Apply for Best Personal Loans with Low Interest Rates Starting from 0.9% & Fast Approval in Singapore May 2026

Compare and apply top loan offers in Singapore from leading banks and licensed lenders

Refine Your Results

We found 23 Personal Loans for you!

%20(1).png)

%20(1).png)

Sign up via MoneySmart and claim:

Up to S$4,200 Cash OR 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more) T&Cs apply.

Bonus promotion:

- 1.00% cashback of your loan amount

- Only applicable to loans over S$18,000 with a 3 to 5 year tenure

- New-to-card and new-to-loan customers only

T&Cs apply.

Valid till 15 Jun 2026

Sign up via MoneySmart and claim:

Up to S$1,700 Cash via PayNow OR 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more) T&Cs apply.

Bonus promotion:

- Use promo code: MONEYSMT

- Get S$10 FairPrice E-Vouchers

- New-to-Trust customers only

T&Cs apply.

Valid till 30 Jun 2026

Valid till 30 Jun 2026

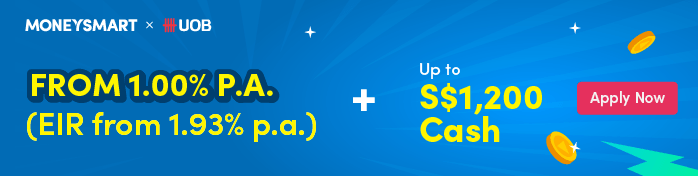

Sign up via MoneySmart and claim:

Up to S$1,200 Cash via PayNow OR 14,335 SmartPoints (enough to redeem an Apple iPhone 17 and more)

And get your rewards in as fast as 4 weeks!

T&Cs apply.

Valid till 07 Jun 2026

Valid till 30 Jun 2026

Valid till 30 Jun 2026

Valid till 30 Jun 2026

.png)

Valid till 30 Jun 2026

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

Disclaimer: At MoneySmart.sg, we strive to keep our information accurate and up to date. This information may be different than what you see when you visit a financial institution, service provider or specific product’s site. All financial products and services are presented without warranty. Additionally, this site may be compensated through third party advertisers. However, the results of our comparison tools which are not marked as sponsored are always based on objective analysis first.

Why MoneySmart is the Trusted Platform for Personal Loans in Singapore 👉

Why Choose MoneySmart?

- MAS-licensed and Ministry of Law approved lenders only

All partners are vetted, licensed, curated, and regulated by the Monetary Authority of Singapore and the Ministry of Law. - Trusted by thousands

Backed by user reviews and a strong track record of helping Singaporeans and expats secure financing through reliable applications. - Fast approvals as quick as 1 hour

Apply online and get results in as little as 1 hour with selected banks and licensed moneylenders. - Digital first

Apply seamlessly via SingPass/Myinfo for a fully online, paperless, and secure application from start to finish. - Inclusive options

Loans are available for Singaporeans, PRs, foreigners, and applicants with lower credit scores. - Flexibility for all applicants

Flexible criteria; personal loans available for a wide range of needs. Compare across banks and licensed moneylenders, all in one place.

How Do Personal Loans Work?

A personal loan in Singapore provides a fixed lump sum upfront, repaid through monthly instalments usually over 1–7 years. Short term loans are also provided by digital banks. Interest rates and fees differ by bank or licensed lender, so comparing options is essential. Singaporeans, PRs, and foreigners can apply online, often benefiting from quick assessments, transparent costs, and flexible repayment terms.

Flat rate vs effective interest rate (EIR)

- Flat rate: Interest is charged on the original loan amount, not the reducing balance. Flat rates are often presented lower, but don’t reflect the true cost of the loan.

- EIR: The real annual cost of borrowing, including compounding interest and other miscellaneous fees like annual fees and one-time processing fees. MAS requires all banks to display EIR on their personal loan products.

- Read More: What is EIR in Personal Loan?

