Why Trust MoneySmart?

Why Trust MoneySmart?When booking a flight online, you’ve probably noticed the little box offering travel insurance from the airline. It looks convenient—just one click and you’re covered. But is it really the best option for your trip? Airline travel insurance can be handy for simple journeys, yet it often comes with limits you might not realise until it’s too late.

This guide walks you through what airline insurance usually covers and how it compares with third-party plans. By the end, you’ll know whether to stick with the airline’s offer or explore more comprehensive alternatives.

Key Takeaways

Airline travel insurance is convenient at checkout, but coverage is often limited to flight-related issues.

Third-party providers usually offer stronger benefits, including higher medical coverage, broader trip cancellation protection, and more flexible add-ons.

For simple, low-risk trips, airline insurance might be enough — but for most travellers, standalone travel insurance delivers far better value.

Always review the fine print and compare options before you pay, as airline add-ons can be more expensive and less comprehensive than buying separately.

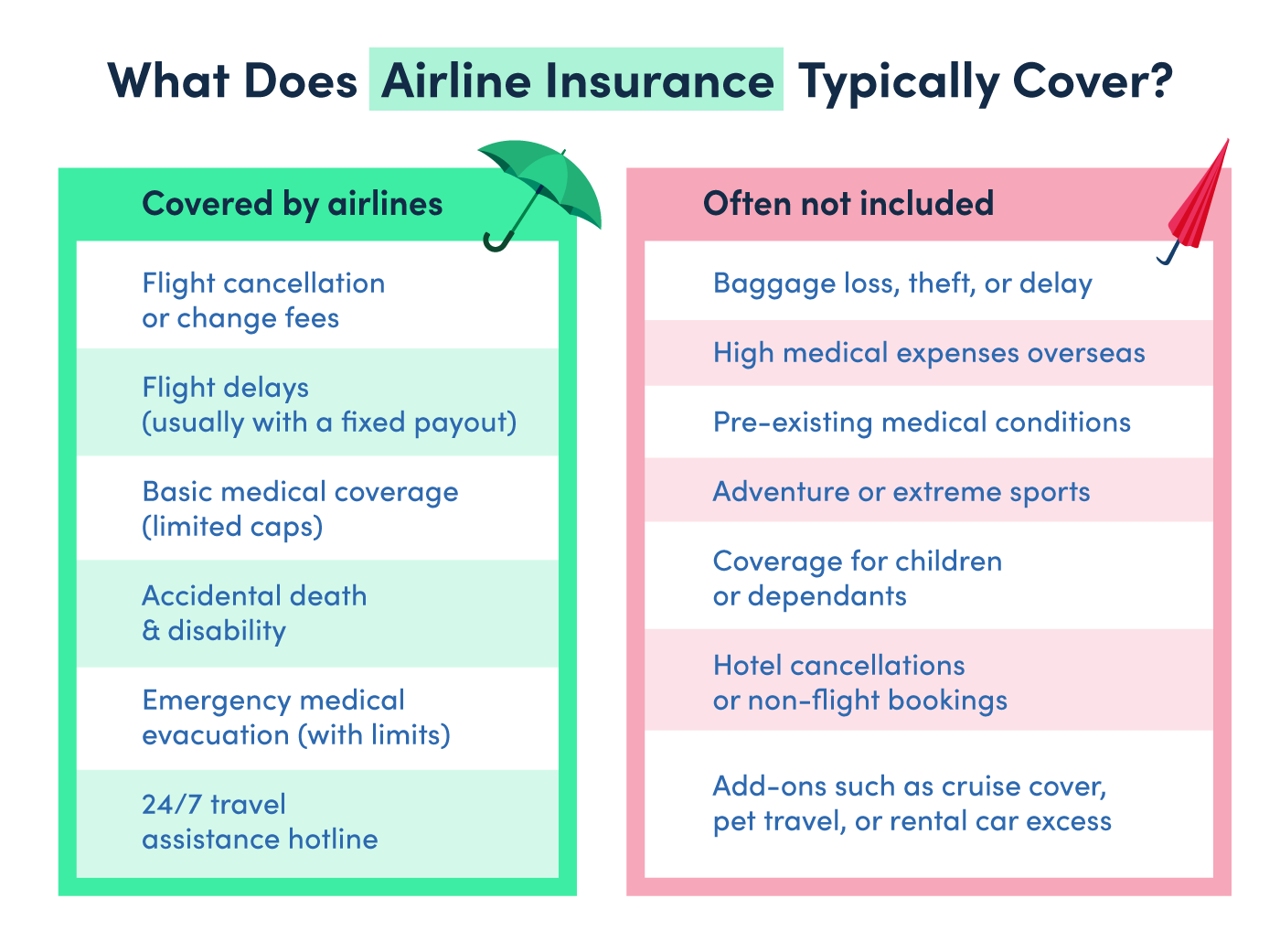

What Does Airline Insurance Typically Cover?

Airline travel insurance usually focuses on protecting your flight booking rather than your entire trip. While it can give peace of mind for disruptions directly tied to your ticket, the scope is often narrower than third-party policies.

Here’s a breakdown of what’s commonly covered and what’s often left out:

In a nutshell, airline-issued plans are flight-centric, so if your trip involves multiple bookings, activities, or higher health risks, you may find critical gaps in protection.

Comparison: Airline vs Third-Party Travel Insurance

At first glance, buying travel insurance from the airline feels convenient. But when you compare cost, benefits, and flexibility with standalone travel insurance, the trade-offs become clearer.

We’ve previously done an in-depth airline vs third-party travel insurance comparison on the MoneySmart blog. Here’s a summary:

Factor | Airline Travel Insurance | Third-Party Travel Insurance |

|---|---|---|

Cost | Generally affordable for short trips (e.g., Scoot: ~$47 for 7 days to Bangkok; AirAsia: ~$24–29) but can get expensive for long-haul (Cathay: $262 for 7 days to London) | Wide price range, but budget plans (e.g., FWD, Tiq) often offer more coverage for the same or lower price than airlines |

