Why Trust MoneySmart?

Why Trust MoneySmart?Imagine working from a café in Chiang Mai or a beach in Bali—and then your laptop gets stolen or you fall ill mid-trip. Standard travel insurance often isn’t enough. Long-term travellers, freelancers, and remote workers from Singapore need more than just emergency coverage—they need protection for ongoing health, gear, and unpredictable work-related disruptions.

That’s where digital nomad insurance comes in—designed for longer stays, multiple countries, and modern needs. Here’s your complete guide to finding the right one in 2026.

Key Takeaways

Nomads need more than standard travel insurance — longer stays, multiple destinations, work gear, and sometimes ongoing health care.

Subscription-based plans like SafetyWing or Genki offer flexibility; single-trip policies work best for short, fixed holidays under 90 days.

Add-ons matter — electronics, adventure sports, mental health, and trip delay cover can make or break your policy.

Don’t ignore exclusions — pre-existing conditions, professional gear, or visa issues often fall outside coverage.

Smooth claims require preparation — save receipts, use apps, and pick insurers with direct billing to avoid paying large sums upfront.

Who is considered a digital nomad?

A digital nomad is anyone who works remotely while travelling for extended periods. This includes freelancers, creatives, start-up founders, and employees on remote contracts.

Why does this matter for insurance? Because unlike tourists, nomads:

Carry expensive work gear (laptops, cameras, headphones).

Stay months instead of weeks, which breaks standard trip duration limits.

Travel to multiple destinations in one year, making single-country cover insufficient.

Need insurance proof for digital nomad visas offered by countries like Portugal, Estonia, Georgia, and Thailand.

For Singaporeans, common hotspots include Bali, Chiang Mai, Da Nang, Seoul, Tbilisi, and Lisbon. Each has thriving nomad communities and, increasingly, visa schemes that require proof of valid insurance.

Medical vs travel insurance: What’s the difference for digital nomads?

It’s easy to confuse travel insurance with health insurance, but the difference is critical.

Travel insurance: Best for unexpected incidents—a stolen laptop, food poisoning abroad, flight delays.

International health insurance: Best for ongoing care—GP visits, prescriptions, dental, or managing chronic conditions.

Why this matters |

If you only rely on travel insurance, you’ll be covered for emergencies but not for routine needs. A hybrid nomad plan (e.g., SafetyWing Complete or Genki Native) combines both—ideal for those living abroad long-term and applying for nomad visas. |

READ: International Health Insurance vs Travel Insurance

Monthly subscription vs single-trip plans

Nomads face a different challenge than holidaymakers: they don’t always know when their trip will end. That’s why the way you pay for insurance matters as much as the coverage itself.

Monthly Subscription Plans

Flexible, auto-renews monthly

Great for open-ended itineraries

Some include global health features

Single-Trip Policies

Fixed duration (usually ≤90 days)

Cheaper upfront

Ideal for fixed-length holidays but impractical for nomads

Tip |

If you’re trying out nomad life, a single-trip plan might work. But if you’re committed to months abroad, go with a subscription—otherwise, you risk being uninsured after day 90. |