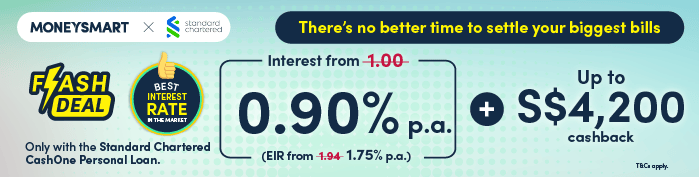

- Example: As of time of writing, Standard Chartered CashOne Personal Loan is advertised at 0.90% p.a. flat, with an EIR of ~1.75% p.a.

What affects loan approval?

- Credit score: Based on your repayment history and outstanding debt.

- Minimum annual income: Banks usually require $10,000–$40,000 for Singaporeans/PRs. This requirement is higher for foreigners.

- Employment type: Salaried employees usually experience smoother approval than freelancers or gig workers due to strict eligibility requirements by banks. That’s why loans from digital banks and licensed moneylenders may be more viable for the self-employed.

- Existing debt: High credit utilisation or multiple loans reduces approval chances. Why? For personal loans, banks use your Balance-to-Income debt servicing ratio to determine if you can take on more credit. Put simply, if too much of your income is already tied up in debt repayments, your chances of approval for future loans drop.

Which Bank Offers the Best Personal Loans and Promotions in Singapore? (June 2026)

MoneySmart’s latest exclusive personal loan promotions give you more cashback, faster gift fulfilment, and lower rates than ever. Whether you’re planning a wedding, consolidating debt, or just need quick cash for a project, here are May 2026’s top personal loan deals — verified and updated.

MoneySmart Exclusive Personal Loan Offers 2026

| Personal Loan | Interest Rate | EIR | Promotion | Valid until |

|---|---|---|---|---|

| Standard Chartered CashOne | From 0.90% p.a. | From 1.75% p.a. | Register through MoneySmart to claim:

Up to S$4,200 cash via PayNow or 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more).

Bonus promotion: | 1 Jun 2026 till 15 Jun 2026 |

| Trust Instant Loan | From 1.00% p.a. | From 2.28% p.a. | Register through MoneySmart to receive up to S$1,700 via PayNow or 19,050 SmartPoints—enough to redeem an Apple iPhone 17 Pro Max and more.

Bonus promotion: | 1 Jun 2026 till 30 Jun 2026 |

| UOB Personal Loan | From 1.00% p.a. | From 1.93% p.a. | Sign up through MoneySmart to claim up to S$1,200 Cash via PayNow or 14,335 SmartPoints, enough to redeem an Apple iPhone 17 and other rewards.

Rewards can be issued in as fast as 4 weeks. | 1 Jun 2026 till 7 Jun 2026 |

| Standard Chartered CashOne (Foreigners) | From 0.90% p.a. | From 1.94% p.a. | Register through MoneySmart to claim:

Up to S$4,200 cash via PayNow or 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more).

Bonus promotion: | 1 Jun 2026 till 15 Jun 2026 |

| Trust Instant Loan (Foreigners) | From 1.00% p.a. | From 2.43% p.a. | Register through MoneySmart to receive up to S$1,700 via PayNow or 19,050 SmartPoints—enough to redeem an Apple iPhone 17 Pro Max and more.

Bonus promotion: | 1 Jun 2026 till 30 Jun 2026 |

💡 MoneySmart Tips

- Rates quoted are illustrative and depend on your credit profile and loan tenure.

- Cashback, SmartPoints or reward fulfilment timelines vary per lender and campaign.

- Rewards are valid for applications via MoneySmart only unless otherwise stated.

- Always refer to the full terms and conditions provided by the lender and application platform.

Personal Loan Comparison in Singapore: Banks vs Licensed Moneylenders

With a curated shortlist of trusted lenders at your fingertips, you can now focus on what really matters—comparing actual loan rates, features, and eligibility details side by side. Here’s a side-by-side look at personal loans from Singapore banks, digital banks, and licensed moneylenders, so you can see at a glance which fits your borrowing needs best.

