend | — | $196.20 (first year waived) | $30,000 / $45,000 | Young adults, digital payments | |

Up to 3 miles per S$1 regional spend, 1.4 miles on local spend, no min. spend/cap | — | $261.60 (first year waived) | $30,000 / $40,000 | Frequent travellers, big spenders | |

10X points on online /shopping; wide reward flexibility | $430 Cash/6,140 SmartPoints** (valid till 14 Mar 2026) | $196.20 (Waiver available) | $30,000 / $42,000 | Online shoppers, families | |

Up to 6% cashback: dining, fuel, groceries, bills | $230 Cash/3,500 SmartPoints**

(valid till 16 Mar 2026) | $196.20 (2 years waived, spend $10,000/year to waive after) | $30,000 / $45,000 | Families, daily essentials | |

10X points (4 miles/2.5% cashback) on online & contactless spend (till 31 Mar 2026) | $400 Cash/6,140 SmartPoints** (valid till 31 Mar 2026) | $0 | $30,000 – $40,000 (SG/PR with ≥$50,000 TRB^) / $65,000 | Fee-free rewards, online payments | |

8% cashback: groceries, dining, transport (5 preferred categories) | — | $196.20 (3 years waived, spend $12,000/year to waive after) | $30,000 / $60,000 | Households, broad spenders | |

Flat 1.6% cashback, no min. spend/cap | $430 Cash/6,140 SmartPoints** (valid till 14 Mar 2026) | $196.20 (first year waived) | $30,000 / $42,000 | Simple, all-purpose cashback | |

Up to 10% cashback on McDonald’s, Grab, Shopee, SimplyGo and more | — | $196.20 (first year waived) | $30,000 / $40,000 | Consistent spenders, daily bills | |

Up to 10% cashback on dining, streaming, transport | — | $91 (waived if spend >$10,000/year) | $30,000 / $90,000 | Foodies, commuters, streamers |

*Promotions marked ** are MoneySmart exclusives, accurate at the time of writing. Offers may change—check card pages for the latest promotions.

^ TRB: Total Relationship Balance, the combined value of deposits, investments, and other eligible accounts you hold with the bank.

Annual fees and waiver policies vary by card. Some waive the first year automatically, while others require a minimum annual spend for future waivers. Most cards also require a $30,000 minimum annual income for Singaporeans and PRs, with different thresholds for foreigners or seniors.

Card benefits can also differ significantly. Some, like HSBC Revolution, have no annual fee and flexible rewards, while others—such as UOB One—offer higher cashback if you meet monthly spending tiers. To explore options based on your spending habits, browse credit cards by benefit (travel, dining, shopping, etc).

How to Apply for a Credit Card: Online and Offline Methods

Step 1: Choose the right credit card

Start by reviewing your needs—are you looking for cashback, air miles, or versatile rewards? Compare cards based on your spending habits, eligibility (such as age and income), and current promotions. Using comparison tools or checking official bank pages can help you find the latest offers and ensure you meet the card’s requirements before applying.