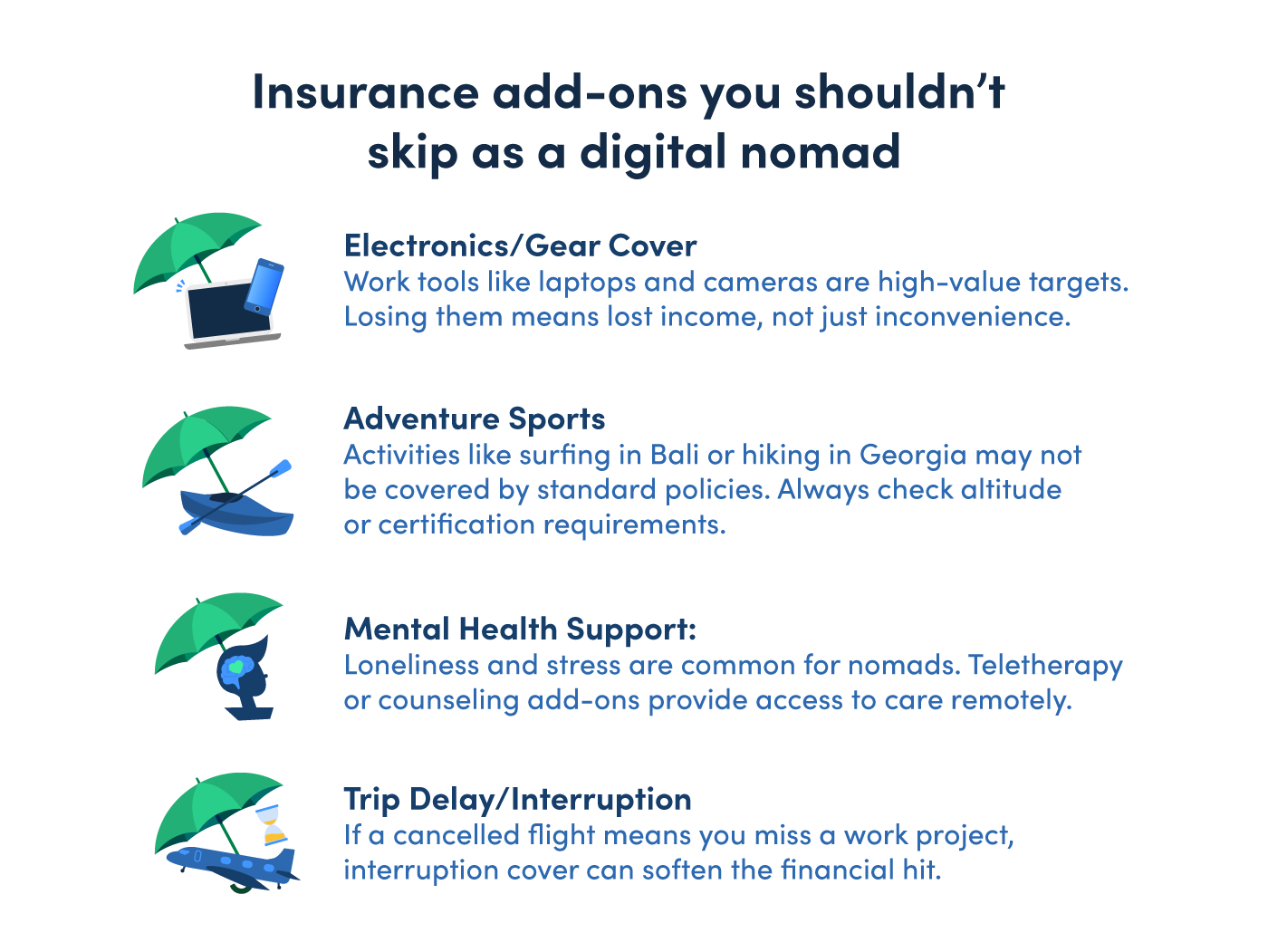

Insurance add-ons you shouldn’t skip as a digital nomad

Nomads have unique risks that go beyond what tourists face. That’s why optional add-ons often matter more:

Electronics/Gear Cover: Work tools like laptops and cameras are high-value targets. Losing them means lost income, not just inconvenience.

Adventure Sports: Activities like surfing in Bali or hiking in Georgia may not be covered by standard policies. Always check altitude or certification requirements.

Mental Health Support: Loneliness and stress are common for nomads. Teletherapy or counseling add-ons provide access to care remotely.

Trip Delay/Interruption: If a cancelled flight means you miss a work project, interruption cover can soften the financial hit.

Why this matters |

Nomad life isn’t just about leisure. It’s also about working sustainably abroad. Specific add-ons protect both your lifestyle and your income. |

Top travel insurance for digital nomads (2026)

Not all insurers are built for nomads. Some focus on emergency-only coverage, others combine travel and health.