Bank Personal Loans in Singapore

| Personal loan | Flat rate / EIR (from) | Tenure | Loan Amount Range | Monthly Repayment ($10k/1yr) | Fees | Eligibility |

|---|---|---|---|---|---|---|

| DBS Personal Loan | 1.48% p.a. / 2.84% p.a. EIR | Up to 5 years | Up to 95% of available credit limit | ~$856 | Full repayment penalty: $250 if early Late payment fee: $100 (Credit card PL); $120 (Cashline PL) |

Minimum $20,000 annual income for Singaporeans/PRs Must be 21-70 years old |

| OCBC ExtraCash Loan | 5.42% p.a. / 10.96% p.a. EIR | Up to 5 years | Up to 6x monthly income (if annual income ≥ $120,000) | ~$880 | Processing fees: $100 (if income $20K-$30K); $200 or 2% of loan amount (for higher incomes) Full/partial repayment penalty: 3% of repayment amount (min. $1,000 for partial) Late payment fee: $80 Restructuring fee: 3% of outstanding amount |

Minimum $20,000 annual income for Singaporeans/PRs Minimum $45,000 annual income for foreigners At least 21 years old |

| UOB Personal Loan | 1.00% p.a. / 1.93% p.a. EIR | Up to 5 years | $1,000-$999,999 | ~$839 | Full repayment penalty: $150 or 3% of outstanding loan Late payment fee: $100 (Credit card PL), $120 (CashPlus PL) Cancellation fee: $150 or 3% of outstanding amount No partial repayment penalty |

Minimum $30,000 annual income for Singaporeans/PRs Must be 21-65 years old |

| CIMB Personal Loan | 1.00% p.a. / 1.94% p.a. EIR | Up to 5 years | $2,000-$200,000 (Up to 8x monthly income if annual income > $120,000) | ~$849 | Processing fee: 1% for <$5,000; waived ≥$5,000 Full repayment penalty: None (waived if approved after 22 Jan 2025, else 3% or $250) Late payment fee: $100 |

Minimum $20,000 annual income for Singaporeans/PRs Minimum $30,000 annual income for Malaysians Must be 21-70 years old |

| Standard Chartered CashOne Personal Loan | 1.00% p.a. / 1.94% p.a. EIR | Up to 5 years | Up to 98% of available SCB credit card limit | ~$842 | No processing fee Annual fee: $199 first year ($50/yr after, waived with 12 on-time payments) Full repayment penalty: $150 or 3% of outstanding principal Late payment fee: $100 Restructuring fee: $50 |

Minimum $30,000 annual income for Singaporeans/PRs Minimum $90,000 annual income for foreigners At least 21 years old |

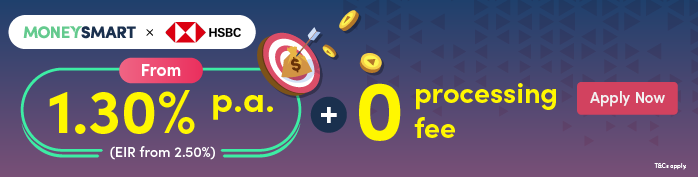

| HSBC Personal Loan | 1.40% p.a. / 2.50% p.a. EIR | Up to 7 years | $1,000-$200,000 (Up to 8x monthly income if annual income ≥ $120,000) | ~$850 | Annual fee: $120 (1st year waived) Full/partial repayment penalty: 2.5% of redemption amount Late payment fee: $120 |

Minimum $30,000 annual income for Singaporeans/PRs Minimum $40,000 annual income for self-employed or commission-based Singaporeans/PRs Minimum $60,000 annual income for foreigners |

Digital Bank Personal Loans

| Digital lender | Flat rate / EIR (from) | Tenure | Loan Amount Range | Monthly Repayment ($10k/1yr) | Fees | Eligibility |

|---|---|---|---|---|---|---|

| Trust Instant Loan | 1.00% p.a. / EIR 2.28% p.a. | Up to 5 years | Up to available credit limit | ~$847 | Late payment fee: $100 Full repayment penalty: 3% |

Minimum $30,000 annual income for Singaporeans/PRs Minimum $60,000 annual income for foreigners Must have a Trust credit card + sufficient credit limit Must be 21-65 years old |