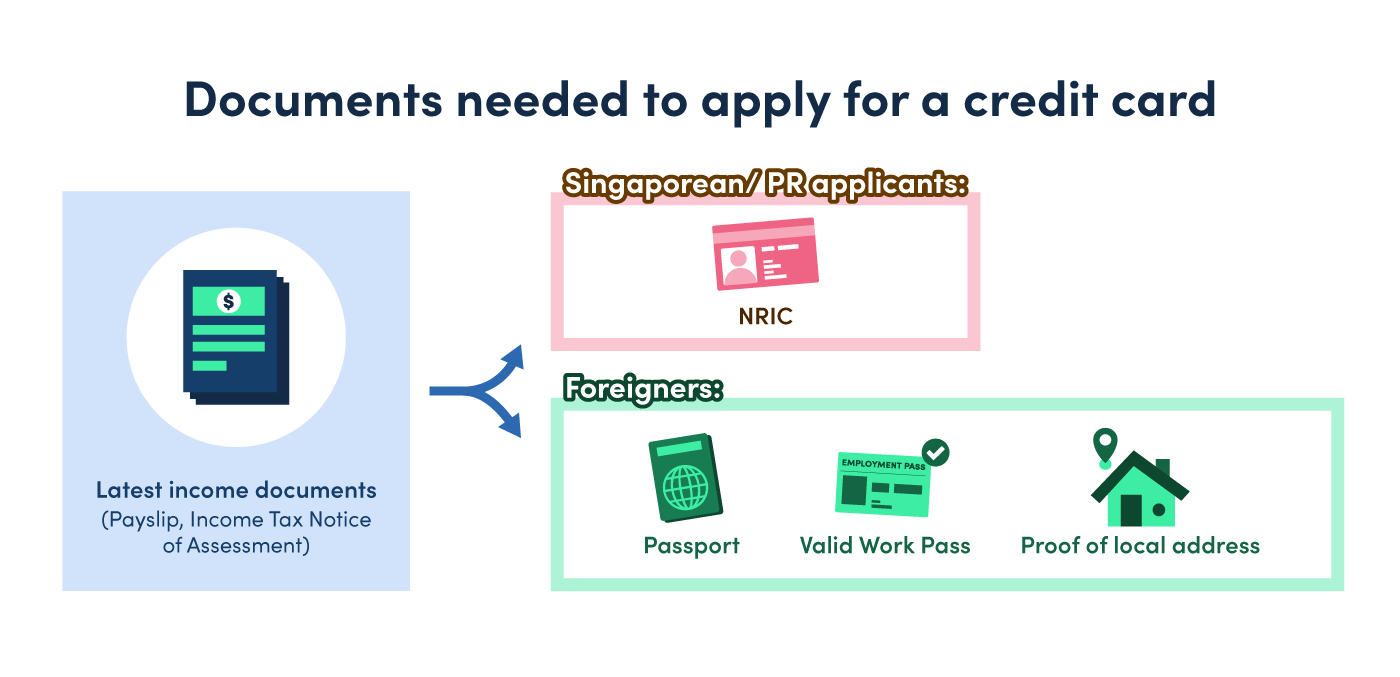

Step 2: Prepare required documents

Generally, you should have these documents ready to speed up your application:

Most banks accept digital uploads, but double-check file size and format requirements on the application page.

Step 3: Apply online

Visit your chosen bank’s credit card page and click “Apply now.” Log in with Singpass/MyInfo if available to auto-fill your details and speed up the process.

Complete the application form, upload any required documents, and submit it. You’ll usually receive an on-screen or email confirmation. Existing customers may also be able to apply directly through their bank’s app or digital banking platform.

How instant approval works

Many banks offer instant approval if you meet the criteria and apply using MyInfo, so you may receive a preliminary decision within minutes. Final card issuance is still subject to backend checks, and additional documents may sometimes be required.

Step 4: Apply offline

Prefer in-person? You can still apply at any participating bank branch:

Collect a credit card application form at the branch.

Fill it out with your personal and financial details.

Submit photocopies of the required documents along with your application.

The bank staff will verify your documents and notify you of the next steps.

Note: Processing time may take longer (typically a few working days) compared to online applications.

Step 5: Track your application status

Online applicants: Most banks email an application reference number. Use this on the bank’s website to check your status.

Offline applicants: Call the bank’s hotline or return to the branch with your reference number for updates.

Expect an email or SMS update on your application outcome. If approved, your card will be mailed to your registered address.