Here’s how some of the better ones compare:

Provider | Coverage Duration | Gear Limits (Electronics) | Medical Limits | Subscription / Flexibility | Home Trip Coverage |

|---|---|---|---|---|---|

SafetyWing Complete | Monthly subscription, renewable | Electronics add-on: ~US$1,000/item (add-on required) | Up to US$1.5 million (includes outpatient + emergency) | Highly flexible—can pause/resume or renew takes effect monthly | Full home coverage, no time restriction |

Genki Native | Monthly subscription, renewable | Limited or no electronics cover—primarily health-focused | Comprehensive global health (incl. outpatient, maternity, mental health) | Flexible subscription | Up to 6 months in home country (per sources) |

World Nomads | Annual / Multi-trip (≤6 months per trip) | Under baggage/personal belongings—unstated caps; must check product disclosure statement (PDS). | Emergency medical—ranges vary (US$100k+) | Less flexible—must purchase pre-trip, extensions possible mid-trip | Usually not covered for home visits |

PassportCard Nomads | Subscription-based | Electronics under personal belongings; separate cover exists | Health + emergency medical—app-based cashless claims | Highly flexible; app-first model | Short home visits may be included—check terms |

FWD (Premium / First) | Single-trip (≤90 days) or annual | Baggage cover up to S$7,500; per-item caps (~S$500–1,000) | Medical + evacuation up to S$1 million | Fixed-term only—no subscription flexibility | Not included |

Note: Premiums vary depending on age, destinations, and trip length. Always get a personalised quote from the provider. Coverage also differs by plan tier (basic vs premium). Limits shown are maximums, and claims are still subject to per-item caps, conditions, and exclusions as stated in each insurer’s policy wording.

Tips for choosing the right insurance

The cheapest plan isn’t always the best. Think about how you’ll actually use it as you travel from coast to coast.

Check if claims are app-based: Uploading receipts via mobile saves time compared to mailing documents.

See if you can renew abroad: Many local Singapore policies require you to be home to extend—nomad plans don’t.

Global customer support: 24/7 support across time zones is crucial if you’re calling from Europe while your insurer is in Asia.

Direct billing networks: Avoid paying out-of-pocket in places where hospital deposits are required.

Why this matters |

For nomads, ease of use is as important as coverage—because you may be far from home when you need support. |

Tips for claims as a digital nomad

Even the best insurance fails if you can’t make a claim. Nomads often move fast, making documentation tricky. Here’s how to stay prepared:

Keep digital copies of receipts and reports in the cloud.

Ask for English-language medical reports—insurers may reject vague or untranslated documents.

Use insurers with mobile claim apps (SafetyWing, PassportCard).

Choose plans with cashless hospital partnerships so you don’t need to pay upfront.

Why this matters |

Claim readiness prevents financial stress when emergencies strike—and keeps you focused on your work. |

Alternatives to traditional travel insurance for digital nomads

Some digital nomads find that traditional travel insurance isn’t enough. Here are some alternatives worth exploring:

SafetyWing Complete / Remote Health: Combines travel and expat-style health insurance—covers emergencies and routine care.

PassportCard Nomads: Gives you a prepaid claims card—use it like a debit card at hospitals instead of waiting for reimbursement.

Expat Global Health Plans (Cigna, Aetna, Allianz): Best if you’re basically relocating for >12 months. Expensive, but comprehensive.

Genki Native: Designed for nomads, with outpatient, preventative, and mental health care included.

Why this matters |

If you’re abroad indefinitely, a traditional travel-only plan may leave gaps. Hybrid or expat plans might suit you better. |

What digital nomad plans don’t cover

Even the best digital nomad insurance has blind spots. Knowing these upfront helps you avoid nasty surprises and plan workarounds.

Pre-existing medical conditions: Most nomad policies exclude ongoing issues like diabetes, asthma, or old injuries. For these, you’d need expat/global health insurance.

Professional equipment: While laptops and cameras may be covered for theft or damage, insurers often exclude gear used for commercial purposes (i.e. your work tools).

High-risk activities: Adventure sports may be restricted. For example, motorbike accidents without a valid license or hiking above set altitudes often aren’t covered.

Visa or immigration issues: Missed flights or costs due to rejected visa applications usually fall outside coverage, as these are considered legal/admin issues.

Extended time back in Singapore: Many nomad plans allow only short “home visits” (30–90 days). Longer stays back home may void your coverage.

Why this matters |

These exclusions don’t mean nomad insurance is useless—it just means you may need to buy separate gadget cover or consider an expat plan if you have ongoing medical needs. |

Final thoughts

The digital nomad lifestyle offers freedom, but it’s always prudent to account for its unpredictability. Having the right insurance ensures you can focus on work and travel without fear of financial setbacks.

👉 To compare plans side-by-side and find one that fits your nomad lifestyle, check the MoneySmart travel insurance listing page.