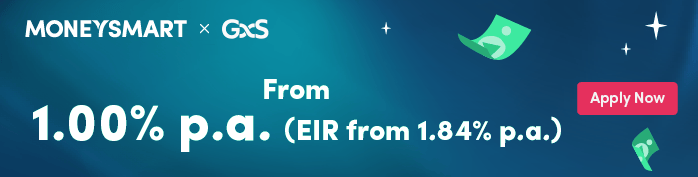

| GXS FlexiLoan | 1.00% p.a. / EIR 1.84% p.a. | Up to 5 years | $100,000 | ~$857 | None | Minimum $20,000 annual income for Singaporeans/PRs Must be 21-65 years old |

| MariBank Instant Loan | 1.86% p.a. / EIR 2.79% p.a. | Up to 5 years | Subject to Maribank’s approval | ~$183 | No late payment but prevailing 30.99% p.a. interest applies if minimum payment not paid in full by due date Early repayment fee: $100 or 3% of remaining unpaid principal amount, whichever is higher |

Minimum $30,000 annual income for Singaporeans/PRs (≤ 55 y/o) Minimum $15,000 annual income for Singaporeans/PRs (≥ 55 y/o) Must be a Mari Credit Cardholder (with $500 credit limit) At least 21 years old |

| Friday Finance Personal Loan | 10.56% p.a. / EIR 11.09% p.a. | Up to 18 months | Up to 6x monthly income | ~$1,013 | Processing fee: 8% Late payment fee: $40 |

At least 21 years old |

Licensed Moneylenders Personal Loans (MAS Licensed)

| Personal loan | Flat rate / EIR (from) | Tenure | Loan Amount Range | Monthly Repayment ($10k/1yr) | Fees | Eligibility |

|---|---|---|---|---|---|---|

| Trillion Credit Solutions Personal Loan | 26.60% p.a. / EIR 30.09% p.a. | Up to 30 months | Up to 6x monthly income | ~$1,060 | Processing fee: 10% of loan amount Late payment fee: $60/month |

Minimum $20,000 annual income At least 18 years old |

| Credible.sg Personal Loan | 10.5% p.a. / EIR 11% p.a. | Up to 3 years | Up to 6x monthly income | ~$950 | Processing fee: From 5% Late payment fee: From 2% |

Minimum $20,000 annual income for Singaporeans/PRs Minimum $40,000 annual income for foreigners |

| Best Licensed Moneylender Personal Loan | 12.12% p.a. / EIR 12.82% p.a. | Up to 3 years | Up to 6x monthly income | From ~$889 | Processing fee: 10% (deducted from loan) Late fee: $60/month |

Minimum $20,000 annual income At least 21 years old |

| Cash Direct Licensed Moneylender Personal Loan | 11.60% p.a. / EIR 12.20% p.a. | Up to 2 years | Up to 6x monthly income | ~$930 | Processing fee: From 8% Late payment fee: $60/month |

Minimum $10,000 annual income for Singaporeans/PRs Minimum $40,000 annual income for foreigners Must be 18-65 years old |

Disclaimer: All interest rates, loan amounts, and monthly repayment figures shown are illustrative estimates drawn from MoneySmart’s comparison data and/or provider websites. Actual offers may differ based on individual credit assessment and are subject to change at the provider’s discretion without prior notice.

💡 MoneySmart Tip

A traditional bank loan usually offers some of the lowest effective interest rates, though they also tend to have stricter eligibility requirements.

Digital banks have become increasingly competitive and can be just as affordable, often providing a strong middle ground with fast approvals, low fees, and app-based convenience.

In contrast, licensed moneylenders typically carry much higher EIRs and lower loan limits tied to your income level, making them best reserved for urgent, short-term borrowing.

Always use MoneySmart to compare across providers and secure the most cost-effective option.