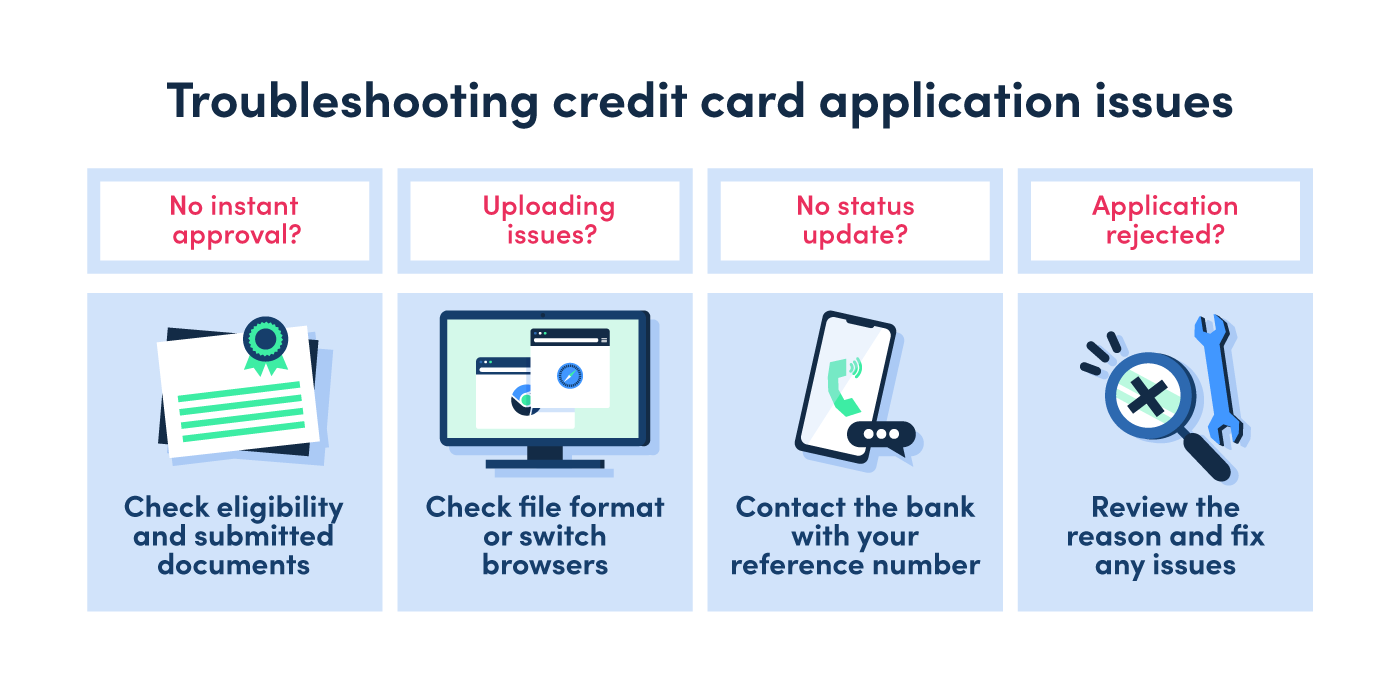

Troubleshooting common application issues

If you’re facing issues applying for a credit card in Singapore, here are some troubleshooting strategies to help.

Latest Credit Card Promotions and Sign-Up Bonuses (2026)

Here are some of the latest credit card promotions in Singapore as of March 2026. As terms and spend requirements may change, check each card’s page for the latest details before applying.

Credit card | Annual fee | Promotion | Spend requirement | Valid till |

$0 | $400 cash or 6,140 SmartPoints via MoneySmart MoneySmart March Gold Rush Madness: Stand to win 1 of 12 dazzling 10g gold bars worth over $2,300 each | $500 from approval date to end of next calendar month | 31 Mar 2026 | |

$196.20 (waiver available) | $430 cash or 6,140 SmartPoints via MoneySmart MoneySmart March Gold Rush Madness: Stand to win 1 of 12 dazzling 10g gold bars worth over $2,300 each | $500 within 30 days of approval | 14 Mar 2026 | |

$196.20 (first year waived) | $180 Cash or 2,800 SmartPoints (sufficient to redeem a Sennheiser Accentum Plus Wireless Headphone) | $500 within 30 days of approval | 19 Mar 2026 | |

$196.20 (waived for 2 years; subsequent waiver with $10,000 annual spend) | $230 cash or 3,500 SmartPoints via MoneySmart | $400 within 30 days of approval | 16 Mar 2026 | |

$196.20 (first year waived) | $430 cash or 6,140 SmartPoints via MoneySmart | $500 within 30 days of approval | 14 Mar 2026 | |

$0 (first year waived) | $180 cash (PayNow) or 2,800 SmartPoints via MoneySmart with eligible product sign-up Bonus: 20,000 miles with $800 spend MoneySmart March Gold Rush Madness: Stand to win 1 of 12 dazzling 10g gold bars worth over $2,300 each | $800 within first 60 days (plus eligible product for cash/SmartPoints reward) | 31 March 2026 | |

$174.40 (first year waived) | 3% cashback on up to $5,000 spend in first 6 months | None | Ongoing | |

$196.20 (first year waived) | $180 Cash or 2,800 SmartPoints (sufficient to redeem a Sennheiser Accentum Plus Wireless Headphone) | $500 within 30 days of approval | 19 Mar 2026 |

Campaign details above are accurate as of March 2026. Promotions, spend criteria, and eligibility may change—always review the latest terms before applying.

Key trends in credit card promotions (March 2026)

Cash gifts, SmartPoints, and shopping vouchers remain common for new-to-bank promotions, often tied to applications through platforms like MoneySmart. Most offers require $400–$800 spend within the first one to two months, and many include first-year annual fee waivers.

Some MoneySmart-exclusive deals also deliver rewards relatively quickly—sometimes within 5 weeks after meeting the spend requirement. For the latest offers, visit MoneySmart’s credit card promo page.