Coverage Breadth | Focused on flights; medical and baggage coverage vary widely. Some plans are generous (Emirates: unlimited medical) but many are limited (AirAsia: only $10,000 medical, $600 trip cancellation) | Broader coverage: higher caps for medical (median $500,000), stronger baggage ($5,000 median), and more comprehensive trip cancellation (up to $20,000) |

Refund Policies | Usually strict; once purchased, cancellation or refund is difficult, and benefits may not apply if insurance was bought less than 3 days before departure | More flexibility; some insurers allow policy cancellation before the trip begins, subject to terms |

Claim Process | Typically submitted online or through the insurer’s portal/app; payouts often fixed (e.g., $100 per 6 hours for delays) rather than based on actual expenses | Also submitted online or via app; usually reimburses actual, documented costs like hotels, meals, and rebooking fees |

Add-Ons | Limited or no add-ons; usually excludes adventure sports, cruises, pet travel | Wide variety of add-ons available: extreme sports, cruise cover, rental car excess, coverage for pre-existing conditions |

Premium and coverage information correct as of 19 Feb 2026

On the whole, airline travel insurance can work for simple, low-risk trips, but if you want comprehensive protection—especially for medical emergencies, baggage, or multi-leg journeys—third-party travel insurance offers much stronger value.

Best Alternatives to Airline Insurance

If you want broader protection and better value than what airlines typically provide, third-party insurers are often the smarter choice. Here are some of the strongest options available in Singapore:

FWD – Best Budget-Friendly Option

For travellers looking for affordability without sacrificing core benefits, FWD is a solid entry point. Prices for a 7-day ASEAN trip start from $34, with medical coverage ranging from $200,000 to $1,000,000 depending on the plan. You’ll also get trip cancellation protection of $7,500 to $15,000 and baggage cover of $3,000 to $7,500. Do note, however, that COVID-19 coverage is not built in and must be purchased as an add-on.

Starr – Value for Money with COVID Coverage Included

Starr is another budget-friendly insurer, with 7-day ASEAN plans starting from $58. While its entry-level benefits are slightly lower—$200,000 medical coverage, $5,000 for trip cancellation, and $3,000 for baggage—COVID-19 coverage is automatically included. This makes Starr a convenient option if you prefer not to manage add-ons separately.