How Much Does a $10,000 Loan Cost Monthly?

| Bank | Loan Amount | Interest Rate (p.a.) | EIR (p.a.) | Tenure | Monthly Repayment (approx.) |

|---|---|---|---|---|---|

| UOB | S$10,000 | 1.00% | 1.93% | 12 months | S$842 |

| UOB | S$10,000 | 1.00% | 1.93% | 36 months | S$286 |

| Standard Chartered | S$10,000 | 1.00% | 1.94% | 12 months | S$842 |

| Standard Chartered | S$10,000 | 1.00% | 1.94% | 36 months | S$286 |

| CIMB | S$10,000 | 1.00% | 1.94% | 12 months | S$842 |

| CIMB | S$10,000 | 1.00% | 1.94% | 36 months | S$286 |

13 Smart Ways Singaporeans and Expats Use Personal Loans

- Wedding expenses ➡ Best Wedding Loans in Singapore

- Home renovations ➡ Personal Loan Guides for Home Renovations

- Education & upskilling ➡ Best Education Loans in Singapore

- Medical bills & emergencies ➡ Best Emergency Loans in Singapore

- Credit card debt consolidation ➡ Debt Consolidation Plan

- For liquidity ➡ Emergency Cash Loans

- Car ownership & COE renewal ➡ Personal Loan Guides for Cars/COE

- Downpayment loan ➡ Personal Loans for Downpayment

- Expat needs ➡ Personal Loans for Foreigners in Singapore

- Loans for travel expenses ➡ Personal Loans for Travel Expenses

- Funeral costs ➡ Personal Loans for Funeral Expenses

- Vet bills ➡ Personal Loans for Vet Bills

- Investments (not recommended) ➡ Can You Use a Personal Loan to Invest in Singapore?

💡In general, personal loans are best for planned expenses with clear repayment ability. If you’re unable to comfortably repay your monthly instalments, taking up a personal loan could worsen your debt situation—and we strongly advise against borrowing irresponsibly. Always compare interest rates, fees, and tenure before applying, so your loan works for you, not against you.

Quick Comparison: Urgent Instant Loans in Singapore

| Product / Bank | Approval / Disbursal time |

|---|---|

| DBS Personal Loan | Instant approval and fund disbursement |

| UOB Personal Loan | Instant approval (8am–9pm), same-day disbursement |

| OCBC ExtraCash Loan | Instant approval and disbursement via MyInfo |

| SCB CashOne Personal Loan | Instant approval and disbursement |

| HSBC Personal Loan | 1-minute in-principle approval; funds in 3–5 days |

| CIMB Personal Loan | Instant approval and disbursement |

| Trust Instant Loan | Approval and disbursement within 60 seconds |

| GXS FlexiLoan | Approval in under 3 minutes, instant disbursement |

| MariBank Instant Loan | Instant approval, funds credited in ~10 seconds |

| Best Licensed Moneylender | Approval within 2 hours, instant fund release |

| Cash Direct Licensed ML | Approval in 30 minutes, same-day disbursement |

Instant personal loans in Singapore offer a critical safety net for urgent financial needs—whether it’s a medical emergency, last-minute travel, or unexpected bills. With digital banks and licensed moneylenders now able to approve and disburse funds in minutes, you can access cash quickly without lengthy paperwork or waiting periods.

If you want to understand when and how to use instant loans responsibly, see our guide to personal loans for emergencies for practical tips and eligibility details.

How to Qualify and Apply for a Personal Loan in Singapore

Eligibility & documents by borrower type

| Borrower profile | Minimum annual income | Lender examples | Typical documents required |

|---|---|---|---|

| Singaporeans/PRs | $10,000-$30,000 | GXS FlexiLoan: $20,000 SCB CashOne Personal Loan: $30,000 HSBC Personal Loan: $30,000 UOB Personal Loan: $30,000 CIMB Personal Loan: $20,000 |

NRIC Latest payslips, or CPF Contribution History, or Latest Tax Notice of Assessment (NOA) |

| Foreigners (Employment Pass) | $40,000-$90,000 | SCB CashOne Personal Loan: $90,000 HSBC Personal Loan: $60,000 CIMB Personal Loan: $30,000 (Malaysians) |