MSIG – Suitable for Pre-Existing Conditions

MSIG stands out as one of the few insurers in Singapore that offer travel insurance designed for travellers with pre-existing conditions. Plans provide up to $150,000 in medical coverage, along with a generous $15,000 for trip cancellation and $7,500 for baggage protection. This makes MSIG particularly valuable for older travellers or those managing ongoing health issues.

Tiq – Best for Travel Delay Benefits

If you’re concerned about the inconvenience of delays, Tiq is worth considering. It offers $50 for every 3 hours of delay overseas, which is more traveller-friendly than the industry norm of $100 for every 6 hours. That means faster, more frequent payouts if your schedule is disrupted.

Compared to airline-issued policies, these third-party insurers provide stronger medical and cancellation cover, more generous baggage limits, and extras like coverage for pre-existing conditions or quicker compensation for delays—all at competitive prices.

When Airline Insurance Might Be Enough

Airline travel insurance can serve its purpose in certain low-risk scenarios. If your trip is straightforward and you’re mainly concerned about flight disruptions, the convenience of adding insurance at checkout could be sufficient.

It may be enough for:

Short business trips, especially when your employer provides additional coverage.

Direct flights with no checked luggage, since fewer moving parts mean fewer chances of baggage issues.

Low-cost trips with minimal risk, such as budget getaways where you don’t need extensive coverage.

In a nutshell, airline-issued insurance should only be considered if you don’t require strong baggage protection or comprehensive medical coverage. For most other situations, a third-party plan usually offers far broader protection.

What Happens if You Miss a Flight Connection?

Missed connections are one of the grey areas in airline travel insurance. Coverage can vary widely depending on the carrier and the specific policy.

Coverage Under Airline Policies

Some airline plans include limited benefits. For instance, Scoot’s travel insurance provides a payout of $100 for every 6 hours of delay, capped at $600. These are usually fixed-sum payouts rather than reimbursements for your actual expenses.

How Third-Party Insurers Handle Missed Connections

Independent travel insurers often provide broader protection. They may cover additional costs such as rebooking fees, meals, or overnight accommodation if your missed connection is due to a covered reason like a flight delay or severe weather.

Why the Fine Print Matters

Whether you buy from an airline or a third party, always review the exclusions carefully. If the delay is your fault—say you arrived late at the gate because you didn’t budget enough time for traffic—you won’t be compensated.

Bottom line |

Airline insurance may give you a token payout, but third-party policies are generally more reliable for covering the real costs of a missed connection. |

What You Might Miss If You Only Use Airline Insurance

Airline-issued policies focus heavily on flights, which means you could be left exposed in other areas of your trip. Here are some important gaps to watch out for:

No Personal Liability Protection

If you accidentally injure someone or damage property overseas, most airline travel insurance won’t cover the costs. Third-party policies typically include personal liability coverage, which can protect you from substantial financial risk.

No Protection for Non-Flight Bookings

Hotel reservations, tours, or event tickets are generally not covered under airline-issued plans. If your trip is cancelled, you’ll likely lose those pre-paid costs unless you have a more comprehensive third-party policy.

No Add-Ons for Special Activities

Airline policies are usually limited to standard travel. Extras like adventure sports, cruises, pet travel, or rental car excess are not available, which could be a dealbreaker if your trip involves anything outside the basics.

All in all, airline insurance may cover your flight, but it won’t cover your trip in its entirety. If your plans are more complex, third-party insurance is almost always the safer choice. |

How to Avoid Being Overcharged

Airline travel insurance can be convenient, but it’s not always the most cost-effective choice. Here’s how to make sure you’re not paying more than you should:

Watch for Pre-Selected Insurance at Checkout

Some airlines automatically tick the insurance box during booking. Always review your cart carefully before payment to avoid paying for a policy you didn’t actively choose.

Compare Before You Commit

Use MoneySmart’s comparison tool to weigh the airline’s offer against third-party options. A side-by-side airline travel insurance comparison often reveals that broader coverage is available for a similar or even lower price.

Consider Buying Separately

In many cases, removing insurance from your flight booking and purchasing a standalone plan can save more than 30%. Beyond the cost savings, you’ll also get a policy with more comprehensive benefits.

💡 MoneySmart Tip |

Use trusted online comparison tools like MoneySmart's travel insurance comparison to explore coverage limits, premiums, and policy features across leading insurers in Singapore—helping you find the right insurance plan for your trip, quickly. |