Passport Employment Pass Proof of income (payslips, bank statements) Proof of residence (tenancy agreement or utility bill) |

| Self-employed / freelancers | $10,000-$40,000 | N/A | NRIC / Employment Pass Latest Tax NOA 12 months’ CPF contribution history or bank statements |

| Licensed moneylender loans | Depends on lender | N/A | Valid ID (NRIC/passport) Proof of residence (tenancy agreement or utility bill) Proof of income (if available) |

Disclaimer: Minimum income thresholds are indicative and vary across lenders. Document requirements listed are non-exhaustive, and additional documents may be requested by lenders as part of their assessment.

Additionally, applying for a personal loan online in Singapore is now faster and easier than ever. With SingPass/MyInfo integration, approvals can take just minutes and funds are disbursed straight into your account. Here’s a step-by-step guide to make the process smooth and stress-free.

Compare & shortlist loans

💡 Remember to look beyond the headline rates; check the EIR and fees reflecting the true cost of your loan.

Check eligibility

- Singaporeans/PRs: $10,000-$40,000

- Foreigners: $40,000-$60,000 with valid EP/S Pass.

- Usually ≥ 18 or 21 years old to apply

Prepare necessary documents

- Singaporeans/PRs: NRIC + payslips/CPF + proof of address

- Foreigners: Passport + EP/S Pass + payslips + employment contract + proof of residence (e.g. utility bills)

Apply for personal loan online via MoneySmart

You’ll also be prompted to submit your email address on our MoneySmart Rewards Form to qualify and track your sign-up reward upon applying through us.

Wait for loan application review and approval

Receive your loan disbursement funds

Monitor your SMS or email for confirmation and payment details.

No Payslip for Personal Loans? No Problem.

Need extra funds but don’t have a fixed monthly salary? Our guide shows you how freelancers, gig workers, and self-employed individuals in Singapore can qualify for personal loans, what documents you’ll need, and which lenders are most flexible.

Personal Loan vs Line of Credit in Singapore: Quick Comparison

| Feature | Personal loan | Line of credit |

|---|---|---|

| How it works | Lump sum disbursed upfront, repaid in fixed monthly instalments | Flexible drawdowns, only pay interest on amount used |

| Interest rates | From 1.00% p.a. (EIR ~1.93-7%) | ~20-29% p.a. (e.g. DBS Cashline: 22.9% p.a.) |

| Loan amounts | Can be up to 10x monthly income, depending on lender | Based on approved credit limit, usually lower than a loan |

| Loan tenure | Up to 7 years (e.g. HSBC personal loan) | Revolving, no fixed end date Credit replenishes as you pay down balance |

| Fees | ~1–3% one-time processing fees (often waived in promos) Some banks like SCB CashOne charge annual fees like $199 for the 1st year, $50 thereafter |

Recurring annual fees: ~$100–$120 (1st year waived at banks e.g. DBS, HSBC) |

| Best for | Planned expenses like weddings, home renovations, debt consolidation | Ongoing or unpredictable needs like emergency cash, short-term use |

When to choose a personal loan?

- You want lower interest rates and structured monthly repayments.

- You need a large lump sum for a one-time expense.

- E.g. Standard Chartered CashOne Personal Loan, UOB Personal Loan, Trust Instant Loan, HSBC Personal Loan

- ⭐ Overall, personal loans remain the more cost-effective option for planned spending.

When to choose a line of credit?

- You want flexible access to cash without reapplying.

- You only need to borrow occasionally or in small amounts.

- You can repay quickly to avoid high interest.

- E.g. DBS Cashline, UOB CashPlus

- ⭐ Lines of credit offer unmatched flexibility but come at higher costs and recurring fees.

Personal Loan VS Line of Credit: What's the Difference?

Is it Better to Get a Secured or Unsecured Loan in Singapore?

Secured loans typically offer lower interest rates and higher borrowing amounts, but require you to pledge an asset (such as property or a vehicle) which could be repossessed if you default.

By contrast, unsecured loans are quicker to access and don’t put your personal assets at risk, but generally come with higher interest rates and stricter eligibility due to the lack of collateral.

Secured loans

A secured loan is backed by collateral - such as a home, car, or fixed deposit-which the lender can claim if you fail to keep up with repayments.

Pros:

-

Generally lower interest rates, since your asset reduces the lender's risk.

-

Higher borrowing limits, making them suitable for big purchases (e.g., homes, cars).

-

Longer repayment periods mean smaller and more manageable monthly instalments.

-

Can be easier to qualify for if your credit score is not strong, as collateral reduces lender risk.

Cons:

-

If you default, you risk losing the pledged asset.

-

Applications can take longer, due to collateral valuation and extra legal documentation.

-

If the collateral's sale value doesn't cover the debt upon default, you may still owe the balance.

When to choose a secured loan in Singapore:

Unsecured loans

An unsecured loan requires no collateral; approval is mainly based on your credit history, income, and existing debt obligations. Examples include personal loans, education loans, and renovation loans.

Pros:

-

No personal asset is at risk if you hit repayment issues.

-

Faster approval, as no collateral valuation is needed.

-

Funds can typically be used for any reason (emergencies, consolidating debt,weddings, etc.).

-

Fewer documents required, so application is simpler.

Cons:

-

Interest rates tend to be higher because the bank is taking on more risk.

-

Lower loan amounts compared to secured loans.

-

Stricter eligibility, with approval hinging on your credit score and income.

-

Default still hurts your credit record and can affect your future borrowing ability.

When to choose an unsecured loan in Singapore:

-

You need fast access to a smaller amount for short-term needs.

-

You have strong credit and steady income.

-

You're uncomfortable risking personal assets and want a fuss-free process.

FAQs About Personal Loans

Can foreigners apply for personal loans in Singapore?

- Yes. Some banks like HSBC Personal Loan (min. S$60,000 income) and Standard Chartered CashOne Personal Loan (min. S$90,000 income) accept foreigners with Employment Passes.

Licensed moneylenders are also open to foreigners, though loan amount caps are based on income. What’s the difference between banks and licensed moneylenders?

- Banks: Lower interest rates, larger loan amounts, and generally stricter qualifying eligibility.

Licensed moneylenders: Relatively more lenient in eligibility and offer easier approvals, especially for lower-income borrowers or foreigners. However, interest is capped at 4% per month under MinLaw rules. How much can I borrow?

- Banks: Up to 10x your monthly income (subject to credit assessment).

Licensed moneylenders: Under MinLaw rules, you can only borrow up to $3,000 if your annual income < $20,000. If your income exceeds that, your loan amount caps can increase. Can unemployed individuals get a loan?

- No, banks will not approve personal loans for unemployed borrowers. Licensed moneylenders may approve small loans if you can show proof of residence and identification, but interest rates will be higher.

Do late payments affect my credit score?

- Yes. Both banks and licensed moneylenders report to the Credit Bureau Singapore (CBS). Missed or late payments lower your score and hurt future loan applications. Always repay on time.

What is personal loan eligibility in Singapore?

- Eligibility depends on citizenship, age, and income:

- Singaporeans/PRs: Typically 21–65 years old, with minimum annual income of $10,000–$40,000.

- Foreigners: 21–65 years old, usually minimum annual income of $40,000–$90,000 with valid EP/S Pass.

- Bad Credit / Special Cases: Banks may reject applications with undischarged bankruptcies or ongoing debt schemes. Licensed moneylenders may consider bad-credit applicants if income is stable.

Can I get urgent or digital loan approvals in Singapore?

- Yes. Many banks and digital banks allow online applications using SingPass/MyInfo, with instant or same-day approvals if you meet criteria. Licensed moneylenders may also offer same-day cash, but always review fees and terms before committing.

What should I do if I have bad credit or have been rejected?

- Banks rely heavily on CBS credit scores, so poor credit lowers your chances. Licensed moneylenders may still approve smaller loans, but at higher costs. If rejections persist, consider credit counselling to improve your finances before reapplying.